Potrebbero piacerti anche

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5795)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Ashok Leyland SEA FORMATDocumento68 pagineAshok Leyland SEA FORMATVi KraNessuna valutazione finora

- Steps of An Internal AuditDocumento3 pagineSteps of An Internal AuditDownload100% (1)

- Basic Cooperative Course (BCC)Documento75 pagineBasic Cooperative Course (BCC)Troy Eric O. Cordero100% (1)

- Preamble To Bill of QuantitiesDocumento1 paginaPreamble To Bill of QuantitiesAziz ul HakeemNessuna valutazione finora

- Basic Concepts in Business Policy and StrategyDocumento3 pagineBasic Concepts in Business Policy and Strategylance100% (1)

- Introduction To Project ManagementDocumento58 pagineIntroduction To Project ManagementAnonymous kwi5IqtWJNessuna valutazione finora

- MAS CVP Analysis HandoutsDocumento8 pagineMAS CVP Analysis HandoutsMartha Nicole MaristelaNessuna valutazione finora

- Sachin Tomar-Iciob MietDocumento3 pagineSachin Tomar-Iciob MietSachin TomarNessuna valutazione finora

- 31 - Vinoya Vs NLRCDocumento8 pagine31 - Vinoya Vs NLRCArthur YamatNessuna valutazione finora

- Enterprise Structure & Master DataDocumento10 pagineEnterprise Structure & Master DatapaiashokNessuna valutazione finora

- Experience Letter LayoutDocumento1 paginaExperience Letter Layoutscribdaj08Nessuna valutazione finora

- FIN 335 UNCW Phase III NotesDocumento23 pagineFIN 335 UNCW Phase III NotesMonydit SantinoNessuna valutazione finora

- NOA Current Affairs Book AghazetaleemDocumento308 pagineNOA Current Affairs Book Aghazetaleem24 Asad AhmadNessuna valutazione finora

- VatDocumento13 pagineVatJohn Derek GarreroNessuna valutazione finora

- Agile Manifesto Has Values and PrinciplesDocumento2 pagineAgile Manifesto Has Values and Principlesबाबा आउलोद्दीनNessuna valutazione finora

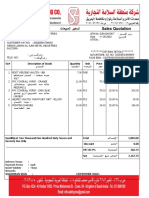

- Sales Quotation: Salesman Sign: Customer SignDocumento1 paginaSales Quotation: Salesman Sign: Customer SignjacobNessuna valutazione finora

- Aibek ZhanybekovDocumento4 pagineAibek ZhanybekovАзаматNessuna valutazione finora

- Operations Management MCQs - Types of Production - MCQs ClubDocumento7 pagineOperations Management MCQs - Types of Production - MCQs ClubPranoy SarkarNessuna valutazione finora

- Institute of Innovation in Technology and ManagementDocumento51 pagineInstitute of Innovation in Technology and ManagementHarsh GuptaNessuna valutazione finora

- Smart Investors DataDocumento6 pagineSmart Investors DataSamrat SahaNessuna valutazione finora

- Partnership LetterDocumento3 paginePartnership LetterDj ComputersNessuna valutazione finora

- Social ResponsibilityDocumento3 pagineSocial ResponsibilityMonique MalateNessuna valutazione finora

- Bai Tap 1Documento2 pagineBai Tap 1Đinh Đào Tặc100% (1)

- Marketing Plan: Mogu MoguDocumento23 pagineMarketing Plan: Mogu MoguBảo Quí TrầnNessuna valutazione finora

- Lokesh Punj Cvdec2018Documento11 pagineLokesh Punj Cvdec2018LOKESH PUNJNessuna valutazione finora

- Industrial Visit Project OnDocumento33 pagineIndustrial Visit Project OnShreyali ShahNessuna valutazione finora

- Definition of WagesDocumento8 pagineDefinition of WagesCorolla SedanNessuna valutazione finora

- Royal EnfieldDocumento2 pagineRoyal EnfieldGopinath GovindarajNessuna valutazione finora

- FAC1503 - 2023 - Learning Unit 2Documento45 pagineFAC1503 - 2023 - Learning Unit 2Cotton CandyNessuna valutazione finora

- Isilon Product FamilyDocumento7 pagineIsilon Product FamilyrejnanNessuna valutazione finora