Potrebbero piacerti anche

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5795)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1091)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Country Profile Official Name in Other Official LanguagesDocumento53 pagineCountry Profile Official Name in Other Official LanguagesMarnelli MabiniNessuna valutazione finora

- For Billing Enquiry Visit Https://selfcare - Tikona.inDocumento2 pagineFor Billing Enquiry Visit Https://selfcare - Tikona.inVivek Jain100% (1)

- The Impact of Service Quality Determinants On Customer Satisfaction A Study of Bank of Bhutan Limited in GEDU Town, BhutanDocumento12 pagineThe Impact of Service Quality Determinants On Customer Satisfaction A Study of Bank of Bhutan Limited in GEDU Town, Bhutanarcherselevators100% (1)

- Samahan NG Manggagawa Sa Hanjin Shipyard V Hanjin Heavy IndustriesDocumento3 pagineSamahan NG Manggagawa Sa Hanjin Shipyard V Hanjin Heavy IndustriesTippy Dos SantosNessuna valutazione finora

- Dmo 1999-34 PDFDocumento5 pagineDmo 1999-34 PDFJanine Hizon GamillaNessuna valutazione finora

- Minor Project Report On Mild Steel BarsDocumento22 pagineMinor Project Report On Mild Steel BarsPawan KumarNessuna valutazione finora

- (Deloitte) Entrance Test & AnswerDocumento36 pagine(Deloitte) Entrance Test & AnswerLê Quang Trung75% (4)

- Civil Engg Cos List - MajorsDocumento10 pagineCivil Engg Cos List - MajorsGp MishraNessuna valutazione finora

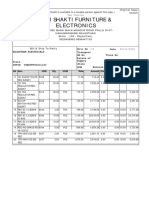

- Shri Shakti Furniture & Electronics: Credit OrginalDocumento1 paginaShri Shakti Furniture & Electronics: Credit OrginalRahul BansalNessuna valutazione finora

- Canara - Epassbook - 2023-11-02 200708.530629Documento95 pagineCanara - Epassbook - 2023-11-02 200708.530629manojsailor855Nessuna valutazione finora

- Effect of Nigerian Border ClosureDocumento5 pagineEffect of Nigerian Border Closuretundescribd1Nessuna valutazione finora

- Project Capstone Abhishek AcharyaDocumento54 pagineProject Capstone Abhishek AcharyaRajan PrasadNessuna valutazione finora

- Sole Proprietary: According To B.D. Wheeler, "The Sole Proprietorship Is That From of BusinessDocumento12 pagineSole Proprietary: According To B.D. Wheeler, "The Sole Proprietorship Is That From of Businessapi-19729505Nessuna valutazione finora

- Hamina Pipa, Bez Ostale EkipeDocumento35 pagineHamina Pipa, Bez Ostale EkipeIsmar HadzicNessuna valutazione finora

- Chapter 2Documento14 pagineChapter 2Pantaleon EdilNessuna valutazione finora

- Short Note On LIC and Insurance SectorDocumento37 pagineShort Note On LIC and Insurance Sectorappliedjobz50% (2)

- EcDocumento2 pagineEcArgie FlorendoNessuna valutazione finora

- Micro Finance AppendicesDocumento42 pagineMicro Finance AppendicesJiya PatelNessuna valutazione finora

- Pangasinan State University: Student Profile FormDocumento1 paginaPangasinan State University: Student Profile Formroger quinitoNessuna valutazione finora

- Colonialism and The Countryside: Exploring Official ArchivesDocumento47 pagineColonialism and The Countryside: Exploring Official Archivesmonika singh100% (3)

- Purchase Order BIG BULLDocumento2 paginePurchase Order BIG BULLAnita JaiswalNessuna valutazione finora

- PEZA Reportorial RequirementsDocumento4 paginePEZA Reportorial RequirementsMV FadsNessuna valutazione finora

- Latihan Soal 02 BingDocumento9 pagineLatihan Soal 02 BingCiki Ciki100% (1)

- OligopolyDocumento8 pagineOligopolyYashsav Gupta100% (1)

- Pakistan Next Generation Report Part 02Documento23 paginePakistan Next Generation Report Part 02ZafarH100% (1)

- Isint BrochureDocumento12 pagineIsint BrochureCristian GuerraNessuna valutazione finora

- 6 Stocks Double Investors' Wealth Since Last Ganesh ChaturthiDocumento8 pagine6 Stocks Double Investors' Wealth Since Last Ganesh ChaturthiJayaprakash MuthuvatNessuna valutazione finora

- PNB Overseas Directory PDFDocumento7 paginePNB Overseas Directory PDFReah Liza Padaoan SalvinoNessuna valutazione finora

- Worksheet 1 - IXDocumento2 pagineWorksheet 1 - IXJa HahaNessuna valutazione finora

- Induction Training 182Documento1 paginaInduction Training 182Satyam mishraNessuna valutazione finora