Potrebbero piacerti anche

- GST Tally ERP9 English: A Handbook for Understanding GST Implementation in TallyDa EverandGST Tally ERP9 English: A Handbook for Understanding GST Implementation in TallyValutazione: 5 su 5 stelle5/5 (1)

- Accounting BasicsDocumento21 pagineAccounting BasicsasifparwezNessuna valutazione finora

- Accountancy XiiDocumento122 pagineAccountancy XiiNancy Ekka100% (1)

- Tally Assignment Yash ComDocumento9 pagineTally Assignment Yash Comraj S.NNessuna valutazione finora

- Ap (Accounts Payable) ProcessDocumento10 pagineAp (Accounts Payable) ProcessRabin DebnathNessuna valutazione finora

- Grdae 9 - Ems - Financial Literacy SummaryDocumento17 pagineGrdae 9 - Ems - Financial Literacy SummarykotolograceNessuna valutazione finora

- Basics of Accounting - QBDocumento7 pagineBasics of Accounting - QBsujanthqatarNessuna valutazione finora

- Tally 036Documento191 pagineTally 036anjalishah7Nessuna valutazione finora

- Tally Final ExamDocumento4 pagineTally Final ExamsatyajitNessuna valutazione finora

- Tax FinalDocumento23 pagineTax FinalJitender ChaudharyNessuna valutazione finora

- Advanced Tally MCQ Original - WatermarkDocumento90 pagineAdvanced Tally MCQ Original - WatermarkVinod RathodNessuna valutazione finora

- FA1 General JournalDocumento5 pagineFA1 General JournalamirNessuna valutazione finora

- D2K-Report6i-by Dinesh Kumar S PDFDocumento98 pagineD2K-Report6i-by Dinesh Kumar S PDFallumohanNessuna valutazione finora

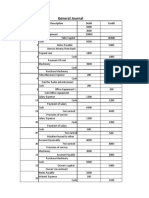

- General Journal: Date Description Debit CreditDocumento7 pagineGeneral Journal: Date Description Debit CreditAmanuel DemekeNessuna valutazione finora

- Accountancy Handout RevisionDocumento181 pagineAccountancy Handout RevisionSIMARNessuna valutazione finora

- Personal Finance and Planning: Skill Enhancement Course (SEC)Documento37 paginePersonal Finance and Planning: Skill Enhancement Course (SEC)Babita DeviNessuna valutazione finora

- Test 2Documento10 pagineTest 2himanshuNessuna valutazione finora

- GST Practical Record 40-50Documento48 pagineGST Practical Record 40-50Aditya raj ojhaNessuna valutazione finora

- TYBCom Sem VI Financial Accounting and Auditing Paper IX Financial AccountingDocumento181 pagineTYBCom Sem VI Financial Accounting and Auditing Paper IX Financial Accountingarbazshaha121Nessuna valutazione finora

- Trading, Profit & Loss Acct.sDocumento14 pagineTrading, Profit & Loss Acct.sSudheer SirangulaNessuna valutazione finora

- Tally - Business Accounts Question BankDocumento9 pagineTally - Business Accounts Question BankBhaskar bhaskarNessuna valutazione finora

- 42 Implementation of Tds in Tallyerp 9Documento171 pagine42 Implementation of Tds in Tallyerp 9P VenkatesanNessuna valutazione finora

- Excise For ManufacturersDocumento160 pagineExcise For ManufacturersPraveen CoolNessuna valutazione finora

- Oracle Apps Course ContentsDocumento12 pagineOracle Apps Course ContentsRabindra P.SinghNessuna valutazione finora

- Tally Record NoteDocumento74 pagineTally Record NoteBarani DharanNessuna valutazione finora

- Short Cut Keys in Tally 9Documento10 pagineShort Cut Keys in Tally 9Partha1962Nessuna valutazione finora

- Tally E Book 2Documento154 pagineTally E Book 2anjali44499Nessuna valutazione finora

- LLB Hon. Intergrated Law Sem 1 To 8 Syllabus May 2019Documento104 pagineLLB Hon. Intergrated Law Sem 1 To 8 Syllabus May 2019shah zavidNessuna valutazione finora

- Tally Interview Questions PDFDocumento6 pagineTally Interview Questions PDFRuqaya AhadNessuna valutazione finora

- 874 Taxation HandbookDocumento170 pagine874 Taxation HandbookYingYiga100% (1)

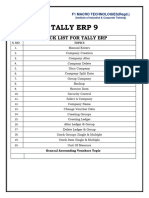

- GB Training & Placement Centre: Tally ERP 9 Certificate CourseDocumento2 pagineGB Training & Placement Centre: Tally ERP 9 Certificate CourseswayamNessuna valutazione finora

- AMFI - Investor Awareness Presentation - Jul'23Documento69 pagineAMFI - Investor Awareness Presentation - Jul'23padmaniaNessuna valutazione finora

- Chapter 1Documento5 pagineChapter 1palash khannaNessuna valutazione finora

- Self Study - Week 1 - Journal RevisionDocumento7 pagineSelf Study - Week 1 - Journal RevisionMehak Gupta100% (1)

- STUDY MATERIAL AccountingcomClass XIDocumento144 pagineSTUDY MATERIAL AccountingcomClass XImalathi SNessuna valutazione finora

- PL SQL - Training - PpsDocumento106 paginePL SQL - Training - PpsAnuNessuna valutazione finora

- Journalise The Following TransactionsDocumento1 paginaJournalise The Following Transactionshamidalikhanscorpion50% (2)

- Tally - Erp 9 - Post-Dated Voucher of Accounting & Inventory Vouchers Creation, Modification, DeletionsDocumento5 pagineTally - Erp 9 - Post-Dated Voucher of Accounting & Inventory Vouchers Creation, Modification, DeletionsHeemanshu ShahNessuna valutazione finora

- Oops TutorialDocumento20 pagineOops TutorialRajesh MandadapuNessuna valutazione finora

- GST Section ListDocumento7 pagineGST Section ListRahul ThapaNessuna valutazione finora

- Tally QuizDocumento9 pagineTally QuizSureshBadigerNessuna valutazione finora

- Villamor FinalDocumento25 pagineVillamor FinalRinconada Benori ReynalynNessuna valutazione finora

- Problem 1Documento3 pagineProblem 1karthikeyan01Nessuna valutazione finora

- Final AssignmentDocumento42 pagineFinal AssignmentRoopesh PandeNessuna valutazione finora

- Dma Module 1 Oracle SQL PL SQL IacDocumento110 pagineDma Module 1 Oracle SQL PL SQL IacK T Hoq Himel100% (1)

- Tally - ERP9 Book With GSTDocumento1.843 pagineTally - ERP9 Book With GSThatimNessuna valutazione finora

- List of Ledgers and It's Under Group in TallyDocumento5 pagineList of Ledgers and It's Under Group in Tallyrachel KujurNessuna valutazione finora

- Accountancy NCERT P2 (WWW - Ssctube.com)Documento305 pagineAccountancy NCERT P2 (WWW - Ssctube.com)Priyankesh ChourasiyaNessuna valutazione finora

- Intermediate Paper 11 PDFDocumento456 pagineIntermediate Paper 11 PDFjesurajajNessuna valutazione finora

- A Revisit On The Fundamentals of AccountingDocumento53 pagineA Revisit On The Fundamentals of AccountingGonzalo Jr. Ruales100% (1)

- Accounting Equation Imp 1Documento5 pagineAccounting Equation Imp 1hiritik gupta100% (1)

- Resume: Saravana Kumar V 8754598732 - Career ObjectiveDocumento3 pagineResume: Saravana Kumar V 8754598732 - Career ObjectiveporurNessuna valutazione finora

- Worksheet Ledger and Trial BalanceDocumento4 pagineWorksheet Ledger and Trial BalanceRajni Sinha VermaNessuna valutazione finora

- Extra Journal QuestionsDocumento3 pagineExtra Journal QuestionsMba BNessuna valutazione finora

- Questions On Trial Balance To StudentsDocumento6 pagineQuestions On Trial Balance To Studentsveraji3735Nessuna valutazione finora

- Accountancy Higher Secondary - Second Year Volume IDocumento132 pagineAccountancy Higher Secondary - Second Year Volume Iakvssakthivel100% (1)

- Accounting and Finance Numericals Problems and AnsDocumento11 pagineAccounting and Finance Numericals Problems and AnsPramodh Kanulla0% (1)

- Final AccountsDocumento5 pagineFinal AccountsGopal KrishnanNessuna valutazione finora

- Department of Business AdministrationDocumento9 pagineDepartment of Business AdministrationKannan NagaNessuna valutazione finora

- Final AccountsDocumento12 pagineFinal Accountsanandm1986100% (1)

- Suncor Energy IncDocumento1 paginaSuncor Energy IncBasil BabymNessuna valutazione finora

- UGMalayalam Online InstructionsDocumento3 pagineUGMalayalam Online InstructionsBasil BabymNessuna valutazione finora

- An Analysis of Financial Operations of Uniroyal Marine Exports LTD, Vengalam, CalicutDocumento49 pagineAn Analysis of Financial Operations of Uniroyal Marine Exports LTD, Vengalam, CalicutBasil BabymNessuna valutazione finora

- LimitationsDocumento2 pagineLimitationsBasil BabymNessuna valutazione finora

- Jerome4 Sample Chap08Documento58 pagineJerome4 Sample Chap08Basil Babym100% (7)

- Classification of MNCDocumento16 pagineClassification of MNCBasil Babym91% (22)

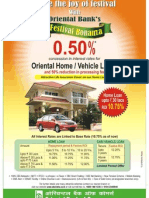

- Festival Bonanza Ad 2011 SepDocumento1 paginaFestival Bonanza Ad 2011 SepBasil BabymNessuna valutazione finora

- Call RoutingDocumento42 pagineCall RoutingRogelio Ramirez MillanNessuna valutazione finora

- Paper IndustryDocumento8 paginePaper IndustryBasil BabymNessuna valutazione finora

- The Full Paper Making ProcessDocumento7 pagineThe Full Paper Making Processnapachaya100% (1)

- WellaPlex Technical 2017Documento2 pagineWellaPlex Technical 2017Rinita BhattacharyaNessuna valutazione finora

- Coc 1 ExamDocumento7 pagineCoc 1 ExamJelo BioNessuna valutazione finora

- Understanding Culture Society, and PoliticsDocumento3 pagineUnderstanding Culture Society, and PoliticsVanito SwabeNessuna valutazione finora

- IELTS Material Writing 1Documento112 pagineIELTS Material Writing 1Lê hoàng anhNessuna valutazione finora

- DR Afwan Fajri - Trauma - Juli 2023Documento82 pagineDR Afwan Fajri - Trauma - Juli 2023afwan fajriNessuna valutazione finora

- Editor Attach 1327138073 1832Documento59 pagineEditor Attach 1327138073 1832Monther Al DebesNessuna valutazione finora

- 2022 NEDA Annual Report Pre PubDocumento68 pagine2022 NEDA Annual Report Pre PubfrancessantiagoNessuna valutazione finora

- Products ListDocumento11 pagineProducts ListPorag AhmedNessuna valutazione finora

- Beng (Hons) Telecommunications: Cohort: Btel/10B/Ft & Btel/09/FtDocumento9 pagineBeng (Hons) Telecommunications: Cohort: Btel/10B/Ft & Btel/09/FtMarcelo BaptistaNessuna valutazione finora

- NJEX 7300G: Pole MountedDocumento130 pagineNJEX 7300G: Pole MountedJorge Luis MartinezNessuna valutazione finora

- PEA Comp Study - Estate Planning For Private Equity Fund Managers (ITaback, JWaxenberg 10 - 10)Documento13 paginePEA Comp Study - Estate Planning For Private Equity Fund Managers (ITaback, JWaxenberg 10 - 10)lbaker2009Nessuna valutazione finora

- Multi-Media Approach To Teaching-LearningDocumento8 pagineMulti-Media Approach To Teaching-LearningswethashakiNessuna valutazione finora

- PRINCIPLES OF TEACHING NotesDocumento24 paginePRINCIPLES OF TEACHING NotesHOLLY MARIE PALANGAN100% (2)

- DLL in Health 7 3rd QuarterDocumento2 pagineDLL in Health 7 3rd QuarterJuna Lyn Hermida ArellonNessuna valutazione finora

- Landcorp FLCC Brochure 2013 v3Documento6 pagineLandcorp FLCC Brochure 2013 v3Shadi GarmaNessuna valutazione finora

- Black Hole Safety Brochure Trifold FinalDocumento2 pagineBlack Hole Safety Brochure Trifold Finalvixy1830Nessuna valutazione finora

- 2021-01-01 - Project (Construction) - One TemplateDocumento1.699 pagine2021-01-01 - Project (Construction) - One TemplatemayalogamNessuna valutazione finora

- Lecture 1 Electrolyte ImbalanceDocumento15 pagineLecture 1 Electrolyte ImbalanceSajib Chandra RoyNessuna valutazione finora

- Text Extraction From Image: Team Members CH - Suneetha (19mcmb22) Mohit Sharma (19mcmb13)Documento20 pagineText Extraction From Image: Team Members CH - Suneetha (19mcmb22) Mohit Sharma (19mcmb13)suneethaNessuna valutazione finora

- NATO Obsolescence Management PDFDocumento5 pagineNATO Obsolescence Management PDFluisNessuna valutazione finora

- The Impact of Personnel Behaviour in Clean RoomDocumento59 pagineThe Impact of Personnel Behaviour in Clean Roomisrael afolayan mayomiNessuna valutazione finora

- Activity Based Costing TestbanksDocumento18 pagineActivity Based Costing TestbanksCharlene MinaNessuna valutazione finora

- USTH Algorithm RecursionDocumento73 pagineUSTH Algorithm Recursionnhng2421Nessuna valutazione finora

- Vtoris 100% Clean Paypal Transfer Guide 2015Documento8 pagineVtoris 100% Clean Paypal Transfer Guide 2015Sean FrohmanNessuna valutazione finora

- Heat Pyqs NsejsDocumento3 pagineHeat Pyqs NsejsPocketMonTuberNessuna valutazione finora

- Credit CardDocumento6 pagineCredit CardJ Boy LipayonNessuna valutazione finora

- Medical Equipment Quality Assurance For Healthcare FacilitiesDocumento5 pagineMedical Equipment Quality Assurance For Healthcare FacilitiesJorge LopezNessuna valutazione finora

- The Chassis OC 500 LE: Technical InformationDocumento12 pagineThe Chassis OC 500 LE: Technical InformationAbdelhak Ezzahrioui100% (1)

- Carbonate Platform MateriDocumento8 pagineCarbonate Platform MateriNisaNessuna valutazione finora

- Technology 6 B Matrixed Approach ToDocumento12 pagineTechnology 6 B Matrixed Approach ToNevin SunnyNessuna valutazione finora