Potrebbero piacerti anche

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- L 1 Mock V 12014 December Am SolutionsDocumento76 pagineL 1 Mock V 12014 December Am SolutionsFatma Hassan ElxeniNessuna valutazione finora

- Cagny 2019 PDFDocumento67 pagineCagny 2019 PDFaz2690Nessuna valutazione finora

- NBP Annual Report 2018 PDFDocumento311 pagineNBP Annual Report 2018 PDFaz2690Nessuna valutazione finora

- Income Tax Ordinance LatestDocumento609 pagineIncome Tax Ordinance LatestInformation ServicesNessuna valutazione finora

- Systems Limited PDFDocumento4 pagineSystems Limited PDFaz2690Nessuna valutazione finora

- Annex III Poverty PDFDocumento2 pagineAnnex III Poverty PDFaz2690Nessuna valutazione finora

- RIF2017 Jean-Paul Agon EN PDFDocumento92 pagineRIF2017 Jean-Paul Agon EN PDFaz2690Nessuna valutazione finora

- General Electric Company Case Study: March 2014Documento27 pagineGeneral Electric Company Case Study: March 2014Clint Jan SalvañaNessuna valutazione finora

- Ford and GMDocumento12 pagineFord and GMaz2690100% (2)

- Bp-Statistical-Review-Of World Energy-2017-Approximate-Conversion-Factors PDFDocumento4 pagineBp-Statistical-Review-Of World Energy-2017-Approximate-Conversion-Factors PDFingbarragan87Nessuna valutazione finora

- 2016 17 Schowalter Tesla PDFDocumento72 pagine2016 17 Schowalter Tesla PDFaz2690Nessuna valutazione finora

- 2012 0802 - World - Bank - StrategyDocumento16 pagine2012 0802 - World - Bank - StrategyAziz.3251Nessuna valutazione finora

- Toyota: A Case StudyDocumento18 pagineToyota: A Case Studysuredotcom007Nessuna valutazione finora

- Exxon Sustainability2 PDFDocumento68 pagineExxon Sustainability2 PDFAmber AhluwaliaNessuna valutazione finora

- BP Energy Outlook 2015 PDFDocumento98 pagineBP Energy Outlook 2015 PDFaz2690Nessuna valutazione finora

- General Electric Company Case Study: March 2014Documento27 pagineGeneral Electric Company Case Study: March 2014Clint Jan SalvañaNessuna valutazione finora

- Synopsis BDocumento11 pagineSynopsis BAnonymous s8Iz5MNessuna valutazione finora

- The Walt Disney Company - A Corporate Strategy Analysis PDFDocumento29 pagineThe Walt Disney Company - A Corporate Strategy Analysis PDFaz2690Nessuna valutazione finora

- Rise and Fall of Nokia (2014)Documento14 pagineRise and Fall of Nokia (2014)Amit71% (7)

- Caso The Rise and Fall of BlackBerryDocumento10 pagineCaso The Rise and Fall of BlackBerryCris Tóbal0% (1)

- Ford and GMDocumento12 pagineFord and GMaz2690100% (2)

- The Walt Disney Company - A Corporate Strategy Analysis PDFDocumento29 pagineThe Walt Disney Company - A Corporate Strategy Analysis PDFaz2690Nessuna valutazione finora

- General Electric Company Case Study: March 2014Documento27 pagineGeneral Electric Company Case Study: March 2014Clint Jan SalvañaNessuna valutazione finora

- Learning From Corporate MistakesDocumento11 pagineLearning From Corporate Mistakesraja2jaya100% (2)

- China New Silk RouteDocumento8 pagineChina New Silk RouteRafaei SantosNessuna valutazione finora

- Luca F Procter Gamble Case StudyDocumento32 pagineLuca F Procter Gamble Case Studyaz2690Nessuna valutazione finora

- Wal Mart CaseStudyDocumento36 pagineWal Mart CaseStudyerwin26100% (2)

- FinQuiz Level1Mock2016Version1JuneAMQuestions PDFDocumento39 pagineFinQuiz Level1Mock2016Version1JuneAMQuestions PDFNevena VasiljevicNessuna valutazione finora

- China New Silk RouteDocumento8 pagineChina New Silk RouteRafaei SantosNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

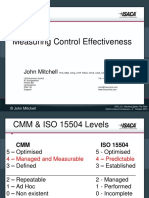

- Measuring Control Effectiveness - John MitchellDocumento19 pagineMeasuring Control Effectiveness - John MitchellShah Maqsumul Masrur TanviNessuna valutazione finora

- Statistical Interpretation of Predictive Factors of Head Impact Kinematics in Traumatic Brain InjuryDocumento4 pagineStatistical Interpretation of Predictive Factors of Head Impact Kinematics in Traumatic Brain InjuryDeepsNessuna valutazione finora

- Bmec 003 Week 1 ModuleDocumento9 pagineBmec 003 Week 1 ModuleJohn Andrei ValenzuelaNessuna valutazione finora

- Scope Insensitivity in Child's Health Risk Reduction: A Comparison of Damage Schedule and Choice Experiment MethodsDocumento32 pagineScope Insensitivity in Child's Health Risk Reduction: A Comparison of Damage Schedule and Choice Experiment MethodsJose DGNessuna valutazione finora

- Learning-Plan-in-Law-144 - Labor Law 1 - SJARVDocumento7 pagineLearning-Plan-in-Law-144 - Labor Law 1 - SJARVSteps RolsNessuna valutazione finora

- Project SpaceDocumento5 pagineProject Spaceapi-490238812Nessuna valutazione finora

- Marking Scheme AgriDocumento3 pagineMarking Scheme AgriDa bert100% (1)

- Term Paper On DBLDocumento19 pagineTerm Paper On DBLSaif HassanNessuna valutazione finora

- Outcome Measures January 2019Documento39 pagineOutcome Measures January 2019Ashwini KatareNessuna valutazione finora

- Apj Abdul KalamDocumento16 pagineApj Abdul Kalamamanblr12100% (2)

- The Heart Man StoryDocumento2 pagineThe Heart Man StorygbakukenjuNessuna valutazione finora

- MKTG1100 Chapter 4Documento28 pagineMKTG1100 Chapter 4Marcus YapNessuna valutazione finora

- Review Jurnal Internasional Yamin - Id.enDocumento4 pagineReview Jurnal Internasional Yamin - Id.enFendi PradanaNessuna valutazione finora

- NRSP Annual Report 2019 20Documento98 pagineNRSP Annual Report 2019 20عادل حسین عابدNessuna valutazione finora

- Chapter No. One Introduction: 1.1 Introduction To The StudyDocumento44 pagineChapter No. One Introduction: 1.1 Introduction To The StudyTahir ShahNessuna valutazione finora

- T TESTDocumento24 pagineT TESTanmolgarg129Nessuna valutazione finora

- Jadwal NEAT SG 1Documento5 pagineJadwal NEAT SG 1sangkertadiNessuna valutazione finora

- Be Winter 2022Documento1 paginaBe Winter 2022Dhruv DesaiNessuna valutazione finora

- The Concept of Packaging LogisticsDocumento31 pagineThe Concept of Packaging LogisticsvenkatryedullaNessuna valutazione finora

- Igcse Art Coursework ChecklistDocumento7 pagineIgcse Art Coursework Checklistdgmtutlfg100% (1)

- Book - OT Manager - Chap 34 Supervising Other DisciplinesDocumento9 pagineBook - OT Manager - Chap 34 Supervising Other DisciplinesWhitney JosephNessuna valutazione finora

- Internship Learning PlanDocumento2 pagineInternship Learning Planapi-284839367Nessuna valutazione finora

- Resume - Huzaifa Khan (P)Documento1 paginaResume - Huzaifa Khan (P)Huzaifa KhanNessuna valutazione finora

- Thesis Summary OutlineDocumento4 pagineThesis Summary Outlinekatiegulleylittlerock100% (2)

- Developing A Global Vision Through Marketing ResearchDocumento27 pagineDeveloping A Global Vision Through Marketing ResearchJamesNessuna valutazione finora

- Job InterviewDocumento13 pagineJob InterviewHajnal SzilasiNessuna valutazione finora

- Sanet ST 9811582807Documento286 pagineSanet ST 9811582807WertonNessuna valutazione finora

- The Impact of MOBA Games On The Mathematical Skills of High School StudentsDocumento5 pagineThe Impact of MOBA Games On The Mathematical Skills of High School StudentswilbertgiuseppedeguzmanNessuna valutazione finora

- Maritime Logistics A Guide To Contemporary Shipping and Port Management (351-400)Documento50 pagineMaritime Logistics A Guide To Contemporary Shipping and Port Management (351-400)ZaNessuna valutazione finora

- Unit 3 Mind MappingDocumento6 pagineUnit 3 Mind MappingFeeroj PathanNessuna valutazione finora