Potrebbero piacerti anche

- Administrative Pricing Mechanism (APM)Documento14 pagineAdministrative Pricing Mechanism (APM)Amber Chourasia50% (2)

- CH 2 Cost-Volume-Profit RelationshipsDocumento24 pagineCH 2 Cost-Volume-Profit RelationshipsMona ElzaherNessuna valutazione finora

- GP AnalysisDocumento25 pagineGP Analysismiles1280Nessuna valutazione finora

- Marginal Costing NotesDocumento22 pagineMarginal Costing Notesmd tabishNessuna valutazione finora

- BS&WDocumento3 pagineBS&WThomas KerlNessuna valutazione finora

- Production Planning Via Integer Linear ProgrammingDocumento15 pagineProduction Planning Via Integer Linear ProgrammingmarianaNessuna valutazione finora

- Optimizing Combustion ControlsDocumento5 pagineOptimizing Combustion ControlsskluxNessuna valutazione finora

- Oil Price Elasticities and Oil Price Fluctuations: International Finance Discussion PapersDocumento60 pagineOil Price Elasticities and Oil Price Fluctuations: International Finance Discussion PapersprdyumnNessuna valutazione finora

- Strategic Managemnt SeminarDocumento62 pagineStrategic Managemnt SeminarAthira AnuNessuna valutazione finora

- Optimisation Problems (I)Documento2 pagineOptimisation Problems (I)Ahasa FarooqNessuna valutazione finora

- 3.sales Variance AnalysisDocumento38 pagine3.sales Variance Analysiskamasuke hegdeNessuna valutazione finora

- Management Accounting AssignmentDocumento21 pagineManagement Accounting AssignmentAadi KaushikNessuna valutazione finora

- Advanced Approach For Residue FCC - Residue FCC AdditivesDocumento7 pagineAdvanced Approach For Residue FCC - Residue FCC Additivessaleh4060Nessuna valutazione finora

- Standard Costing and Variance Analysis: Fall 2007 CrossonDocumento20 pagineStandard Costing and Variance Analysis: Fall 2007 CrossonBernard SalongaNessuna valutazione finora

- CH 8Documento16 pagineCH 8emanmamdouh596Nessuna valutazione finora

- Target Costing Presentation FinalDocumento57 pagineTarget Costing Presentation FinalMr Dampha100% (1)

- Control Emissions From Refinery FlaresDocumento35 pagineControl Emissions From Refinery FlaresAli YousefNessuna valutazione finora

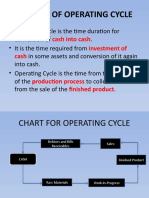

- Concept of Operating Cycle: Cash Into Cash Investment of CashDocumento6 pagineConcept of Operating Cycle: Cash Into Cash Investment of CashVenket RamanaNessuna valutazione finora

- Variable Production Overhead Variance (VPOH)Documento9 pagineVariable Production Overhead Variance (VPOH)Wee Han ChiangNessuna valutazione finora

- Module IV - Working Capital ManagementDocumento50 pagineModule IV - Working Capital ManagementAshwin DholeNessuna valutazione finora

- Refining Margin Supplement OMRAUG 12SEP2012Documento30 pagineRefining Margin Supplement OMRAUG 12SEP2012Won JangNessuna valutazione finora

- Total Loss ControlDocumento6 pagineTotal Loss ControlCalleb ZuvaNessuna valutazione finora

- Cost ManagementDocumento18 pagineCost ManagementGeo Rublico ManilaNessuna valutazione finora

- Lecture-1 Inventory Control IntroductionDocumento44 pagineLecture-1 Inventory Control IntroductionHOD MEC BVC Engineering Colelge OdalarevuNessuna valutazione finora

- Overhead VariancesDocumento11 pagineOverhead VariancesDanica VillaganteNessuna valutazione finora

- Lecture 5: Interest Rate Risk (Part I) : DR Lixiong Guo Semester 2, 2015Documento31 pagineLecture 5: Interest Rate Risk (Part I) : DR Lixiong Guo Semester 2, 2015studentNessuna valutazione finora

- Contribution MarginDocumento4 pagineContribution MarginjibranqqNessuna valutazione finora

- International FInanceDocumento3 pagineInternational FInanceJemma JadeNessuna valutazione finora

- MCS Assignment - 3Documento13 pagineMCS Assignment - 3MIRAL PATELNessuna valutazione finora

- CH 13Documento28 pagineCH 13ReneeNessuna valutazione finora

- Finance Assignment InstructionDocumento7 pagineFinance Assignment InstructionJe-Ta CllNessuna valutazione finora

- Cost Volume Profit Analysis Lecture NotesDocumento34 pagineCost Volume Profit Analysis Lecture NotesAra Reyna D. Mamon-DuhaylungsodNessuna valutazione finora

- Transfer Pricing CH 22Documento5 pagineTransfer Pricing CH 22prachi aroraNessuna valutazione finora

- Lecture 2: Exchange Rates and The Foreign Exchange Market: TopicsDocumento79 pagineLecture 2: Exchange Rates and The Foreign Exchange Market: TopicsSalvio MachaNessuna valutazione finora

- The Journal of Energy and Development: "Crude Oil Market Risk Evaluations Under The Presence of The COVID-19 Pandemic,"Documento22 pagineThe Journal of Energy and Development: "Crude Oil Market Risk Evaluations Under The Presence of The COVID-19 Pandemic,"The International Research Center for Energy and Economic Development (ICEED)Nessuna valutazione finora

- Application of Facility Management Concepts in Sports Facilities PDFDocumento13 pagineApplication of Facility Management Concepts in Sports Facilities PDFAndrew ShishkoNessuna valutazione finora

- Short Term Hedging, Long Term Vertical IntegrationDocumento41 pagineShort Term Hedging, Long Term Vertical IntegrationZorance75Nessuna valutazione finora

- PPT-4 Parity Conditions and Currency ForecastingDocumento42 paginePPT-4 Parity Conditions and Currency ForecastingKamal KantNessuna valutazione finora

- Chapter 7Documento53 pagineChapter 7Baby KhorNessuna valutazione finora

- BM Introduction To BankingDocumento36 pagineBM Introduction To BankingNatasha OliviaNessuna valutazione finora

- Financial Derivatives: Prof. Scott JoslinDocumento49 pagineFinancial Derivatives: Prof. Scott Joslinarnav100% (2)

- 324 - International Parity ConditionsDocumento49 pagine324 - International Parity ConditionsTamuna BibiluriNessuna valutazione finora

- Setting Profit Margin For BiddingDocumento2 pagineSetting Profit Margin For BiddingMAGED MOHMMED AHMED QASEMNessuna valutazione finora

- BAT - For Emission of RefineriesDocumento185 pagineBAT - For Emission of Refineriesbiondimi66Nessuna valutazione finora

- Petroleum Refining Operations: Key Issues, Advances, and OpportunitiesDocumento10 paginePetroleum Refining Operations: Key Issues, Advances, and OpportunitiesMarbel VldNessuna valutazione finora

- Case Analysis On IOCLDocumento12 pagineCase Analysis On IOCLRaoul Savio GomesNessuna valutazione finora

- Characterization and Modeling of Crude Oil Desalting Plant by A Statistically Design ApproachDocumento8 pagineCharacterization and Modeling of Crude Oil Desalting Plant by A Statistically Design ApproachangelkindlyNessuna valutazione finora

- Chapter Five: The Financial Statements of Banks and Their Principal CompetitorsDocumento58 pagineChapter Five: The Financial Statements of Banks and Their Principal CompetitorsYoussef Youssef Ahmed Abdelmeguid Abdel LatifNessuna valutazione finora

- Marginal CostingDocumento22 pagineMarginal CostingbelladoNessuna valutazione finora

- Operating and Financial LeverageDocumento36 pagineOperating and Financial LeverageKiena AnthiaNessuna valutazione finora

- FCC Fractionation For LCODocumento10 pagineFCC Fractionation For LCOBehnam RahzaniNessuna valutazione finora

- Breakeven AnalysisDocumento4 pagineBreakeven AnalysisSaugata Shovan HaiderNessuna valutazione finora

- Linear Program 1Documento52 pagineLinear Program 1ChaOs_Air75% (4)

- 3-EPA Flare Activity Overview-Dickens, BrianDocumento37 pagine3-EPA Flare Activity Overview-Dickens, BrianAhmed MaaroofNessuna valutazione finora

- Cost-Volume-Profit Relationships: Principles of Management AccountingDocumento16 pagineCost-Volume-Profit Relationships: Principles of Management Accountingsyed haider ali shah shah100% (1)

- Kinder Morgan Presentation To Investors at Credit Suisse June 2014Documento36 pagineKinder Morgan Presentation To Investors at Credit Suisse June 2014dracutcivicwatchNessuna valutazione finora

- Transfer PricingDocumento35 pagineTransfer PricingsivaNessuna valutazione finora

- Transfer PricingDocumento9 pagineTransfer PricingGalbraith Kevin NongrumNessuna valutazione finora

- Alternative Methods of Transfer PricingDocumento4 pagineAlternative Methods of Transfer PricingRyan FranklinNessuna valutazione finora

- Transfer PricingDocumento20 pagineTransfer PricingsachinbscagriNessuna valutazione finora

- Management Control SystemDocumento49 pagineManagement Control SystembijoyendasNessuna valutazione finora

- Management Control and Operational ControlDocumento3 pagineManagement Control and Operational ControlbijoyendasNessuna valutazione finora

- BudgetDocumento3 pagineBudgetbijoyendasNessuna valutazione finora

- Port & LogisticsDocumento32 paginePort & LogisticsbijoyendasNessuna valutazione finora

- Port & LogisticsDocumento32 paginePort & LogisticsbijoyendasNessuna valutazione finora

- Ramdev Food Products PVT LTDDocumento32 pagineRamdev Food Products PVT LTDbijoyendas100% (2)

- Business Plan FurnaceDocumento18 pagineBusiness Plan FurnacebijoyendasNessuna valutazione finora

- TOA Reviewer (UE) - Bank Reconcilation PDFDocumento1 paginaTOA Reviewer (UE) - Bank Reconcilation PDFjhallylipmaNessuna valutazione finora

- List of SAP Status CodesDocumento19 pagineList of SAP Status Codesmajid D71% (7)

- 2189XXXXXXXXX316721 09 2019Documento3 pagine2189XXXXXXXXX316721 09 2019Sumit ChakrabortyNessuna valutazione finora

- Examples Transfer PricingDocumento15 pagineExamples Transfer PricingRajat RathNessuna valutazione finora

- Managerial Level-1: Part - Aweightage 20%Documento6 pagineManagerial Level-1: Part - Aweightage 20%fawad aslamNessuna valutazione finora

- FX4Cash CorporatesDocumento4 pagineFX4Cash CorporatesAmeerHamsa0% (1)

- She Bsa 4-2Documento7 pagineShe Bsa 4-2Justine GuilingNessuna valutazione finora

- Contract For Services Law240Documento5 pagineContract For Services Law240Izwan Muhamad100% (1)

- Tally MCQ 1Documento11 pagineTally MCQ 1rs0100100% (4)

- Rural Marketing ManualDocumento21 pagineRural Marketing ManualRahul Verma RVNessuna valutazione finora

- Poliform Kitchens Aust (855KB) PDFDocumento12 paginePoliform Kitchens Aust (855KB) PDFsage_9290% (1)

- ISO 9001 CertificateDocumento7 pagineISO 9001 CertificateMoidu ThavottNessuna valutazione finora

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Documento1 paginaTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Ganesh PrabuNessuna valutazione finora

- Project Appraisal FinanceDocumento20 pagineProject Appraisal Financecpsandeepgowda6828Nessuna valutazione finora

- Treasurer'S Affidavit: Republic of The Philippines) City of Taguig) S.S. Metro Manila)Documento2 pagineTreasurer'S Affidavit: Republic of The Philippines) City of Taguig) S.S. Metro Manila)Maria Andres50% (2)

- Macro 03Documento381 pagineMacro 03subroto36100% (1)

- RPT Case DigestsDocumento71 pagineRPT Case Digestscarlota ann lafuenteNessuna valutazione finora

- Cirque de Soleil Case StudyDocumento2 pagineCirque de Soleil Case StudyAnand Prasad0% (1)

- Essential Qualities of A Sales PersonDocumento6 pagineEssential Qualities of A Sales PersonSTREAM123456789Nessuna valutazione finora

- Frauds in Indian Banking SectorDocumento5 pagineFrauds in Indian Banking SectorPayal Ambhore100% (1)

- CH 8Documento64 pagineCH 8Anonymous 0cdKGOBBNessuna valutazione finora

- Products Services FCPO EnglishDocumento16 pagineProducts Services FCPO EnglishKhairul AdhaNessuna valutazione finora

- Chapter 1 Global ServiceDocumento23 pagineChapter 1 Global ServiceRandeep SinghNessuna valutazione finora

- INTERN 1 DefinitionsDocumento2 pagineINTERN 1 DefinitionsJovis MalasanNessuna valutazione finora

- OpinionLab v. Iperceptions Et. Al.Documento34 pagineOpinionLab v. Iperceptions Et. Al.PriorSmartNessuna valutazione finora

- Kabushi Kaisha Isetan Vs IacDocumento2 pagineKabushi Kaisha Isetan Vs IacJudee Anne100% (2)

- Keeney v. Larkin, 4th Cir. (2004)Documento4 pagineKeeney v. Larkin, 4th Cir. (2004)Scribd Government DocsNessuna valutazione finora

- Ker61035 Appd Case01Documento3 pagineKer61035 Appd Case01GeeSungNessuna valutazione finora

- Autobus Vs BautistaDocumento1 paginaAutobus Vs BautistaJoel G. AyonNessuna valutazione finora

- Fundamentals of Corporate Finance 4th Edition Parrino Test BankDocumento35 pagineFundamentals of Corporate Finance 4th Edition Parrino Test BankbrumfieldridleyvipNessuna valutazione finora