Potrebbero piacerti anche

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- Instructions: This Affidavit Should Be Executed by The PersonDocumento1 paginaInstructions: This Affidavit Should Be Executed by The PersonspcbankingNessuna valutazione finora

- Reillo Vs Heirs of Quiterio San Jose - VosotrosDocumento2 pagineReillo Vs Heirs of Quiterio San Jose - VosotrosJules Vosotros100% (1)

- UP vs. DizonDocumento4 pagineUP vs. DizonJade Marlu DelaTorre100% (1)

- Police Power and Mandatory PWD DiscountsDocumento4 paginePolice Power and Mandatory PWD DiscountsIkkinNessuna valutazione finora

- Bilateral Versus Unilateral ContractsDocumento2 pagineBilateral Versus Unilateral ContractsThao TranNessuna valutazione finora

- Constantino A. Pascual, Substituted by His Heirs, Represented by Zenaida PascualDocumento2 pagineConstantino A. Pascual, Substituted by His Heirs, Represented by Zenaida PascualJei Essa Almias100% (1)

- Double Murder Conviction UpheldDocumento4 pagineDouble Murder Conviction Upheldcmptmarissa75% (4)

- Almario vs. Alba 127 SCRA 69 G.R. No. L-66088 January 25, 1984Documento14 pagineAlmario vs. Alba 127 SCRA 69 G.R. No. L-66088 January 25, 1984Eriyuna100% (1)

- Montebon Vs ComelecDocumento2 pagineMontebon Vs ComelecRaymond Roque100% (1)

- Spouses Yusay Vs CA Digest PubcorpDocumento2 pagineSpouses Yusay Vs CA Digest PubcorpEmelie Marie Diez100% (1)

- Sample MERCY Malaysia Annual Report 2011Documento140 pagineSample MERCY Malaysia Annual Report 2011raiden6263Nessuna valutazione finora

- Tenancy Form Blank - Schedule 1Documento3 pagineTenancy Form Blank - Schedule 1raiden6263Nessuna valutazione finora

- Hira Cave (Makka-KSA)Documento1 paginaHira Cave (Makka-KSA)raiden6263Nessuna valutazione finora

- 2014 Calendar with HolidaysDocumento1 pagina2014 Calendar with HolidaysMhackSahuNessuna valutazione finora

- Average Cost of FundsDocumento4 pagineAverage Cost of Fundsraiden6263Nessuna valutazione finora

- Hira Cave (Makka-KSA)Documento1 paginaHira Cave (Makka-KSA)raiden6263Nessuna valutazione finora

- 2014 Calendar with HolidaysDocumento1 pagina2014 Calendar with HolidaysMhackSahuNessuna valutazione finora

- Investment Linked Funds Annual Report 2011Documento23 pagineInvestment Linked Funds Annual Report 2011raiden6263Nessuna valutazione finora

- ASEAN List of Provisionally Allowed Hair Dye SubstancesDocumento31 pagineASEAN List of Provisionally Allowed Hair Dye Substancesraiden6263Nessuna valutazione finora

- Tutorial 1Documento3 pagineTutorial 1raiden6263Nessuna valutazione finora

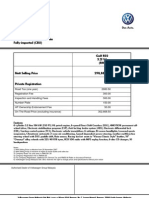

- Golf R32 - Price ListDocumento1 paginaGolf R32 - Price Listraiden6263Nessuna valutazione finora

- Incremental Model Incremental Theory Holds That The Selection of Goals and Objectives IsDocumento3 pagineIncremental Model Incremental Theory Holds That The Selection of Goals and Objectives IsLailanie L. LlameloNessuna valutazione finora

- CCBPI Vs MenezDocumento2 pagineCCBPI Vs MenezfaithNessuna valutazione finora

- The Color PurpleDocumento8 pagineThe Color PurplemjgvalcarceNessuna valutazione finora

- Rights To Filiation - CivRev1Documento82 pagineRights To Filiation - CivRev1Lindsay MillsNessuna valutazione finora

- Id Guide AttachmentsDocumento67 pagineId Guide AttachmentstransgenderlawcenterNessuna valutazione finora

- VirtuesDocumento3 pagineVirtuesIvy Gracia GarruchaNessuna valutazione finora

- WhatDoTheyKnow Threat - RDocumento2 pagineWhatDoTheyKnow Threat - RMiscellaneousNessuna valutazione finora

- Seminar Report On: Rattan Professional Education College Sohana, Sas Nagar (Mohali)Documento48 pagineSeminar Report On: Rattan Professional Education College Sohana, Sas Nagar (Mohali)Bharat AhujaNessuna valutazione finora

- Synopsis RedoDocumento2 pagineSynopsis Redo43Janhavi SansareNessuna valutazione finora

- CIR v. MANILA BANKERS LIFE INSURANCE CORPORATIONDocumento4 pagineCIR v. MANILA BANKERS LIFE INSURANCE CORPORATIONlyka timanNessuna valutazione finora

- Report EssayDocumento8 pagineReport Essayapi-291595324Nessuna valutazione finora

- Delgado Vda vs. Heirs of RustiaDocumento14 pagineDelgado Vda vs. Heirs of RustiaAnna BautistaNessuna valutazione finora

- 3 - Mariano vs. Atty. LakiDocumento2 pagine3 - Mariano vs. Atty. LakiJOSHUA KENNETH LAZARONessuna valutazione finora

- How To Save Income Tax Through Planning - RediffDocumento3 pagineHow To Save Income Tax Through Planning - Rediffsirsa11Nessuna valutazione finora

- PAD104 Tutorial Chapter 3Documento3 paginePAD104 Tutorial Chapter 3Emilda Mohamad JaafarNessuna valutazione finora

- Benjamin F. Washington v. Secretary of Health and Human Services, 718 F.2d 608, 3rd Cir. (1983)Documento4 pagineBenjamin F. Washington v. Secretary of Health and Human Services, 718 F.2d 608, 3rd Cir. (1983)Scribd Government DocsNessuna valutazione finora

- Rizona Ourt of PpealsDocumento8 pagineRizona Ourt of PpealsScribd Government DocsNessuna valutazione finora

- Speedy Trial Rights in India AnalyzedDocumento17 pagineSpeedy Trial Rights in India AnalyzedSumanth BhaskarNessuna valutazione finora

- Grounds For Judicial EjectmentDocumento2 pagineGrounds For Judicial EjectmentFrancis PalabayNessuna valutazione finora