Potrebbero piacerti anche

- Case-Security Bank CorpDocumento6 pagineCase-Security Bank CorpFernando VergaraNessuna valutazione finora

- Bank of The Philippine IslandsDocumento5 pagineBank of The Philippine IslandsCaryl Almira SayreNessuna valutazione finora

- Specialization: Human Resources Group: Human Resources Development DivisionDocumento5 pagineSpecialization: Human Resources Group: Human Resources Development DivisionkennethNessuna valutazione finora

- Metrobank - AnalysisDocumento28 pagineMetrobank - AnalysisMeditacio Monto89% (27)

- Metrobank Strama PaperDocumento28 pagineMetrobank Strama PaperAnderei Acantilado67% (9)

- Yes Bank: Prof. Shilpa Chadichal Alliance Business AcademyDocumento17 pagineYes Bank: Prof. Shilpa Chadichal Alliance Business AcademyNihal SinghNessuna valutazione finora

- Metrobank Strama Paper, Group 3/M0531 Strategic Planning and Management: Group 3 Metropolitan Bank and Trust Company (METROBANK)Documento28 pagineMetrobank Strama Paper, Group 3/M0531 Strategic Planning and Management: Group 3 Metropolitan Bank and Trust Company (METROBANK)sheila mae adayaNessuna valutazione finora

- Bank of The Philippine IslandDocumento5 pagineBank of The Philippine IslandAdeline Mangulad MontebonNessuna valutazione finora

- FM 133 Capital-Wps OfficeDocumento10 pagineFM 133 Capital-Wps OfficeJade Del MundoNessuna valutazione finora

- Tadifa ReportDocumento28 pagineTadifa ReportBennie AmansecNessuna valutazione finora

- Economic Performance Review of Commercial and Investment Banking in PakistanDocumento16 pagineEconomic Performance Review of Commercial and Investment Banking in PakistanNayab NoumanNessuna valutazione finora

- Chapter 1: Introduction: A. Company BackgroundDocumento30 pagineChapter 1: Introduction: A. Company Backgroundwangyu roqueNessuna valutazione finora

- HRM in IDBI BankDocumento75 pagineHRM in IDBI BankAkshayBorgharkar80% (5)

- PNBDocumento3 paginePNBLove KarenNessuna valutazione finora

- Canara Bank Priority Sector AnalysisDocumento59 pagineCanara Bank Priority Sector AnalysisSoujanya NagarajaNessuna valutazione finora

- My Internship Report Bank Alfalah Islamic Ltd. CompletedDocumento63 pagineMy Internship Report Bank Alfalah Islamic Ltd. Completedanon_512862546Nessuna valutazione finora

- Chapter 1: Introduction: A. Company BackgroundDocumento34 pagineChapter 1: Introduction: A. Company Backgroundwangyu roqueNessuna valutazione finora

- Philippine Bank of CommunicationsDocumento30 paginePhilippine Bank of CommunicationsGab ReyesNessuna valutazione finora

- Analysis of Icici and PNB Marketing EssayDocumento13 pagineAnalysis of Icici and PNB Marketing EssayRonald MurphyNessuna valutazione finora

- Table of ContentsDocumento32 pagineTable of ContentsElizabeth KibodyaNessuna valutazione finora

- HDFC BankDocumento50 pagineHDFC BankNikhil TyagiNessuna valutazione finora

- FIIB - CIP - Interim Report: Annexure - IVDocumento18 pagineFIIB - CIP - Interim Report: Annexure - IVRavi SinghNessuna valutazione finora

- Yes Bank: Prof. Shilpa Chadichal Alliance Business AcademyDocumento17 pagineYes Bank: Prof. Shilpa Chadichal Alliance Business AcademyEkta Luciferisious SharmaNessuna valutazione finora

- Bank of The Philippine Islands-CisDocumento9 pagineBank of The Philippine Islands-CisKershey SalacNessuna valutazione finora

- Introduction To Bank AlfalahDocumento39 pagineIntroduction To Bank AlfalahUsman ButtNessuna valutazione finora

- BPIDocumento2 pagineBPIApril Jane CornelioNessuna valutazione finora

- The Use of Financial Inclusion Data Country Case Study - Philippines PDFDocumento7 pagineThe Use of Financial Inclusion Data Country Case Study - Philippines PDFshau ildeNessuna valutazione finora

- Identify & Evaluate Marketing OpportunitiesDocumento9 pagineIdentify & Evaluate Marketing Opportunitiesmsohail_2004Nessuna valutazione finora

- Executive SummaryDocumento6 pagineExecutive SummaryAsad BilalNessuna valutazione finora

- Bank AlfahaDocumento94 pagineBank AlfahamcbNessuna valutazione finora

- Presentation Report On Union Bank of India: Submitted ToDocumento23 paginePresentation Report On Union Bank of India: Submitted ToAniket PawasheNessuna valutazione finora

- Philippine Saving Bank (Shortened As Psbank or Abbreurated As PSB)Documento2 paginePhilippine Saving Bank (Shortened As Psbank or Abbreurated As PSB)Afesoj BelirNessuna valutazione finora

- SME TrifoldsDocumento2 pagineSME TrifoldsRavi KhandgeNessuna valutazione finora

- In Partial Fulfilment For Human Resource Management AY 2020-20201, First SemesterDocumento14 pagineIn Partial Fulfilment For Human Resource Management AY 2020-20201, First Semestermatteo rossiNessuna valutazione finora

- Final StramaDocumento74 pagineFinal StramaRalphDesiEscueta94% (36)

- Banking IndustryDocumento33 pagineBanking IndustryJOHN PAUL DOROINNessuna valutazione finora

- Banking Sector: 1.1 Introduction To The TaskDocumento23 pagineBanking Sector: 1.1 Introduction To The TaskRIYA CHALKENessuna valutazione finora

- E-Portfolio of A Financial InstitutionDocumento9 pagineE-Portfolio of A Financial InstitutionLeah Grace DeatrasNessuna valutazione finora

- Group e - MetrobankDocumento24 pagineGroup e - Metrobankhanna jeanNessuna valutazione finora

- Assessment 1 in Financial Management: Central Bicol State University of AgricultureDocumento8 pagineAssessment 1 in Financial Management: Central Bicol State University of AgricultureDan Louie San AgustinNessuna valutazione finora

- Final StramaDocumento75 pagineFinal StramaChristian Jay Patiño Orpano100% (1)

- METROBANKDocumento28 pagineMETROBANKMa Teresa Angelyn100% (5)

- Module 4 - Commercial BanksDocumento9 pagineModule 4 - Commercial BanksRizell Mae PruebasNessuna valutazione finora

- Company Profile of Bank MandiriDocumento2 pagineCompany Profile of Bank MandiriTee's O-RamaNessuna valutazione finora

- Jayesh Gupta PDF 1Documento12 pagineJayesh Gupta PDF 1Jayesh GuptaNessuna valutazione finora

- Customer Satisfaction of Prime BankDocumento42 pagineCustomer Satisfaction of Prime BankShuvro DattaNessuna valutazione finora

- Transcript of MetrobankDocumento6 pagineTranscript of MetrobankChessarie AngelesNessuna valutazione finora

- PSBDocumento16 paginePSBXtorm TrooperNessuna valutazione finora

- Public BankDocumento4 paginePublic BankKhairul AslamNessuna valutazione finora

- PRE4Documento105 paginePRE4J. BautistaNessuna valutazione finora

- Audit of BanksDocumento6 pagineAudit of BanksLouella Vea HernandezNessuna valutazione finora

- Banco de Oro or Bdo Unibank IncDocumento4 pagineBanco de Oro or Bdo Unibank IncJcel JcelNessuna valutazione finora

- Vision and MissionDocumento10 pagineVision and MissionMun YeeNessuna valutazione finora

- UNO Digital Bank Annual Report 2022Documento65 pagineUNO Digital Bank Annual Report 2022tuando.bongbongNessuna valutazione finora

- Soft Copy Internship Report of Sadia ChowdhuryDocumento52 pagineSoft Copy Internship Report of Sadia ChowdhuryEligible Bachelor75% (4)

- UB - LeadersDocumento7 pagineUB - LeadersAlaiza Maas LanonNessuna valutazione finora

- The Philippine National Bank Was Established As A GovernmentDocumento7 pagineThe Philippine National Bank Was Established As A GovernmentIris Valerie Bontia CabunilasNessuna valutazione finora

- Marketing of Banking-ServicesDocumento25 pagineMarketing of Banking-ServicesImran ShaikhNessuna valutazione finora

- Specialized IndustriesDocumento107 pagineSpecialized IndustriesCristine Joyce ValdezNessuna valutazione finora

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Da EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Nessuna valutazione finora

- KohlerDocumento79 pagineKohlerAnthony RoyupaNessuna valutazione finora

- Aifs/ Finance Case StudyDocumento5 pagineAifs/ Finance Case StudyMohit Kumar GuptaNessuna valutazione finora

- Beta Management CompanyDocumento8 pagineBeta Management Companymanishverma56470% (1)

- American Chemical Corp (ACC) Case Study Executive SummaryDocumento1 paginaAmerican Chemical Corp (ACC) Case Study Executive SummaryNatasha SuddhiNessuna valutazione finora

- American Chemical Corp (ACC) Case Study Executive SummaryDocumento1 paginaAmerican Chemical Corp (ACC) Case Study Executive SummaryNatasha SuddhiNessuna valutazione finora

- HRM10eChap16 - Employee Rihgts and DisciplineDocumento35 pagineHRM10eChap16 - Employee Rihgts and DisciplineAnthony RoyupaNessuna valutazione finora

- Financial AnalysisDocumento16 pagineFinancial AnalysisAnthony RoyupaNessuna valutazione finora

- HRM10eChap09 - Training Human ResourcesDocumento33 pagineHRM10eChap09 - Training Human ResourcesAnthony RoyupaNessuna valutazione finora

- HRM10eChap01 - Changing Nature of HRMDocumento21 pagineHRM10eChap01 - Changing Nature of HRMAnthony RoyupaNessuna valutazione finora

- Human Resource Management: Managing Employee BenefitsDocumento31 pagineHuman Resource Management: Managing Employee BenefitsAnthony RoyupaNessuna valutazione finora

- HRM10eChap12 - Compensation Strategies and PracticesDocumento42 pagineHRM10eChap12 - Compensation Strategies and PracticesAnthony RoyupaNessuna valutazione finora

- HRM10eChap13 - Variable Pay Executive CompensationDocumento24 pagineHRM10eChap13 - Variable Pay Executive CompensationAnthony RoyupaNessuna valutazione finora

- Human Resource Management: Health, Safety, and SecurityDocumento25 pagineHuman Resource Management: Health, Safety, and SecurityJoko DewotoNessuna valutazione finora

- Human Resource Management Human Resource ManagementDocumento38 pagineHuman Resource Management Human Resource ManagementDheeraaj GeadamNessuna valutazione finora

- HRM10eChap10 - Career and HR DevelopmentDocumento28 pagineHRM10eChap10 - Career and HR DevelopmentAnthony RoyupaNessuna valutazione finora

- HRM10eChap09 - Training Human ResourcesDocumento33 pagineHRM10eChap09 - Training Human ResourcesAnthony RoyupaNessuna valutazione finora

- HRM10eChap08 - Selecting, Placing Human ResourcesDocumento45 pagineHRM10eChap08 - Selecting, Placing Human ResourcesAnthony RoyupaNessuna valutazione finora

- HRM10eChap03 - Individual Performance and RetentionDocumento29 pagineHRM10eChap03 - Individual Performance and RetentionAnthony RoyupaNessuna valutazione finora

- Human Resource Management: Robert L. Mathis John H. JacksonDocumento34 pagineHuman Resource Management: Robert L. Mathis John H. JacksonZeeshan KhanNessuna valutazione finora

- Labor Code: CompensationDocumento1 paginaLabor Code: CompensationAnthony RoyupaNessuna valutazione finora

- HRM10 e Chap 02Documento45 pagineHRM10 e Chap 02Ahmed Cherif WasfyNessuna valutazione finora

- Human Resource Management: Legal Framework For Equal EmploymentDocumento37 pagineHuman Resource Management: Legal Framework For Equal EmploymentfgdgdfgdfgNessuna valutazione finora

- UnionismDocumento31 pagineUnionismAnthony RoyupaNessuna valutazione finora

- Location Planning and AnalysisDocumento15 pagineLocation Planning and AnalysisAnthony RoyupaNessuna valutazione finora

- Student Slides Chapter 14Documento15 pagineStudent Slides Chapter 14Anthony RoyupaNessuna valutazione finora

- CH 01 10th EditionDocumento2 pagineCH 01 10th EditionAnthony RoyupaNessuna valutazione finora

- Production Management FormulasDocumento3 pagineProduction Management FormulasAnthony RoyupaNessuna valutazione finora

- CH 01 10th EditionDocumento2 pagineCH 01 10th EditionAnthony RoyupaNessuna valutazione finora

- Student Slides Chapter 10Documento15 pagineStudent Slides Chapter 10Gaurav WidhaniNessuna valutazione finora

- Student Slides Supplement 15Documento15 pagineStudent Slides Supplement 15Anthony RoyupaNessuna valutazione finora

- CIR Vs LincolnDocumento2 pagineCIR Vs LincolnAmee Bagtang-dapingNessuna valutazione finora

- Analysis of Investor Perception, Apprehension and Decision Making in Indian Stock MarketsDocumento73 pagineAnalysis of Investor Perception, Apprehension and Decision Making in Indian Stock MarketsSunil Goyal50% (4)

- Advisory Agreement Quasi-FinalDocumento28 pagineAdvisory Agreement Quasi-FinalMartineOrangeNessuna valutazione finora

- Credit Insurance PPT BasicDocumento8 pagineCredit Insurance PPT Basicshikha82Nessuna valutazione finora

- Chapter 16Documento11 pagineChapter 16John Michael GalleneroNessuna valutazione finora

- Vcnotes 05 09 2017Documento72 pagineVcnotes 05 09 2017MohammadRahemanNessuna valutazione finora

- SCB Tariff 2021Documento15 pagineSCB Tariff 2021Fuaad DodooNessuna valutazione finora

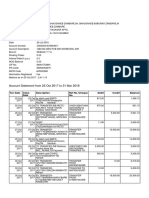

- Wells Fargo Statement - June 2022Documento5 pagineWells Fargo Statement - June 2022pradeep yadavNessuna valutazione finora

- SWOT Analysis of Banking IndustryDocumento13 pagineSWOT Analysis of Banking IndustryApoorv94% (18)

- MicroLead - PHB - TK4 - Own Agent Network - BM - ENG PDFDocumento55 pagineMicroLead - PHB - TK4 - Own Agent Network - BM - ENG PDFNambasa JoyceNessuna valutazione finora

- Enterprise Risk - May 2010Documento44 pagineEnterprise Risk - May 20103S Media PublicationsNessuna valutazione finora

- Vivere CatalogueDocumento33 pagineVivere CatalogueGalih Baskara AjiNessuna valutazione finora

- Indian Money MarketDocumento0 pagineIndian Money MarketaasisranjanNessuna valutazione finora

- 424 434Documento2 pagine424 434Kim Balauag100% (1)

- Sales ContractDocumento5 pagineSales ContractDemoBriliyanto0% (1)

- CV Sadiq 2010Documento4 pagineCV Sadiq 2010Tijani Raheemot AjedoyinNessuna valutazione finora

- Wa0025Documento8 pagineWa0025SachinZambareNessuna valutazione finora

- Ingenico Ict220 Users Manual 120304Documento40 pagineIngenico Ict220 Users Manual 120304dermordNessuna valutazione finora

- Product Development AgreementDocumento15 pagineProduct Development Agreementhuangpeter55Nessuna valutazione finora

- Assignment BancassuranceDocumento10 pagineAssignment BancassuranceGetrude Mvududu100% (4)

- Central BankingDocumento29 pagineCentral BankingMarcy ViernesGalasinao MaguigadCabacunganNessuna valutazione finora

- Deposist AccountDocumento6 pagineDeposist AccountwaheedarifNessuna valutazione finora

- Osman Ali Yousif: Job DescriptionDocumento7 pagineOsman Ali Yousif: Job DescriptionAnonymous K8uhurNessuna valutazione finora

- Nacif V White-SorensonDocumento46 pagineNacif V White-SorensonDinSFLANessuna valutazione finora

- Credit AppraisalDocumento46 pagineCredit AppraisalApekshaNessuna valutazione finora

- MCBDocumento16 pagineMCBTariq SiddiqNessuna valutazione finora

- DebtCapitalMarkets TheBasics AsiaEditionDocumento28 pagineDebtCapitalMarkets TheBasics AsiaEditionVivek AgNessuna valutazione finora

- 1.1history of BankingDocumento18 pagine1.1history of BankingHarika KollatiNessuna valutazione finora

- Chapter 12 - Payables - QuestionsDocumento3 pagineChapter 12 - Payables - Questionsmariam simonyanNessuna valutazione finora

- Role of It in BankingDocumento5 pagineRole of It in BankingSamaira SheikhNessuna valutazione finora