Potrebbero piacerti anche

- Managing Liquidity in Banks: A Top Down ApproachDa EverandManaging Liquidity in Banks: A Top Down ApproachNessuna valutazione finora

- Global Forecast: UpdateDocumento6 pagineGlobal Forecast: Updatebkginting6300Nessuna valutazione finora

- Bar Cap 3Documento11 pagineBar Cap 3Aquila99999Nessuna valutazione finora

- Economic Insights 25 02 13Documento16 pagineEconomic Insights 25 02 13vikashpunglia@rediffmail.comNessuna valutazione finora

- Quarterly Market Review: Second Quarter 2016Documento15 pagineQuarterly Market Review: Second Quarter 2016Anonymous Ht0MIJNessuna valutazione finora

- Treasury Outlook MarDocumento6 pagineTreasury Outlook Marelise_stefanikNessuna valutazione finora

- Week in Pictures 10 17 22 1666106256Documento13 pagineWeek in Pictures 10 17 22 1666106256Barry HeNessuna valutazione finora

- Global Markets Chart Book: High-Grade Bond Yields Plunge To Record LowsDocumento12 pagineGlobal Markets Chart Book: High-Grade Bond Yields Plunge To Record LowslosdiabloNessuna valutazione finora

- Foreign Exchange OutlookDocumento17 pagineForeign Exchange Outlookdey.parijat209Nessuna valutazione finora

- Global Market Outlook - August 2013 - GWMDocumento14 pagineGlobal Market Outlook - August 2013 - GWMFauzi DjauhariNessuna valutazione finora

- Global Macro Trends and Strategies - BloombergDocumento70 pagineGlobal Macro Trends and Strategies - Bloombergdrewmx100% (1)

- Asia Maxima (Delirium) - 3Q14 20140703Documento100 pagineAsia Maxima (Delirium) - 3Q14 20140703Hans WidjajaNessuna valutazione finora

- RBS On DowngradesDocumento17 pagineRBS On Downgradesharlock01Nessuna valutazione finora

- Euro Themes - SpainDocumento22 pagineEuro Themes - SpainGuy DviriNessuna valutazione finora

- MSFL - Inflation Aug'11Documento4 pagineMSFL - Inflation Aug'11Himanshu KuriyalNessuna valutazione finora

- Positioning For A Liquidity Drain: U.S. Interest Rates Outlook 2010Documento108 paginePositioning For A Liquidity Drain: U.S. Interest Rates Outlook 2010zacchariahNessuna valutazione finora

- ASEAN Economics: What Does A Cross-Current of DM Recovery, Rising Real Rates & China Slowdown Mean For ASEAN?Documento20 pagineASEAN Economics: What Does A Cross-Current of DM Recovery, Rising Real Rates & China Slowdown Mean For ASEAN?bodai100% (1)

- Week Summary: Macro StrategyDocumento10 pagineWeek Summary: Macro StrategyNoel AndreottiNessuna valutazione finora

- Foreign Exchange Daily ReportDocumento5 pagineForeign Exchange Daily ReportPrashanth Goud DharmapuriNessuna valutazione finora

- Bank Loans: Market Dynamics Poised To Deliver Attractive Risk-Adjusted ReturnsDocumento6 pagineBank Loans: Market Dynamics Poised To Deliver Attractive Risk-Adjusted ReturnsSabin NiculaeNessuna valutazione finora

- Across - The - Curve - in - Rates - and - Structured - Products - and - Across - The - Grade - in - Credit - Products - December 19, 2006 - (Bear, - Stearns - & - Co. - Inc.) PDFDocumento60 pagineAcross - The - Curve - in - Rates - and - Structured - Products - and - Across - The - Grade - in - Credit - Products - December 19, 2006 - (Bear, - Stearns - & - Co. - Inc.) PDFQuantDev-MNessuna valutazione finora

- HSBC - Currency Outlook DecemberDocumento46 pagineHSBC - Currency Outlook Decembermgroble3Nessuna valutazione finora

- Nomura Report On ChinaDocumento104 pagineNomura Report On ChinaSimon LouieNessuna valutazione finora

- ING Think FX Daily Currencies Gear Up For Another Big Week of Central Bank MeetingsDocumento5 pagineING Think FX Daily Currencies Gear Up For Another Big Week of Central Bank MeetingsPositionNessuna valutazione finora

- FX Compass: Looking For Signs of Pushback: Focus: Revising GBP Forecasts HigherDocumento25 pagineFX Compass: Looking For Signs of Pushback: Focus: Revising GBP Forecasts HighertekesburNessuna valutazione finora

- Barclays Global FX Quarterly Fed On Hold Eyes On GrowthDocumento42 pagineBarclays Global FX Quarterly Fed On Hold Eyes On GrowthgneymanNessuna valutazione finora

- Economics Docs 2022 184258.ashxDocumento65 pagineEconomics Docs 2022 184258.ashxTshepo ThaisiNessuna valutazione finora

- Van Hoisington Letter, Q3 2011Documento5 pagineVan Hoisington Letter, Q3 2011Elliott WaveNessuna valutazione finora

- Quarterly Review and Outlook: Growth Recession Continues Fiscal Policy in NeutralDocumento6 pagineQuarterly Review and Outlook: Growth Recession Continues Fiscal Policy in NeutralHonza MynarNessuna valutazione finora

- PzenaCommentary Second Quarter 2013Documento3 paginePzenaCommentary Second Quarter 2013CanadianValueNessuna valutazione finora

- Barclays Capital Tuesday Credit Call 20 September 2011Documento22 pagineBarclays Capital Tuesday Credit Call 20 September 2011poitrenacNessuna valutazione finora

- UBS Research Year Ahead 2019 Report Global enDocumento68 pagineUBS Research Year Ahead 2019 Report Global enphilipw_15Nessuna valutazione finora

- Lacy Hunt - Hoisington - Quartely Review Q1 2015Documento5 pagineLacy Hunt - Hoisington - Quartely Review Q1 2015TREND_7425Nessuna valutazione finora

- 48 - IEW March 2014Documento13 pagine48 - IEW March 2014girishrajsNessuna valutazione finora

- Oil & Commodities Monthly - February 2011Documento13 pagineOil & Commodities Monthly - February 2011ILoveDubsNessuna valutazione finora

- ING - FX TalkingDocumento18 pagineING - FX TalkingCiocoiu Vlad AndreiNessuna valutazione finora

- UBS Real Estate Outlook 2010Documento32 pagineUBS Real Estate Outlook 2010CRE Console100% (1)

- Understanding Vietnam - A Look Beyond The Facts and PDFDocumento24 pagineUnderstanding Vietnam - A Look Beyond The Facts and PDFDawood GacayanNessuna valutazione finora

- Nomura EU Bank Stress Test Results 2011 18 7 447460Documento23 pagineNomura EU Bank Stress Test Results 2011 18 7 447460ppt46Nessuna valutazione finora

- 巴克莱-美股-银行业-CCAR 2020 2.0:股票回购可以恢复,但派息率有上限-2020.12.20-27页Documento29 pagine巴克莱-美股-银行业-CCAR 2020 2.0:股票回购可以恢复,但派息率有上限-2020.12.20-27页HungNessuna valutazione finora

- Gic WeeklyDocumento12 pagineGic WeeklycampiyyyyoNessuna valutazione finora

- Abs CDSDocumento32 pagineAbs CDSMatt WallNessuna valutazione finora

- April Remit BarCApDocumento21 pagineApril Remit BarCApZerohedgeNessuna valutazione finora

- J.P. 摩根-美股-保险行业-2021年财险预览:商业再保险保险价格和自动频率顺风顺水-2021.1.4-83页Documento85 pagineJ.P. 摩根-美股-保险行业-2021年财险预览:商业再保险保险价格和自动频率顺风顺水-2021.1.4-83页HungNessuna valutazione finora

- Gundlach 6-14-16 Total Return Webcast Slides - Final - UnlockedDocumento73 pagineGundlach 6-14-16 Total Return Webcast Slides - Final - UnlockedZerohedge100% (1)

- Unicredit CEE Quarterly 4Q2019Documento76 pagineUnicredit CEE Quarterly 4Q2019Sorin DinuNessuna valutazione finora

- ACM - The Great Vega ShortDocumento10 pagineACM - The Great Vega ShortThorHollisNessuna valutazione finora

- Deutsche Bank Asia Healthcare 2018Documento76 pagineDeutsche Bank Asia Healthcare 2018Jc TanNessuna valutazione finora

- RCSI Weekly Bull/Bear Recap: Nov. 18-22, 2013Documento7 pagineRCSI Weekly Bull/Bear Recap: Nov. 18-22, 2013RCS_CFANessuna valutazione finora

- Cds - Heading Towards More Stable SystemDocumento28 pagineCds - Heading Towards More Stable SystemReadEverythingNessuna valutazione finora

- G10 Annual OutlookDocumento27 pagineG10 Annual OutlookansarialiNessuna valutazione finora

- ECON 351-International Trade-Turab HussainDocumento6 pagineECON 351-International Trade-Turab HussainshyasirNessuna valutazione finora

- FX Talking: Ing'S View On The Major Bullish and Bearish Currency ThemesDocumento20 pagineFX Talking: Ing'S View On The Major Bullish and Bearish Currency ThemesCiocoiu Vlad AndreiNessuna valutazione finora

- CS - GMN - 22 - Collateral Supply and Overnight RatesDocumento49 pagineCS - GMN - 22 - Collateral Supply and Overnight Rateswmthomson50% (2)

- Gold Yield Reports Investors IntelligenceDocumento100 pagineGold Yield Reports Investors IntelligenceAmit NadekarNessuna valutazione finora

- 507068Documento43 pagine507068ab3rdNessuna valutazione finora

- BNP FX WeeklyDocumento22 pagineBNP FX WeeklyPhillip HsiaNessuna valutazione finora

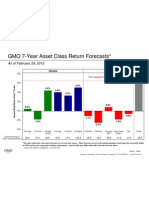

- GMO 7-Year Forecast - Feb '12Documento1 paginaGMO 7-Year Forecast - Feb '12Douglas RattrayNessuna valutazione finora

- Bond Price VolatilityDocumento56 pagineBond Price Volatilityanurag71500Nessuna valutazione finora

- Balance Sheet Recession - Richard KooDocumento19 pagineBalance Sheet Recession - Richard KooBryan LiNessuna valutazione finora

- The Failure of The Royal Bank of Scotland: Financial Services Authority Board ReportDocumento452 pagineThe Failure of The Royal Bank of Scotland: Financial Services Authority Board Reportbabstar999Nessuna valutazione finora

- The Price Revolution in The 16th Century: Empirical Results From A Structural Vectorautoregression ModelDocumento17 pagineThe Price Revolution in The 16th Century: Empirical Results From A Structural Vectorautoregression Modelbabstar999Nessuna valutazione finora

- The Monetary Origins of The Price Revolution': South German Silver Mining, Merchant - Banking, and Venetian Commerce, 1470-1540'Documento60 pagineThe Monetary Origins of The Price Revolution': South German Silver Mining, Merchant - Banking, and Venetian Commerce, 1470-1540'babstar999Nessuna valutazione finora

- Too Sovereign To Be Sued: Immunity of Centralbanks in Times of Financial CrisisDocumento22 pagineToo Sovereign To Be Sued: Immunity of Centralbanks in Times of Financial Crisisbabstar999Nessuna valutazione finora

- On ThinkingDocumento5 pagineOn Thinkingbabstar999Nessuna valutazione finora

- IMF ReportDocumento34 pagineIMF Reportpicchu144Nessuna valutazione finora

- Money, Bank Credit, and Economic CyclesDocumento936 pagineMoney, Bank Credit, and Economic CyclesJames HenryNessuna valutazione finora

- The Great Sovereign Risk Shift, Mark ThirlwellDocumento4 pagineThe Great Sovereign Risk Shift, Mark Thirlwellbabstar999100% (1)

- Solutions 1Documento9 pagineSolutions 1lalomg_straussNessuna valutazione finora

- Book Chapter SustainableDevelopment2022Documento22 pagineBook Chapter SustainableDevelopment2022Hernando CastellanosNessuna valutazione finora

- Agriculture 12 01372 v2Documento20 pagineAgriculture 12 01372 v2agastyaNessuna valutazione finora

- Vicious Circle of PovertyDocumento37 pagineVicious Circle of PovertyAdeel AhmadNessuna valutazione finora

- Pre-Board Papers With MS EconomicsDocumento160 paginePre-Board Papers With MS Economicsbksbharatkumar22005Nessuna valutazione finora

- Analisis Financiero de PRIMA AFPDocumento33 pagineAnalisis Financiero de PRIMA AFPJorge JimenezNessuna valutazione finora

- A Study of Unemployment in India, Causes and Implication: Anala Upadhya and Sruthy UnnikrishnanDocumento3 pagineA Study of Unemployment in India, Causes and Implication: Anala Upadhya and Sruthy UnnikrishnanMuthukrishnan NarayananNessuna valutazione finora

- OECD Review of The Corporate Governance of State Owned Enterprises CroatiaDocumento180 pagineOECD Review of The Corporate Governance of State Owned Enterprises CroatiagianniM0Nessuna valutazione finora

- Sample Business Article CritiqueDocumento5 pagineSample Business Article CritiqueGlaize FulgencioNessuna valutazione finora

- Bandhan BankDocumento5 pagineBandhan BankvaibhavNessuna valutazione finora

- IOUSA Not OK: An Analysis of The Deficit Disaster Story in The Film IOUSADocumento21 pagineIOUSA Not OK: An Analysis of The Deficit Disaster Story in The Film IOUSACenter for Economic and Policy Research100% (3)

- WRLODocumento31 pagineWRLOshailendra369Nessuna valutazione finora

- APO Productivity Databook 2017Documento174 pagineAPO Productivity Databook 2017cyntia namiraNessuna valutazione finora

- EC1101E Tutorial 6 - Macro Tutorial 1 (AY2011-2012 - Semester I) (With Answers)Documento6 pagineEC1101E Tutorial 6 - Macro Tutorial 1 (AY2011-2012 - Semester I) (With Answers)laevorisNessuna valutazione finora

- Con MixDocumento9 pagineCon MixsachirocksNessuna valutazione finora

- Interim Budget 2009-10Documento12 pagineInterim Budget 2009-10allmutualfundNessuna valutazione finora

- Wealth X World Ultra Wealth Report 2021Documento27 pagineWealth X World Ultra Wealth Report 2021Huong DuongNessuna valutazione finora

- MSMEs Unleashing The Engines of Economic ProsperityDocumento21 pagineMSMEs Unleashing The Engines of Economic ProsperityburhanuddinsaifyNessuna valutazione finora

- Bikol Reporter August 5 - 11, 2018 IssueDocumento8 pagineBikol Reporter August 5 - 11, 2018 IssueBikol ReporterNessuna valutazione finora

- Empowering Indonesia Report 2023pdfDocumento67 pagineEmpowering Indonesia Report 2023pdfAndre YPNessuna valutazione finora

- 16 Anwar Amar IqbalDocumento38 pagine16 Anwar Amar IqbalVaibhav KaushikNessuna valutazione finora

- Economics 10Documento3 pagineEconomics 10sherman ullahNessuna valutazione finora

- Export Market Selection Methods PDFDocumento41 pagineExport Market Selection Methods PDFAbahnya UkasyahNessuna valutazione finora

- European Countries English Skills Report 2019Documento52 pagineEuropean Countries English Skills Report 2019Andre Pierre GentzschNessuna valutazione finora

- Dissertation Report - Nikhil GuptaDocumento33 pagineDissertation Report - Nikhil GuptaJay Prakash SinghNessuna valutazione finora

- GCC Retail Industry Report 2012 - 9 December 2012Documento80 pagineGCC Retail Industry Report 2012 - 9 December 2012aakashblueNessuna valutazione finora

- Oq 2016 Raamdeo Agrawal 1Documento35 pagineOq 2016 Raamdeo Agrawal 1theNessuna valutazione finora

- Construction in The UK EconomyDocumento36 pagineConstruction in The UK Economyapi-25930623100% (1)

- Chapter Two:: Measuring National IncomeDocumento42 pagineChapter Two:: Measuring National IncomeArni Ayuni100% (1)

- Theory of Nations - Pastor Chris OyakhilomeDocumento5 pagineTheory of Nations - Pastor Chris OyakhilomePrince Charles Moyo100% (1)