Potrebbero piacerti anche

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Capital BudgetingDocumento20 pagineCapital BudgetingAngelo VilladoresNessuna valutazione finora

- Capital Budgeting: AbvilladoresDocumento39 pagineCapital Budgeting: AbvilladoresAngelo VilladoresNessuna valutazione finora

- Utilitarian Ethics and The Case of The Sole Remaining Supplier 1. BackgroundDocumento9 pagineUtilitarian Ethics and The Case of The Sole Remaining Supplier 1. BackgroundAngelo VilladoresNessuna valutazione finora

- People Power:: The Everyday Politics of Democratic Resistance in Burma and The PhilippinesDocumento180 paginePeople Power:: The Everyday Politics of Democratic Resistance in Burma and The PhilippinesAngelo VilladoresNessuna valutazione finora

- Trade Life Cycle Management in Finpricing: Part 3Documento16 pagineTrade Life Cycle Management in Finpricing: Part 3Angelo VilladoresNessuna valutazione finora

- Business: The Case AnalysisDocumento4 pagineBusiness: The Case AnalysisAngelo VilladoresNessuna valutazione finora

- Test Bank For Quantitative Analysis For Management 12th EditionDocumento12 pagineTest Bank For Quantitative Analysis For Management 12th EditionAngelo VilladoresNessuna valutazione finora

- Auditing Problems With AnswersDocumento12 pagineAuditing Problems With Answersaerwinde79% (34)

- Better Communities: Humans Helping HumansDocumento1 paginaBetter Communities: Humans Helping HumansAngelo VilladoresNessuna valutazione finora

- CPAR - TAX7411 - Estate Tax With Answer PDFDocumento6 pagineCPAR - TAX7411 - Estate Tax With Answer PDFAngelo Villadores92% (12)

- Major Themes in The Catholic Social TeachingsDocumento13 pagineMajor Themes in The Catholic Social TeachingsAngelo VilladoresNessuna valutazione finora

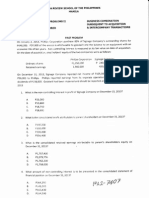

- CPAR - P2 - 7407 - Business Combination Subsequent To Acquisition PDFDocumento5 pagineCPAR - P2 - 7407 - Business Combination Subsequent To Acquisition PDFAngelo Villadores100% (3)

- CPAR - P2 - 7409 - NGAS & Non-Profit Organization PDFDocumento9 pagineCPAR - P2 - 7409 - NGAS & Non-Profit Organization PDFAngelo VilladoresNessuna valutazione finora

- CPAR - P2 - 7406 - Business Combination at Date of Acquisition With Answer PDFDocumento6 pagineCPAR - P2 - 7406 - Business Combination at Date of Acquisition With Answer PDFAngelo Villadores100% (4)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Econ 2000 Exam 2Documento11 pagineEcon 2000 Exam 2Peyton LawrenceNessuna valutazione finora

- 0455 w15 Ms 21 PDFDocumento12 pagine0455 w15 Ms 21 PDFMost. Amina KhatunNessuna valutazione finora

- Sandeep Garg Macroeconomics Class 12 Solutions Chapter 1Documento7 pagineSandeep Garg Macroeconomics Class 12 Solutions Chapter 1Muskan LohariwalNessuna valutazione finora

- 50 ArticleText 168 1 10 20200331Documento11 pagine50 ArticleText 168 1 10 20200331FajrinNessuna valutazione finora

- CV Tarun Das For Monitoring and Evaluation Expert July 2016Documento9 pagineCV Tarun Das For Monitoring and Evaluation Expert July 2016Professor Tarun DasNessuna valutazione finora

- Chapter 07. MC Questions No SolutionDocumento2 pagineChapter 07. MC Questions No SolutionAlliahDataNessuna valutazione finora

- Arbitrage Pricing TheoryDocumento8 pagineArbitrage Pricing Theorysush_bhatNessuna valutazione finora

- Comprehensive Problem 4 Solutions ManualDocumento9 pagineComprehensive Problem 4 Solutions Manualfarsi786Nessuna valutazione finora

- Topic 3 - Todaro, Economic Development - Ch.3 (Wiscana AP)Documento4 pagineTopic 3 - Todaro, Economic Development - Ch.3 (Wiscana AP)Wiscana Chacha100% (1)

- Management of Inventory SystemsDocumento14 pagineManagement of Inventory SystemsBiswanathMudiNessuna valutazione finora

- Design in Search of Roots An Indian Experience Uday AthavankarDocumento16 pagineDesign in Search of Roots An Indian Experience Uday AthavankarPriyanka MokkapatiNessuna valutazione finora

- Unit 6 TestDocumento4 pagineUnit 6 TestmecribbsNessuna valutazione finora

- 6 Pricing Understanding and Capturing Customer ValueDocumento27 pagine6 Pricing Understanding and Capturing Customer ValueShadi JabbourNessuna valutazione finora

- Iandfct 1 Examinersreportsept 2014 FinalDocumento12 pagineIandfct 1 Examinersreportsept 2014 FinalnigerianhacksNessuna valutazione finora

- Demand and Supply MicroeconomicsDocumento8 pagineDemand and Supply MicroeconomicsAviyaan SrivastavaNessuna valutazione finora

- FINMAN1 Module1Documento9 pagineFINMAN1 Module1Jayron NonguiNessuna valutazione finora

- MUH. AFDAL - E061211105 - International RelationsDocumento6 pagineMUH. AFDAL - E061211105 - International RelationsMuhammad AfdalNessuna valutazione finora

- Digital CompaqDocumento8 pagineDigital CompaqgauravrewariNessuna valutazione finora

- Monetary Policy of IndiaDocumento3 pagineMonetary Policy of IndiaBala SubramanianNessuna valutazione finora

- Problem SetDocumento14 pagineProblem SetVin PheakdeyNessuna valutazione finora

- Malaysian Economy SystemDocumento2 pagineMalaysian Economy SystemKassthurei Yogarajan100% (6)

- Production - The Heart of Organization - TBDDocumento14 pagineProduction - The Heart of Organization - TBDSakshi G AwasthiNessuna valutazione finora

- Market Indices PDFDocumento3 pagineMarket Indices PDFAshwani Rana100% (1)

- Itl 528 Assignment 2b 5day ExtendedDocumento14 pagineItl 528 Assignment 2b 5day Extendedapi-470484168Nessuna valutazione finora

- A Comparison of Different Automated Market-Maker StrategiesDocumento14 pagineA Comparison of Different Automated Market-Maker StrategiesmeamaNessuna valutazione finora

- Macroeconomics Lecture Chapter 15 UnemploymentDocumento30 pagineMacroeconomics Lecture Chapter 15 UnemploymentDX 1Nessuna valutazione finora

- Syllabi of B.voc. (Retail Management) 2014-15Documento38 pagineSyllabi of B.voc. (Retail Management) 2014-15Bikalpa BoraNessuna valutazione finora

- A.1 Topicos de Economia de La Regulacion de Los Servicios PublicosDocumento145 pagineA.1 Topicos de Economia de La Regulacion de Los Servicios PublicosFernandoNessuna valutazione finora

- PPTDocumento20 paginePPTshrutidas20% (1)

- Caie As Level Business 9609 Theory v1Documento44 pagineCaie As Level Business 9609 Theory v1Angelos LazaruNessuna valutazione finora