Potrebbero piacerti anche

- Piping Drawings Basics: N.P.TodkarDocumento37 paginePiping Drawings Basics: N.P.Todkaredgar_glezav100% (2)

- Inventory ControlDocumento25 pagineInventory ControlSuja Pillai100% (1)

- Ca ProjDocumento6 pagineCa ProjSuja PillaiNessuna valutazione finora

- Introduction To HmsDocumento20 pagineIntroduction To HmsSuja Pillai100% (1)

- I TDocumento14 pagineI TSuja PillaiNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Private Foundation TemplateDocumento4 paginePrivate Foundation TemplateGee Penn100% (5)

- Manappuram General Finance & Leasing Ltd. (Gold Loan)Documento14 pagineManappuram General Finance & Leasing Ltd. (Gold Loan)Rushabh ShahNessuna valutazione finora

- Model On Small Scale Cashew ProcessingDocumento20 pagineModel On Small Scale Cashew Processingrajesh67% (3)

- 9-Death of A Salesman Test 2Documento15 pagine9-Death of A Salesman Test 2ErlGeordieNessuna valutazione finora

- Chapter 29 Macroeconomics HWDocumento6 pagineChapter 29 Macroeconomics HWMỹ Dung PhạmNessuna valutazione finora

- Loan Policy of Uco Bank For Retail SectorDocumento22 pagineLoan Policy of Uco Bank For Retail SectorAnurag BohraNessuna valutazione finora

- Research Proposal by Pragya Jaiswal - Edited VersionDocumento8 pagineResearch Proposal by Pragya Jaiswal - Edited Versionpragya jaiswalNessuna valutazione finora

- Car WC - Petronas Refinery and Petrochemical Corporation SDN BHD Unijaya Industri SDN BHDDocumento6 pagineCar WC - Petronas Refinery and Petrochemical Corporation SDN BHD Unijaya Industri SDN BHDniedanorNessuna valutazione finora

- Santos Vs CA - 120820 - August 1, 2000 - JDocumento7 pagineSantos Vs CA - 120820 - August 1, 2000 - Jlala reyesNessuna valutazione finora

- FNAN 321: (COMPANY NAME) (Company Address)Documento7 pagineFNAN 321: (COMPANY NAME) (Company Address)Shehryaar AhmedNessuna valutazione finora

- A Study of Non Performing Assets in Bank of BarodaDocumento88 pagineA Study of Non Performing Assets in Bank of BarodaShubham MayekarNessuna valutazione finora

- Assignement 3 - 24 GSIS v. Heirs of CaballeroDocumento2 pagineAssignement 3 - 24 GSIS v. Heirs of CaballeropatrickNessuna valutazione finora

- Mrunal (Economic Survey Ch7) International Trade, FTA, PTA, ASIDE, E-BRC, CEPA Vs CECA Difference Explained MrunalDocumento21 pagineMrunal (Economic Survey Ch7) International Trade, FTA, PTA, ASIDE, E-BRC, CEPA Vs CECA Difference Explained MrunalHamdard BoparaiNessuna valutazione finora

- Ethics in FinanceDocumento30 pagineEthics in FinanceSujit Dutta MazumdarNessuna valutazione finora

- Debt RestructuringDocumento2 pagineDebt RestructuringVicong PogiNessuna valutazione finora

- Withholding Tax Invoices in Oracle APDocumento8 pagineWithholding Tax Invoices in Oracle APvijaymselvamNessuna valutazione finora

- Core Banking Partner GuideDocumento19 pagineCore Banking Partner GuideClint JacobNessuna valutazione finora

- G.R. No. 97753 August 10, 1992 CALTEX (PHILIPPINES), INC., Petitioner, Court of Appeals and Security Bank and Trust Company, RespondentsDocumento17 pagineG.R. No. 97753 August 10, 1992 CALTEX (PHILIPPINES), INC., Petitioner, Court of Appeals and Security Bank and Trust Company, RespondentsJucca Noreen SalesNessuna valutazione finora

- AC EXAM PDF 2019 - LIC Assistant Main Exam (Jan-Dec14th) by AffairsCloud PDFDocumento309 pagineAC EXAM PDF 2019 - LIC Assistant Main Exam (Jan-Dec14th) by AffairsCloud PDFRajaram RNessuna valutazione finora

- Fil Assurance Vs NavaDocumento5 pagineFil Assurance Vs NavamansikiaboNessuna valutazione finora

- The Case of The Returned CollateralDocumento18 pagineThe Case of The Returned CollateralJoyce Ann Sosa60% (5)

- Employee Compensation and BenefitsDocumento46 pagineEmployee Compensation and BenefitsJuanito Cabiles JrNessuna valutazione finora

- AJ ResumeDocumento3 pagineAJ ResumeCristin StefenNessuna valutazione finora

- Components of Indian Financial SystemDocumento10 pagineComponents of Indian Financial Systemvikas1only100% (2)

- 1602Documento2 pagine1602Rhizz RamirezNessuna valutazione finora

- UK Home Office: Set (O) FormDocumento15 pagineUK Home Office: Set (O) FormUK_HomeOfficeNessuna valutazione finora

- Economics Nov 2009 Eng MemoDocumento30 pagineEconomics Nov 2009 Eng Memokubayik7402Nessuna valutazione finora

- Mid Term Exam MCQs For 5530Documento6 pagineMid Term Exam MCQs For 5530Amy WangNessuna valutazione finora

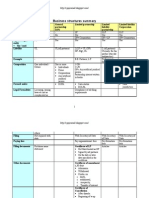

- Business Structures SummaryDocumento5 pagineBusiness Structures SummaryMrudula V.100% (2)

- Non Current Liabilities San Carlos CollegeDocumento12 pagineNon Current Liabilities San Carlos CollegeRowbby Gwyn50% (2)