Potrebbero piacerti anche

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (894)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Case Study 5-9Documento7 pagineCase Study 5-9Dayan DudosNessuna valutazione finora

- Import Export DummiesDocumento3 pagineImport Export DummiesKB COPY CENTER DEPOK100% (2)

- Business Plan For A New ProductDocumento57 pagineBusiness Plan For A New ProductRuhan S M100% (1)

- DPP2013 Unit 1 Overview of International BusinessDocumento41 pagineDPP2013 Unit 1 Overview of International Businessnikazida100% (2)

- Constant Share Market AnalysisDocumento18 pagineConstant Share Market Analysisaviralsharma1711Nessuna valutazione finora

- 845-1605600599519-Unit - 18 GBE AssignmentDocumento55 pagine845-1605600599519-Unit - 18 GBE AssignmentKithmina ThilakarathneNessuna valutazione finora

- SR Supdt ListDocumento74 pagineSR Supdt ListRajesh AroraNessuna valutazione finora

- Latest December 2012 Final All India Supdts SerniorityDocumento174 pagineLatest December 2012 Final All India Supdts SernioritynlvmadhavNessuna valutazione finora

- ACES Assessee GuideDocumento13 pagineACES Assessee GuideArul SakthiNessuna valutazione finora

- IZT-ICT - Calling For RepresentationsDocumento4 pagineIZT-ICT - Calling For RepresentationsnlvmadhavNessuna valutazione finora

- Official Civil List 01-01-2012Documento268 pagineOfficial Civil List 01-01-2012nlvmadhavNessuna valutazione finora

- Ad Hoc Promtn JC BBM 08aug2013Documento2 pagineAd Hoc Promtn JC BBM 08aug2013nlvmadhavNessuna valutazione finora

- Boards Circular On Recovery of DemandsDocumento2 pagineBoards Circular On Recovery of DemandshydexcustNessuna valutazione finora

- Latest December 2012 Final All India Supdts SerniorityDocumento174 pagineLatest December 2012 Final All India Supdts SernioritynlvmadhavNessuna valutazione finora

- B 8 (Security)Documento2 pagineB 8 (Security)nlvmadhavNessuna valutazione finora

- Checklist For Central Excise RefundDocumento1 paginaChecklist For Central Excise RefundnlvmadhavNessuna valutazione finora

- Ad Hoc Promtn JC ACR 1 08aug2013Documento10 pagineAd Hoc Promtn JC ACR 1 08aug2013nlvmadhavNessuna valutazione finora

- Superintendent CE Seniority List 26.11.2010Documento1.144 pagineSuperintendent CE Seniority List 26.11.2010nlvmadhavNessuna valutazione finora

- MACP OrderDocumento6 pagineMACP OrdernlvmadhavNessuna valutazione finora

- MACP OrderDocumento6 pagineMACP OrderVigneshwar Raju PrathikantamNessuna valutazione finora

- Hand Book On RRsDocumento24 pagineHand Book On RRsinspvizagNessuna valutazione finora

- Notification No. 25/2012-Service Tax: Download From:Simple Tax India Dot NetDocumento70 pagineNotification No. 25/2012-Service Tax: Download From:Simple Tax India Dot NetSai Krishna MaddukuriNessuna valutazione finora

- Recruitment Rules - SuperintendentDocumento6 pagineRecruitment Rules - SuperintendentinspvizagNessuna valutazione finora

- IZT-ICT - Calling For RepresentationsDocumento4 pagineIZT-ICT - Calling For RepresentationsnlvmadhavNessuna valutazione finora

- B 8 (Security)Documento2 pagineB 8 (Security)nlvmadhavNessuna valutazione finora

- Checklist For Central Excise RefundDocumento1 paginaChecklist For Central Excise RefundnlvmadhavNessuna valutazione finora

- Form E.R.-1: MM YyyyDocumento8 pagineForm E.R.-1: MM YyyynlvmadhavNessuna valutazione finora

- Nomination FormsDocumento6 pagineNomination FormsnlvmadhavNessuna valutazione finora

- Cadre Restructuring - Implications For Gr.B. Gazetted) Officers in A.P. and Hyderabad ZoneDocumento4 pagineCadre Restructuring - Implications For Gr.B. Gazetted) Officers in A.P. and Hyderabad ZonehydexcustNessuna valutazione finora

- VizagictDocumento3 pagineVizagictnlvmadhavNessuna valutazione finora

- Govt Holiday List 11Documento6 pagineGovt Holiday List 11Archana AggarwalNessuna valutazione finora

- Lecture Notes-IfmDocumento90 pagineLecture Notes-IfmShradha BhandariNessuna valutazione finora

- 2013Documento127 pagine2013Sor VictorNessuna valutazione finora

- Export Marketing - Sem Vi MCQ Module 1 - Product Planning & Pricing DecisionsDocumento4 pagineExport Marketing - Sem Vi MCQ Module 1 - Product Planning & Pricing DecisionsSaniya SiddiquiNessuna valutazione finora

- BANSAL TYRE FinalDocumento78 pagineBANSAL TYRE FinalNishant KumarNessuna valutazione finora

- RBI Circular On Export Finance - 1Documento21 pagineRBI Circular On Export Finance - 1Anonymous l0MTRDGu3MNessuna valutazione finora

- LISTENING 10 Points: Intermediate Progress Test 3 Unit 7-9Documento3 pagineLISTENING 10 Points: Intermediate Progress Test 3 Unit 7-9Pao NogalesNessuna valutazione finora

- A Study On Export Procedures & Documentation at Itc BPL Pondi Uniersity Project ReportDocumento109 pagineA Study On Export Procedures & Documentation at Itc BPL Pondi Uniersity Project Reportphani raja kumarNessuna valutazione finora

- Managing Political Risk, Government Relations, and AlliancesDocumento26 pagineManaging Political Risk, Government Relations, and AlliancesNikita SangalNessuna valutazione finora

- Morita (w1)Documento27 pagineMorita (w1)JemalNessuna valutazione finora

- Magnan Andre J.R. 201006 PHD ThesisDocumento354 pagineMagnan Andre J.R. 201006 PHD ThesisMinhyoung KangNessuna valutazione finora

- Heba Handoussa-Economic Transition in The Middle East - Global ChallengesDocumento284 pagineHeba Handoussa-Economic Transition in The Middle East - Global ChallengesMourrani MarranNessuna valutazione finora

- MalaysiaDocumento29 pagineMalaysiaHanna TaganiNessuna valutazione finora

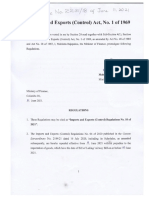

- Imports and Exports (Control) Act, No. 1 of 1969: Mahinda RajapaksaDocumento45 pagineImports and Exports (Control) Act, No. 1 of 1969: Mahinda RajapaksaShami MudunkotuwaNessuna valutazione finora

- Questionnaire On Export Procedure and DocumentationDocumento18 pagineQuestionnaire On Export Procedure and Documentationuma100% (1)

- Ib Unit 1Documento31 pagineIb Unit 1drashti vaishnavNessuna valutazione finora

- Anti Radiation ChipDocumento29 pagineAnti Radiation ChipMarufNessuna valutazione finora

- BCG Creative Cultural Economy Fact PackDocumento65 pagineBCG Creative Cultural Economy Fact Packapi-315608861Nessuna valutazione finora

- The Rationale of New Economic Policy 1991Documento3 pagineThe Rationale of New Economic Policy 1991Neeraj Agarwal50% (2)

- Guide to FDI (Foreign Direct InvestmentDocumento73 pagineGuide to FDI (Foreign Direct InvestmentArvind Sanu MisraNessuna valutazione finora

- Factors Influencing International SalesDocumento42 pagineFactors Influencing International SalesNayana Premchand100% (1)

- Australian Small Business Key Statistics and AnalysisDocumento109 pagineAustralian Small Business Key Statistics and AnalysisGeorge SmithNessuna valutazione finora

- Naamsa and Naacam 5 Year Automotive Sector Business PlanDocumento20 pagineNaamsa and Naacam 5 Year Automotive Sector Business PlandhurushaNessuna valutazione finora

- INDIA Trade 2018Documento176 pagineINDIA Trade 2018Vipin LNessuna valutazione finora

- IB International TradeDocumento41 pagineIB International TradeANTHONY AKINYOSOYENessuna valutazione finora