Potrebbero piacerti anche

- Dividend Investing for Beginners & DummiesDa EverandDividend Investing for Beginners & DummiesValutazione: 5 su 5 stelle5/5 (1)

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideDa EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNessuna valutazione finora

- Chapter 16 Employee BenefitsDocumento56 pagineChapter 16 Employee BenefitsHammad Ahmad100% (27)

- Chapter 12 Government GrantsDocumento19 pagineChapter 12 Government GrantsHammad Ahmad82% (11)

- Advanced Financial Management - 20MBAFM306: Department of Management Studies, JNNCE, ShivamoggaDocumento16 pagineAdvanced Financial Management - 20MBAFM306: Department of Management Studies, JNNCE, ShivamoggaDrusti M S100% (1)

- Chapter 3 Deferred TaxDocumento47 pagineChapter 3 Deferred TaxHammad Ahmad100% (1)

- Chapter9 - Noncurrentassetsheldforsale2008 - Gripping IFRS 2008 by ICAPDocumento22 pagineChapter9 - Noncurrentassetsheldforsale2008 - Gripping IFRS 2008 by ICAPFalah Ud Din SheryarNessuna valutazione finora

- Check, DefinedDocumento17 pagineCheck, DefinedMykee NavalNessuna valutazione finora

- Dividend Investing 101 Create Long Term Income from DividendsDa EverandDividend Investing 101 Create Long Term Income from DividendsNessuna valutazione finora

- Dividend Policy of Reliance Industries Itd.Documento24 pagineDividend Policy of Reliance Industries Itd.rohit280273% (11)

- Chapter 19 Foreign Currency TransactionsDocumento23 pagineChapter 19 Foreign Currency TransactionsHammad AhmadNessuna valutazione finora

- Pfau Sustainable Withdrawal Rates WhitepaperDocumento14 paginePfau Sustainable Withdrawal Rates WhitepaperJohn Koh100% (1)

- Chapter 5 Property Plant and EquipmentDocumento41 pagineChapter 5 Property Plant and EquipmentHammad Ahmad100% (8)

- Common and Preferred StockDocumento14 pagineCommon and Preferred StockMuhammad AyazNessuna valutazione finora

- Textbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingDa EverandTextbook of Urgent Care Management: Chapter 46, Urgent Care Center FinancingNessuna valutazione finora

- Risk Bearing Documents in International TradeDocumento8 pagineRisk Bearing Documents in International TradeSukrut BoradeNessuna valutazione finora

- Dividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementDa EverandDividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementNessuna valutazione finora

- ch15 2e Kieso TBDocumento46 paginech15 2e Kieso TBMohammed Khouli100% (3)

- Best Investing Books of All TimeDocumento10 pagineBest Investing Books of All Timejohn vladimirNessuna valutazione finora

- Ultimate Reward Current Account GuideDocumento112 pagineUltimate Reward Current Account GuideRyan BucuNessuna valutazione finora

- Dividend PolicyDocumento47 pagineDividend PolicyniovaleyNessuna valutazione finora

- Chapter 7 Intangible AssetsDocumento34 pagineChapter 7 Intangible AssetsHammad Ahmad100% (5)

- R23 Dividends and Share Repurchases IFT NotesDocumento20 pagineR23 Dividends and Share Repurchases IFT NotesAdnan MasoodNessuna valutazione finora

- CIMA F2 Course Notes PDFDocumento293 pagineCIMA F2 Course Notes PDFganNessuna valutazione finora

- Indonesia Economic Update 2023 q2Documento18 pagineIndonesia Economic Update 2023 q2Jaeysen CanilyNessuna valutazione finora

- Aik Qatra Khoon by Ismat ChughtaiDocumento247 pagineAik Qatra Khoon by Ismat ChughtaiHammad AhmadNessuna valutazione finora

- Chapter 6 Property Plant and Equipment ModelsDocumento41 pagineChapter 6 Property Plant and Equipment ModelsHammad Ahmad77% (13)

- NEGO 103 Case DigestsDocumento34 pagineNEGO 103 Case DigestskbongcoNessuna valutazione finora

- Chapter23 - Earningspershare2008 - Gripping IFRS 2008 by ICAPDocumento30 pagineChapter23 - Earningspershare2008 - Gripping IFRS 2008 by ICAPFalah Ud Din SheryarNessuna valutazione finora

- Appropriated P & L DetailsDocumento10 pagineAppropriated P & L DetailsM Usman AslamNessuna valutazione finora

- Retained EarningsDocumento28 pagineRetained EarningsKen MaulionNessuna valutazione finora

- FM II Chapter 1Documento12 pagineFM II Chapter 1Addisu TadesseNessuna valutazione finora

- Dilutive Securities and Earnings Per ShareDocumento11 pagineDilutive Securities and Earnings Per ShareAdhiyanto PLNessuna valutazione finora

- Dividend Policy of Reliance Industries SwatiDocumento24 pagineDividend Policy of Reliance Industries SwatiYashasvi KothariNessuna valutazione finora

- Dividend DecisionDocumento5 pagineDividend DecisionRishika SinghNessuna valutazione finora

- Accounting For and Reporting of Preference SharesDocumento19 pagineAccounting For and Reporting of Preference SharesAis Syang DyaNessuna valutazione finora

- Libby 4ce Solutions Manual - Ch12Documento43 pagineLibby 4ce Solutions Manual - Ch127595522Nessuna valutazione finora

- Earning Per ShareDocumento22 pagineEarning Per Sharekimuli FreddieNessuna valutazione finora

- Final AssignmentDocumento51 pagineFinal AssignmentNaveeda RiazNessuna valutazione finora

- Different Types of DividendDocumento7 pagineDifferent Types of DividendAnshul Mehrotra100% (1)

- 10 Chapter UGLEDocumento26 pagine10 Chapter UGLEMahek AroraNessuna valutazione finora

- Lesson 6 - Statement of Financial Position (Part 2)Documento9 pagineLesson 6 - Statement of Financial Position (Part 2)yana jungNessuna valutazione finora

- Dividends: 1.1 Definition of DividendDocumento11 pagineDividends: 1.1 Definition of Dividendshiza sheikhNessuna valutazione finora

- Dividends: 1.1 Definition of DividendDocumento11 pagineDividends: 1.1 Definition of Dividendshiza sheikhNessuna valutazione finora

- Company AccountingDocumento7 pagineCompany AccountingMsuBrainBoxNessuna valutazione finora

- Dividend Decisions: Unit 5Documento41 pagineDividend Decisions: Unit 5Fara HameedNessuna valutazione finora

- Special Topics - Written ReportDocumento5 pagineSpecial Topics - Written ReportMary Maddie JenningsNessuna valutazione finora

- FIASDocumento4 pagineFIASTika GusmawarniNessuna valutazione finora

- Fa Unit 4Documento13 pagineFa Unit 4VTNessuna valutazione finora

- Corporate Securites Classes of Corporate Securities: Ownership Securities and Creditor Ship SecuritiesDocumento11 pagineCorporate Securites Classes of Corporate Securities: Ownership Securities and Creditor Ship SecuritiesSanjeev KumarNessuna valutazione finora

- Financial Management II 2020: Aims and Objectives After Completing This Chapter, You Should Have A Good Understanding ofDocumento15 pagineFinancial Management II 2020: Aims and Objectives After Completing This Chapter, You Should Have A Good Understanding ofSintu TalefeNessuna valutazione finora

- Chapter 18 IRMDocumento33 pagineChapter 18 IRMWissamMouakNessuna valutazione finora

- Dividend Decision Part 1Documento10 pagineDividend Decision Part 1avinashchoudhary2043Nessuna valutazione finora

- Dividend Policy (S)Documento3 pagineDividend Policy (S)Nahian ShalimNessuna valutazione finora

- Corporate Accounting 1: III Semester BBADocumento57 pagineCorporate Accounting 1: III Semester BBAAR Ananth Rohith BhatNessuna valutazione finora

- Financial Management Ii: Chapter 1dividend Policy and TheoryDocumento54 pagineFinancial Management Ii: Chapter 1dividend Policy and TheoryhabtamuNessuna valutazione finora

- True or FalseDocumento7 pagineTrue or FalseColline ZoletaNessuna valutazione finora

- IA3 Mod 4 REDocumento12 pagineIA3 Mod 4 REjulia4razoNessuna valutazione finora

- Ifrs Chapter TwoDocumento25 pagineIfrs Chapter TwoGeorge YabaNessuna valutazione finora

- Acctba2 Lecture - Lump Sum LiquidationDocumento10 pagineAcctba2 Lecture - Lump Sum Liquidationmia_catapangNessuna valutazione finora

- Dividends & Its TypesDocumento3 pagineDividends & Its TypesMD KamaalNessuna valutazione finora

- Module 8 - Shareholders' Equity, Retained Earnings, and DividendsDocumento10 pagineModule 8 - Shareholders' Equity, Retained Earnings, and DividendsLaurio, Genebabe TagubarasNessuna valutazione finora

- CH 6Documento91 pagineCH 6EyobedNessuna valutazione finora

- Dividend: HistoryDocumento20 pagineDividend: Historyanup bhattNessuna valutazione finora

- Ca 2Documento16 pagineCa 2Parth SharmaNessuna valutazione finora

- Unit 4 - Company Accounts Lecture NotesDocumento12 pagineUnit 4 - Company Accounts Lecture NotesTan TaylorNessuna valutazione finora

- Unit - 3: Dividend DecisionDocumento34 pagineUnit - 3: Dividend DecisionChethan.sNessuna valutazione finora

- Dividend - ClassificationsDocumento13 pagineDividend - ClassificationsAdanechNessuna valutazione finora

- Chapter 17 1Documento26 pagineChapter 17 1Diệu Linh NguyễnNessuna valutazione finora

- IAS 32 Financial Instrument PresentationDocumento8 pagineIAS 32 Financial Instrument PresentationMehdi BelkadiNessuna valutazione finora

- An Overview On Financial Statements and Ratio AnalysisDocumento10 pagineAn Overview On Financial Statements and Ratio AnalysissachinoilNessuna valutazione finora

- Non-Current LiabilityDocumento9 pagineNon-Current Liabilityjameson EbuñaNessuna valutazione finora

- Chapter - 2 Conceptual Framework of DividendDocumento36 pagineChapter - 2 Conceptual Framework of DividendMadhavasadasivan PothiyilNessuna valutazione finora

- Chapter 21 Financial InstrumentsDocumento21 pagineChapter 21 Financial InstrumentsHammad Ahmad67% (3)

- Chapter24 Cashflowstatements2008Documento21 pagineChapter24 Cashflowstatements2008Marium Rafiq100% (2)

- Chapter 17 Provisions and Post Balance Sheet EventsDocumento29 pagineChapter 17 Provisions and Post Balance Sheet EventsHammad Ahmad100% (1)

- IAS 18 - Revenue RecognitionDocumento26 pagineIAS 18 - Revenue Recognitionwakemeup143Nessuna valutazione finora

- Chapter 18 Policies Estimates and ErrorsDocumento28 pagineChapter 18 Policies Estimates and ErrorsHammad Ahmad100% (1)

- Chapter 13 LeaseDocumento29 pagineChapter 13 LeaseHammad Ahmad100% (2)

- Chapter14 - Leases Lessors2008 - Gripping IFRS 2008 by ICAPDocumento27 pagineChapter14 - Leases Lessors2008 - Gripping IFRS 2008 by ICAPFalah Ud Din SheryarNessuna valutazione finora

- Borrowing CostsDocumento19 pagineBorrowing CostsIrfan100% (20)

- Financial Analysis - Ratio AnalysisDocumento26 pagineFinancial Analysis - Ratio AnalysisHuzaifa Ahmed100% (2)

- Ifrs 36 (Impairement of Assets)Documento33 pagineIfrs 36 (Impairement of Assets)Irfan100% (4)

- IAS 40 - Investment PropertyDocumento16 pagineIAS 40 - Investment Propertywakemeup143Nessuna valutazione finora

- IAS 2 - InventoriesDocumento42 pagineIAS 2 - Inventorieswakemeup143100% (1)

- IAS 12 TaxationDocumento30 pagineIAS 12 Taxationwakemeup143Nessuna valutazione finora

- Chapter1 The Pillars 2008Documento57 pagineChapter1 The Pillars 2008Umair ArifNessuna valutazione finora

- InvoicemmDocumento1 paginaInvoicemmankithmallelaNessuna valutazione finora

- Regulations On Fdi, Adr, GDR, Idr, Fii &ecbDocumento59 pagineRegulations On Fdi, Adr, GDR, Idr, Fii &ecbAvinash SinghNessuna valutazione finora

- 604 ch3Documento72 pagine604 ch3Hazel Grace SantosNessuna valutazione finora

- Individual Assignment Financial ManagementDocumento17 pagineIndividual Assignment Financial ManagementUtheu Budhi Susetyo100% (1)

- JAIIB-PPB-Free Mock Test - JAN 2022Documento3 pagineJAIIB-PPB-Free Mock Test - JAN 2022kanarendranNessuna valutazione finora

- Payback Period Year IC FC TVC TC Gross Benefits Net Benefits YearsDocumento2 paginePayback Period Year IC FC TVC TC Gross Benefits Net Benefits YearsIzhiel Mai PadillaNessuna valutazione finora

- Foreign Exchange MarketDocumento3 pagineForeign Exchange MarketVasim ShaikhNessuna valutazione finora

- FINA1904 - ALL Weitzel - Spring 2019Documento11 pagineFINA1904 - ALL Weitzel - Spring 2019JamesNessuna valutazione finora

- 4th Accounts Dec 2021Documento2 pagine4th Accounts Dec 2021KillingNessuna valutazione finora

- Accounting Standards and Company Audit AnswersDocumento9 pagineAccounting Standards and Company Audit AnswersrinshaNessuna valutazione finora

- Act Broadband AprilDocumento2 pagineAct Broadband AprilAshaNessuna valutazione finora

- Submitted By: Anmol Hindwani (Pgsf1907) : Bank Performance AnalysisDocumento20 pagineSubmitted By: Anmol Hindwani (Pgsf1907) : Bank Performance AnalysisSurbhî GuptaNessuna valutazione finora

- R NPV IRR 0% 5.000 15.24% 5% 2.988 10% 1.372 15% 0.056 20% - 1.028 25% - 1.932 30% - 2.693Documento1 paginaR NPV IRR 0% 5.000 15.24% 5% 2.988 10% 1.372 15% 0.056 20% - 1.028 25% - 1.932 30% - 2.693mattNessuna valutazione finora

- Xi Akl 3 - Lembar Kerja Memproses Entry JurnalDocumento25 pagineXi Akl 3 - Lembar Kerja Memproses Entry JurnalKeshya MantovanniNessuna valutazione finora

- Draft Version - Article On Cross Collateralization-C1Documento6 pagineDraft Version - Article On Cross Collateralization-C1Rohit Anand DasNessuna valutazione finora

- The Bank of KhyberDocumento76 pagineThe Bank of KhyberWaqas KhanNessuna valutazione finora

- Case Study-Istisna NewDocumento2 pagineCase Study-Istisna Newmali27a767100% (1)

- Futures - Meaning, Types, Mechanism, SEBI GuidelinesDocumento49 pagineFutures - Meaning, Types, Mechanism, SEBI GuidelinesKARISHMAAT67% (6)

- Bus 5111: Financial Management: Written Assignment Unit 1 Ratios CalculationDocumento5 pagineBus 5111: Financial Management: Written Assignment Unit 1 Ratios CalculationCharles IrikefeNessuna valutazione finora

- End of Season: Spring Summer 2021Documento29 pagineEnd of Season: Spring Summer 2021Abdaud RasyidNessuna valutazione finora

- FXOM Definitions EN PDFDocumento10 pagineFXOM Definitions EN PDFDenni SeptianNessuna valutazione finora

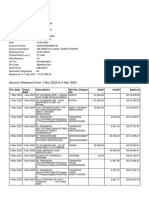

- Account Statement From 1 Mar 2023 To 4 Mar 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocumento2 pagineAccount Statement From 1 Mar 2023 To 4 Mar 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancesameer bawejaNessuna valutazione finora

- Topic Three: Developing A Business Plan: William Amone Lecturer, Gulu UniversityDocumento14 pagineTopic Three: Developing A Business Plan: William Amone Lecturer, Gulu UniversityInnocent OdagaNessuna valutazione finora