Potrebbero piacerti anche

- Sms 6Documento41 pagineSms 6api-3871199Nessuna valutazione finora

- Sms 5Documento35 pagineSms 5api-3871199100% (1)

- Sms 4 PPTRDocumento37 pagineSms 4 PPTRapi-3871199Nessuna valutazione finora

- Sms 3 PPTRDocumento32 pagineSms 3 PPTRapi-3871199Nessuna valutazione finora

- Lecture Notes 3Documento6 pagineLecture Notes 3api-3871199Nessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- QP02Documento11 pagineQP02zakwanmustafa0% (1)

- Case Study On DominoDocumento7 pagineCase Study On Dominodisha_pandey_4Nessuna valutazione finora

- Coding Guidelines-CDocumento71 pagineCoding Guidelines-CKishoreRajuNessuna valutazione finora

- Book LoRa LoRaWAN and Internet of ThingsDocumento140 pagineBook LoRa LoRaWAN and Internet of ThingsNguyễn Hữu HạnhNessuna valutazione finora

- What Is Aggregate DemandqwertDocumento9 pagineWhat Is Aggregate DemandqwertShahana KhanNessuna valutazione finora

- ATH SR5BT DatasheetDocumento1 paginaATH SR5BT DatasheetspeedbeatNessuna valutazione finora

- G6Documento14 pagineG6Arinah RdhNessuna valutazione finora

- Venezuela's Gold Heist - Ebus & MartinelliDocumento18 pagineVenezuela's Gold Heist - Ebus & MartinelliBram EbusNessuna valutazione finora

- Appointment - Letter GaganDocumento10 pagineAppointment - Letter GaganAjay choudharyNessuna valutazione finora

- Azar Mukhtiar Abbasi: Arkad Engineering & ConstructionDocumento4 pagineAzar Mukhtiar Abbasi: Arkad Engineering & ConstructionAnonymous T4xDd4Nessuna valutazione finora

- Implementation of BS 8500 2006 Concrete Minimum Cover PDFDocumento13 pagineImplementation of BS 8500 2006 Concrete Minimum Cover PDFJimmy Lopez100% (1)

- Tales of Mystery Imagination and Humour Edgar Allan Poe PDFDocumento289 pagineTales of Mystery Imagination and Humour Edgar Allan Poe PDFmatildameisterNessuna valutazione finora

- Intel L515 - User - GuLidarDocumento20 pagineIntel L515 - User - GuLidarRich ManNessuna valutazione finora

- Dy DX: NPTEL Course Developer For Fluid Mechanics Dr. Niranjan Sahoo Module 04 Lecture 33 IIT-GuwahatiDocumento7 pagineDy DX: NPTEL Course Developer For Fluid Mechanics Dr. Niranjan Sahoo Module 04 Lecture 33 IIT-GuwahatilawanNessuna valutazione finora

- ISDM - Lab Sheet 02Documento4 pagineISDM - Lab Sheet 02it21083396 Galappaththi S DNessuna valutazione finora

- Engineering MetallurgyDocumento540 pagineEngineering Metallurgymadhuriaddepalli100% (1)

- Chapter 1 - Food Quality Control ProgrammeDocumento75 pagineChapter 1 - Food Quality Control ProgrammeFattah Abu Bakar100% (1)

- Notes in Train Law PDFDocumento11 pagineNotes in Train Law PDFJanica Lobas100% (1)

- PPR 8001Documento1 paginaPPR 8001quangga10091986Nessuna valutazione finora

- PSI 8.8L ServiceDocumento197 paginePSI 8.8L Serviceedelmolina100% (1)

- Abhijit Auditorium Elective Sem 09Documento3 pagineAbhijit Auditorium Elective Sem 09Abhijit Kumar AroraNessuna valutazione finora

- Unix Training ContentDocumento5 pagineUnix Training ContentsathishkumarNessuna valutazione finora

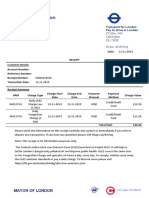

- Transport For London Pay To Drive in London: PO Box 344 Darlington Dl1 9qe TFL - Gov.uk/drivingDocumento1 paginaTransport For London Pay To Drive in London: PO Box 344 Darlington Dl1 9qe TFL - Gov.uk/drivingDanyy MaciucNessuna valutazione finora

- Dislocations and StrenghteningDocumento19 pagineDislocations and StrenghteningAmber WilliamsNessuna valutazione finora

- EconiQ High Voltage Roadmap 1629274842Documento1 paginaEconiQ High Voltage Roadmap 1629274842Daniel CaceresNessuna valutazione finora

- WSM - Ziale - Commercial Law NotesDocumento36 pagineWSM - Ziale - Commercial Law NotesElizabeth Chilufya100% (1)

- BloodDocumento22 pagineBloodGodd LlikeNessuna valutazione finora

- MN502 Lecture 3 Basic CryptographyDocumento45 pagineMN502 Lecture 3 Basic CryptographySajan JoshiNessuna valutazione finora

- Pumpkin Cultivation and PracticesDocumento11 paginePumpkin Cultivation and PracticesGhorpade GsmNessuna valutazione finora

- DM2 0n-1abDocumento6 pagineDM2 0n-1abyus11Nessuna valutazione finora