Potrebbero piacerti anche

- Industry Analysis and Competitive AnalysisDocumento6 pagineIndustry Analysis and Competitive Analysisapi-3716588Nessuna valutazione finora

- 4th ClassDocumento13 pagine4th Classapi-3716588Nessuna valutazione finora

- Retail ConsumerDocumento11 pagineRetail Consumerapi-3716588100% (2)

- Commercial Banking - 1Documento31 pagineCommercial Banking - 1api-3716588Nessuna valutazione finora

- Retail StrategyDocumento27 pagineRetail Strategyapi-3716588100% (17)

- Medium & Long Term FinanceDocumento67 pagineMedium & Long Term Financeapi-3716588100% (2)

- Introduction To RetailDocumento13 pagineIntroduction To Retailapi-3716588100% (2)

- Retail Brand ManagementDocumento8 pagineRetail Brand Managementapi-3716588100% (6)

- Indian Investment AbroadDocumento17 pagineIndian Investment Abroadapi-3716588Nessuna valutazione finora

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Trade FinanceDocumento40 pagineTrade Financeapi-371658880% (5)

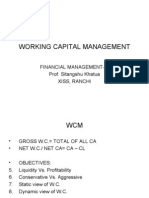

- Working Capital Management: Financial Management - Ii Prof. Sitangshu Khatua Xiss, RanchiDocumento10 pagineWorking Capital Management: Financial Management - Ii Prof. Sitangshu Khatua Xiss, Ranchiapi-3716588Nessuna valutazione finora

- Foreign Investment in IndiaDocumento43 pagineForeign Investment in Indiaapi-3716588100% (2)

- Acma - 7-8Documento8 pagineAcma - 7-8api-3716588Nessuna valutazione finora

- Acma - 9-10Documento3 pagineAcma - 9-10api-3716588Nessuna valutazione finora

- Acma - 3-4Documento4 pagineAcma - 3-4api-3716588Nessuna valutazione finora

- 5 Cust PerceptionsDocumento20 pagine5 Cust Perceptionsapi-3716588100% (2)

- DerivativesDocumento53 pagineDerivativesapi-3716588100% (1)

- Management of Financial Institutions Syllabus 2006-08Documento7 pagineManagement of Financial Institutions Syllabus 2006-08api-3716588Nessuna valutazione finora

- MFI CH 1c (Money MKT & Cap MKT Inst)Documento12 pagineMFI CH 1c (Money MKT & Cap MKT Inst)api-3716588Nessuna valutazione finora

- MFI-Ch1a (Ec Growth & Fin Inst)Documento5 pagineMFI-Ch1a (Ec Growth & Fin Inst)api-3716588Nessuna valutazione finora

- 6 Gap 1Documento10 pagine6 Gap 1api-3716588Nessuna valutazione finora

- 2 Intro To Serv MarDocumento23 pagine2 Intro To Serv Marapi-3716588100% (2)

- MFI CH 1b (Financial System & Fin Inst)Documento4 pagineMFI CH 1b (Financial System & Fin Inst)api-3716588Nessuna valutazione finora

- Commercial BankingDocumento7 pagineCommercial Bankingapi-3716588100% (1)

- ExerciseDocumento2 pagineExerciseapi-3716588Nessuna valutazione finora

- Central Banking System & RBIDocumento50 pagineCentral Banking System & RBIapi-3716588Nessuna valutazione finora

- 1 Course Contents Serv MarDocumento12 pagine1 Course Contents Serv Marapi-3716588100% (2)

- 3rd Class FinDocumento14 pagine3rd Class Finapi-3716588Nessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (890)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Logistics & Supply Chain Challenges at Schneider ElectricDocumento28 pagineLogistics & Supply Chain Challenges at Schneider ElectricSachin MaharajNessuna valutazione finora

- Sustainable Enterprise KPIs and ERP Post AdoptionDocumento7 pagineSustainable Enterprise KPIs and ERP Post AdoptionDaniel GuerreroNessuna valutazione finora

- Planning For LogisticsDocumento399 paginePlanning For LogisticsShashi KanwalNessuna valutazione finora

- Efficient Material Management in HospitalsDocumento72 pagineEfficient Material Management in HospitalsAdnan RAHATNessuna valutazione finora

- Online Grocery Shopping System PDF Documentation PDFDocumento3 pagineOnline Grocery Shopping System PDF Documentation PDFakash mayekar75% (4)

- Just in Time (JIT) Inventory - How Does It WorkDocumento12 pagineJust in Time (JIT) Inventory - How Does It WorkPradeepNessuna valutazione finora

- ID Karakteristik Dan Penanganan Limbah Padat Serta Keluhan Iritasi Kulit Pada PetugDocumento10 pagineID Karakteristik Dan Penanganan Limbah Padat Serta Keluhan Iritasi Kulit Pada Petugfaqih zidnyNessuna valutazione finora

- Ifmis P2P Kenya Supplier Portal Training ManualDocumento30 pagineIfmis P2P Kenya Supplier Portal Training ManualalfredNessuna valutazione finora

- Set 3Documento8 pagineSet 3Debasri DeyNessuna valutazione finora

- Sales and Distribution Management: Prepared By: Abhishek J. Frederick Asst - ProfessorDocumento59 pagineSales and Distribution Management: Prepared By: Abhishek J. Frederick Asst - ProfessorasbroadwayNessuna valutazione finora

- Dissertation - Seyed Siamak Mousavi - Effective Elements On E-Marketing Strategy in Tourism IndustryDocumento9 pagineDissertation - Seyed Siamak Mousavi - Effective Elements On E-Marketing Strategy in Tourism IndustrySetya Aristu PranotoNessuna valutazione finora

- Optimize Supply Network DesignDocumento39 pagineOptimize Supply Network DesignThức NguyễnNessuna valutazione finora

- Management Information Systems 12th Edition Laudon Test BankDocumento22 pagineManagement Information Systems 12th Edition Laudon Test BankMhmdd Nour AlameddineNessuna valutazione finora

- SCM Final Project ReportDocumento14 pagineSCM Final Project ReportShaharyar Amin NCBA&ENessuna valutazione finora

- OEDocumento1 paginaOEJuse CoreNessuna valutazione finora

- E-Business Management & Innovation LecturesDocumento87 pagineE-Business Management & Innovation LecturesjnlyjunNessuna valutazione finora

- Minit LubeDocumento2 pagineMinit LubeMichael Tuazon Labao0% (1)

- Logistics J Operations and Supply Chain ManagementDocumento35 pagineLogistics J Operations and Supply Chain ManagementArjay B. CenizaNessuna valutazione finora

- Cost AccountingDocumento21 pagineCost AccountingMohamed SururrNessuna valutazione finora

- Supply Chain ManagementDocumento74 pagineSupply Chain ManagementAisyah RamliNessuna valutazione finora

- Kanban VS MRPDocumento16 pagineKanban VS MRPAffizul Azuwar100% (3)

- Unpacking Transportation Pricing FinalDocumento41 pagineUnpacking Transportation Pricing FinalSowmya RameshNessuna valutazione finora

- ME2065 KursPMDocumento4 pagineME2065 KursPMPacoNessuna valutazione finora

- Apics CourseworkDocumento6 pagineApics Courseworkf5dpebax100% (2)

- Basics Function OTMDocumento11 pagineBasics Function OTMHarisha Gowda100% (1)

- Clarion Technologies: at A GlanceDocumento7 pagineClarion Technologies: at A GlanceChetan PrasadNessuna valutazione finora

- Online Resources for Supply Chain Management TextbookDocumento6 pagineOnline Resources for Supply Chain Management TextbookRODRIGO FERNANDEZ ALVAREZ0% (2)

- Enterprise Resource PlanningDocumento11 pagineEnterprise Resource PlanningTanzil HaqueNessuna valutazione finora

- Company Introduction PT GEADocumento8 pagineCompany Introduction PT GEABegawan Half DoneNessuna valutazione finora

- ENEB Master in Supply Chain ManagementDocumento10 pagineENEB Master in Supply Chain ManagementHasnain IftikharNessuna valutazione finora