Potrebbero piacerti anche

- Turtle StrategyDocumento31 pagineTurtle StrategyJeniffer Rayen100% (3)

- The Foreign Exchange MarketDocumento145 pagineThe Foreign Exchange MarketNikita JoshiNessuna valutazione finora

- Time Value of Money Explained in 40 CharactersDocumento78 pagineTime Value of Money Explained in 40 Charactersneha_baid_167% (3)

- Practice Questions - International FinanceDocumento18 paginePractice Questions - International Financekyle7377Nessuna valutazione finora

- Purchasing Power ParityDocumento17 paginePurchasing Power ParitySwati Dhoot100% (1)

- Small Business LoansDocumento2 pagineSmall Business Loanskirandasi123Nessuna valutazione finora

- High-Q Financial Basics. Skills & Knowlwdge for Today's manDa EverandHigh-Q Financial Basics. Skills & Knowlwdge for Today's manNessuna valutazione finora

- Depreciation ExerciseDocumento11 pagineDepreciation Exerciserikita_17100% (2)

- Defining The Bull & BearDocumento8 pagineDefining The Bull & BearNo NameNessuna valutazione finora

- Working Capital Management in Steel IndustryDocumento54 pagineWorking Capital Management in Steel IndustryPrashant Singh50% (2)

- Engineering Economics CH 2Documento81 pagineEngineering Economics CH 2karim kobeissiNessuna valutazione finora

- Solnik & McLeavey - Global Investments 6th EdDocumento8 pagineSolnik & McLeavey - Global Investments 6th Edhotmail13Nessuna valutazione finora

- Investments - Risk & ReturnDocumento85 pagineInvestments - Risk & ReturnBushra JavedNessuna valutazione finora

- Lecture03 Parity StudentDocumento23 pagineLecture03 Parity StudentMit DaveNessuna valutazione finora

- IFM ProblemsDocumento107 pagineIFM ProblemsRammohanreddy RajidiNessuna valutazione finora

- 3.1 Research Methodology: Mutual FundDocumento12 pagine3.1 Research Methodology: Mutual FundAbdulRahman Elham40% (5)

- Chapter 3 Forward ContractsDocumento79 pagineChapter 3 Forward ContractsMalek Ben HmidaNessuna valutazione finora

- Multinational Finance Butler 5th EditionDocumento2 pagineMultinational Finance Butler 5th EditionUnostudent2014Nessuna valutazione finora

- International Parity RelationshipsDocumento11 pagineInternational Parity RelationshipsIsunni AroraNessuna valutazione finora

- Lent 2020 Week 7 Test Revision AnswersDocumento4 pagineLent 2020 Week 7 Test Revision AnswersShihab HasanNessuna valutazione finora

- If Chapter 4 Determining The Exchange RateDocumento67 pagineIf Chapter 4 Determining The Exchange Rateธชพร พรหมสีดาNessuna valutazione finora

- Midterm Exam 1 Practice - SolutionDocumento6 pagineMidterm Exam 1 Practice - SolutionbobtanlaNessuna valutazione finora

- Forex For CAIIBDocumento6 pagineForex For CAIIBkushalnadekarNessuna valutazione finora

- Minggu 11 Chapter 14 Inflation and Price ChangeDocumento29 pagineMinggu 11 Chapter 14 Inflation and Price ChangePutriska RazaniNessuna valutazione finora

- Currency Exchange Rates: 1 Usd 7 Yen 1USD 6 Yen Price/Base BDT/USD 85/1. 87/1, 83/1Documento31 pagineCurrency Exchange Rates: 1 Usd 7 Yen 1USD 6 Yen Price/Base BDT/USD 85/1. 87/1, 83/1mostakNessuna valutazione finora

- Sample TestDocumento9 pagineSample Teststudunt100% (2)

- 5b Chapter 7 - Exchange RateDocumento73 pagine5b Chapter 7 - Exchange Rateاشرينكيل مسونكيلNessuna valutazione finora

- How to calculate retirement savings needs using a spreadsheetDocumento49 pagineHow to calculate retirement savings needs using a spreadsheetUntung PriambodoNessuna valutazione finora

- Macro đề thiDocumento6 pagineMacro đề thitranquyduong1102Nessuna valutazione finora

- Real Exchange Rates, Hedging, Speculation and ArbitrageDocumento11 pagineReal Exchange Rates, Hedging, Speculation and ArbitragemostakNessuna valutazione finora

- Understanding Foreign Exchange QuotationsDocumento12 pagineUnderstanding Foreign Exchange QuotationsGulshan KumarNessuna valutazione finora

- Engineering Economics CH 4Documento42 pagineEngineering Economics CH 4karim kobeissiNessuna valutazione finora

- U6018+Practice+Midterm+Exam Spring+2022 SolsDocumento6 pagineU6018+Practice+Midterm+Exam Spring+2022 SolsKaren QNessuna valutazione finora

- 2 Parity ConditionsDocumento7 pagine2 Parity ConditionsNaomi LyngdohNessuna valutazione finora

- Lecture 5: Inflation: Engineering EconomyDocumento37 pagineLecture 5: Inflation: Engineering EconomyQed VioNessuna valutazione finora

- Mba50 Wa4 Key 202223Documento7 pagineMba50 Wa4 Key 202223serepasfNessuna valutazione finora

- Forex Forecasting Vital for Multinational CorporationsDocumento8 pagineForex Forecasting Vital for Multinational CorporationsSimba MashiriNessuna valutazione finora

- Measure of InflationDocumento28 pagineMeasure of InflationdannyNessuna valutazione finora

- PS7 Primera ParteDocumento5 paginePS7 Primera PartethomasNessuna valutazione finora

- TVM Chapter 6 Key ConceptsDocumento27 pagineTVM Chapter 6 Key ConceptsMahe990Nessuna valutazione finora

- ABC Bank currency arbitrage profit calculationDocumento9 pagineABC Bank currency arbitrage profit calculationfaisalharaNessuna valutazione finora

- Intuition Behind The Present Value RuleDocumento34 pagineIntuition Behind The Present Value RuleAbhishek MishraNessuna valutazione finora

- 1 Foreign Exchange Markets - IDocumento8 pagine1 Foreign Exchange Markets - INaomi LyngdohNessuna valutazione finora

- Finals Preparation Notes - Forex Markets and Interest RatesDocumento24 pagineFinals Preparation Notes - Forex Markets and Interest RatesbenNessuna valutazione finora

- Lesson 2.1 Foreign Exchange MarketDocumento19 pagineLesson 2.1 Foreign Exchange Marketashu1286Nessuna valutazione finora

- Understanding Returns: Absolute Return, CAGR, IRR Etc: What Is Return or Return On Investment?Documento13 pagineUnderstanding Returns: Absolute Return, CAGR, IRR Etc: What Is Return or Return On Investment?IndranilGhoshNessuna valutazione finora

- Exercises International FinanceDocumento15 pagineExercises International FinanceGiulia ChistéNessuna valutazione finora

- Lecture 4Documento29 pagineLecture 4Tayyab AbbasNessuna valutazione finora

- Engeco Chap 04 - The Time Value of MoneyDocumento27 pagineEngeco Chap 04 - The Time Value of Moneyjivie300998Nessuna valutazione finora

- Capital Markets and InstitutionsDocumento32 pagineCapital Markets and InstitutionsNicoleNessuna valutazione finora

- INTERNATIONAL FINANCE FORUMULASDocumento17 pagineINTERNATIONAL FINANCE FORUMULASMileth Xiomara Ramirez GomezNessuna valutazione finora

- PPA ExcercisesDocumento10 paginePPA ExcercisesJuan Pablo GarciaNessuna valutazione finora

- Ch.16 OutlineDocumento26 pagineCh.16 OutlinehappybeansssNessuna valutazione finora

- The Time Value of MoneyDocumento98 pagineThe Time Value of MoneyNathaniel YbanezNessuna valutazione finora

- Total Points: 20, Time: 20 Min: 2. Define Interlocking Directorates. How Are They Perceived in The SWM and inDocumento5 pagineTotal Points: 20, Time: 20 Min: 2. Define Interlocking Directorates. How Are They Perceived in The SWM and inFolk BluesNessuna valutazione finora

- AusBond Currency Hedging MethodologyDocumento10 pagineAusBond Currency Hedging MethodologyPedro MarquesNessuna valutazione finora

- 7 Int Parity RelationshipDocumento40 pagine7 Int Parity RelationshipumangNessuna valutazione finora

- Unit - 3 Forex MarketDocumento4 pagineUnit - 3 Forex MarketRavi SistaNessuna valutazione finora

- 6 International Parity Relationships & Forecasting Foreign Exchange RatesDocumento35 pagine6 International Parity Relationships & Forecasting Foreign Exchange RatesRicha ChauhanNessuna valutazione finora

- FINA3020 Question Bank Solutions PDFDocumento27 pagineFINA3020 Question Bank Solutions PDFTrinh Phan Thị NgọcNessuna valutazione finora

- Chapter 4 - Determinants of FX Rates: Last LectureDocumento8 pagineChapter 4 - Determinants of FX Rates: Last LecturejamilkhannNessuna valutazione finora

- BBFH308 - International Finance-2Documento6 pagineBBFH308 - International Finance-2Simba MashiriNessuna valutazione finora

- Understanding Money: Compound Interest (C.I) (P (1+r/100) T - P)Documento4 pagineUnderstanding Money: Compound Interest (C.I) (P (1+r/100) T - P)Ajay CyrilNessuna valutazione finora

- Key Concepts of Finance: Understanding MoneyDocumento4 pagineKey Concepts of Finance: Understanding MoneyAkshay HemanthNessuna valutazione finora

- Handbook of Capital Recovery (CR) Factors: European EditionDa EverandHandbook of Capital Recovery (CR) Factors: European EditionNessuna valutazione finora

- Aradhana SrivastavaDocumento2 pagineAradhana SrivastavaAnkit SethNessuna valutazione finora

- AC86VH Confirmed: Booking Reference Status Date of BookingDocumento1 paginaAC86VH Confirmed: Booking Reference Status Date of BookingAnkit SethNessuna valutazione finora

- HR Employee Contact DetailsDocumento2 pagineHR Employee Contact DetailsAnkit SethNessuna valutazione finora

- Maruti Suzuki India LimitedDocumento3 pagineMaruti Suzuki India LimitedAnkit SethNessuna valutazione finora

- Communication Project 1Documento4 pagineCommunication Project 1Ankit SethNessuna valutazione finora

- Tata Vs HyundaiDocumento49 pagineTata Vs HyundaiAnkit SethNessuna valutazione finora

- Dell PCDocumento26 pagineDell PCAnkit SethNessuna valutazione finora

- Accredited Consultants - Eligibility CriteriaDocumento1 paginaAccredited Consultants - Eligibility CriteriaAnkit SethNessuna valutazione finora

- The Basis of Market Segmentation: A Critical Review of LiteratureDocumento11 pagineThe Basis of Market Segmentation: A Critical Review of LiteratureAnkit SethNessuna valutazione finora

- Cluster customers using K-Means analysisDocumento7 pagineCluster customers using K-Means analysisAnkit SethNessuna valutazione finora

- 7 PsDocumento58 pagine7 PsAnkit SethNessuna valutazione finora

- Consume ErDocumento26 pagineConsume ErAnkit SethNessuna valutazione finora

- Brand Post 2Documento6 pagineBrand Post 2Ankit SethNessuna valutazione finora

- A Study On The Effect of Working Capital On The Firm'S Profitability of InfosysDocumento11 pagineA Study On The Effect of Working Capital On The Firm'S Profitability of InfosysDr Abhijit ChakrabortyNessuna valutazione finora

- Consolidate Banking SistemDocumento104 pagineConsolidate Banking SistemandreeavasiuNessuna valutazione finora

- (Agogue) - E Auction (Phy Possession) - SALE NOTICE PUBLICATION DRAFTDocumento3 pagine(Agogue) - E Auction (Phy Possession) - SALE NOTICE PUBLICATION DRAFTSaurabh KapurNessuna valutazione finora

- NYSEDocumento2 pagineNYSEkokabNessuna valutazione finora

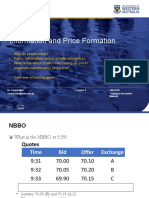

- Information and Price FormationDocumento36 pagineInformation and Price FormationDylan AdrianNessuna valutazione finora

- The Emerging Indian Investing Landcape Amitabh SinghiDocumento37 pagineThe Emerging Indian Investing Landcape Amitabh SinghiZheng YuanNessuna valutazione finora

- Project For BikramDocumento83 pagineProject For Bikramchi005Nessuna valutazione finora

- Dewata Raya Ep 3Documento2 pagineDewata Raya Ep 3Betta UcupNessuna valutazione finora

- Country Risk Analysis Techniques and FactorsDocumento37 pagineCountry Risk Analysis Techniques and FactorsKibria UtshobNessuna valutazione finora

- Benaim, Dodgson, Kainth - An Arbitrage-Free Method For Smile Extrapolation - 2009Documento10 pagineBenaim, Dodgson, Kainth - An Arbitrage-Free Method For Smile Extrapolation - 2009Slavi GeorgievNessuna valutazione finora

- Tables of Content of The ProjectDocumento70 pagineTables of Content of The ProjectShiv GowdaNessuna valutazione finora

- Common Stocks, Uncommon Profits by Phil Fisher - Review by Henrik AnderssonDocumento1 paginaCommon Stocks, Uncommon Profits by Phil Fisher - Review by Henrik AnderssonaxiosbibliosNessuna valutazione finora

- Open Market Operation-2Documento10 pagineOpen Market Operation-2Arslan AshrafNessuna valutazione finora

- Currency Hedging: Currency Hedging Is The Use of Financial Instruments, Called Derivative Contracts, ToDocumento3 pagineCurrency Hedging: Currency Hedging Is The Use of Financial Instruments, Called Derivative Contracts, Tovivekananda RoyNessuna valutazione finora

- About PSEDocumento19 pagineAbout PSEDianna LabayaniNessuna valutazione finora

- R37 Valuation and Analysis Q Bank PDFDocumento14 pagineR37 Valuation and Analysis Q Bank PDFZidane KhanNessuna valutazione finora

- A Project Report On Study of Mutual Fund With Respect To Systematic Investment PlanDocumento84 pagineA Project Report On Study of Mutual Fund With Respect To Systematic Investment PlanNeeraj BaghelNessuna valutazione finora

- Counter TradeDocumento499 pagineCounter TradeVaalu MuthuNessuna valutazione finora

- Nptel: Infrastructure Finance - Video CourseDocumento3 pagineNptel: Infrastructure Finance - Video CourseGaneshNessuna valutazione finora

- JM Institute of Technologies: Duration: 1 Hr. MM: 50Documento2 pagineJM Institute of Technologies: Duration: 1 Hr. MM: 50Rahul NigamNessuna valutazione finora

- FM-Module 3 Act1&2Documento3 pagineFM-Module 3 Act1&2Erica XaoNessuna valutazione finora

- Major Regulatory Bodies in Indian Financial SystemDocumento2 pagineMajor Regulatory Bodies in Indian Financial SystemPooja TripathiNessuna valutazione finora

- AssignmentDocumento18 pagineAssignmentBidur KhanalNessuna valutazione finora

- Safari - Aug 9, 2019 at 7:13 AMDocumento1 paginaSafari - Aug 9, 2019 at 7:13 AMMikaela SamonteNessuna valutazione finora