Potrebbero piacerti anche

- Food Outlook: Biannual Report on Global Food Markets: November 2022Da EverandFood Outlook: Biannual Report on Global Food Markets: November 2022Nessuna valutazione finora

- MENAP Oil-Exporting Countries: Feeling The Impact of Lower and More Volatile Oil PricesDocumento12 pagineMENAP Oil-Exporting Countries: Feeling The Impact of Lower and More Volatile Oil PricesSara SimoesNessuna valutazione finora

- ENMPOOCT19 KuwaitDocumento2 pagineENMPOOCT19 KuwaitfdsfdsaNessuna valutazione finora

- Task-7 Crude Oil: Impact of Crude Oil Fluctuations in Different Sectors Refiners and Oil Marketing CompaniesDocumento17 pagineTask-7 Crude Oil: Impact of Crude Oil Fluctuations in Different Sectors Refiners and Oil Marketing Companiessnithisha chandranNessuna valutazione finora

- Macroeconomic Update Nov 2018Documento11 pagineMacroeconomic Update Nov 2018Dana GaithNessuna valutazione finora

- Management Discussion Analysis 2009Documento6 pagineManagement Discussion Analysis 2009himanshu2400Nessuna valutazione finora

- Economic Indicators Report August 2021Documento36 pagineEconomic Indicators Report August 2021Dheeraj DhondNessuna valutazione finora

- Godrej Consumer Products Limited: Recovery Likely by Q1FY2021Documento5 pagineGodrej Consumer Products Limited: Recovery Likely by Q1FY2021anjugaduNessuna valutazione finora

- Macroeconomic Report May 2020 Economic DivisionDocumento22 pagineMacroeconomic Report May 2020 Economic DivisionTim SheldonNessuna valutazione finora

- Shell Pakistan Stock in Trade: Horizontal AnalysisDocumento12 pagineShell Pakistan Stock in Trade: Horizontal Analysisfahad pansotaNessuna valutazione finora

- Quarterly July2017Documento18 pagineQuarterly July2017Sahludheen N HNessuna valutazione finora

- Insights Bullish Near Term OutlookDocumento62 pagineInsights Bullish Near Term OutlookHandy HarisNessuna valutazione finora

- Oil PricesDocumento7 pagineOil PricesSrikara SimhaNessuna valutazione finora

- Applied Economics AssignmentDocumento1 paginaApplied Economics AssignmentAnonymous tgYyno0w6Nessuna valutazione finora

- Sector Comment Oil Gas Cross Region 27may20Documento5 pagineSector Comment Oil Gas Cross Region 27may20Pedro MentadoNessuna valutazione finora

- AngelTopPicks Aug 2022Documento13 pagineAngelTopPicks Aug 2022vijay kumarNessuna valutazione finora

- India Export and Import PDFDocumento43 pagineIndia Export and Import PDFKARTIK PANPALIA 22DM122Nessuna valutazione finora

- Monetary Policy ReportDocumento75 pagineMonetary Policy Reportpls2019Nessuna valutazione finora

- Section 1Documento10 pagineSection 1Imran RazaNessuna valutazione finora

- Chartbook - September 2022Documento13 pagineChartbook - September 2022Shama ShaikNessuna valutazione finora

- Financial Markets - Trading Report - 2Documento5 pagineFinancial Markets - Trading Report - 2Usman AhmadNessuna valutazione finora

- Diwali Muhurat Fundamental 2021Documento22 pagineDiwali Muhurat Fundamental 2021Swasthyasudha AyurvedNessuna valutazione finora

- Qe Co ForecastDocumento9 pagineQe Co ForecastJudithRavelloNessuna valutazione finora

- Macro Outlook: United Arab Emirates: PublicDocumento2 pagineMacro Outlook: United Arab Emirates: PublicahatttNessuna valutazione finora

- Oil Demand Uncertainties Linger: Economic and Financial AnalysisDocumento6 pagineOil Demand Uncertainties Linger: Economic and Financial AnalysisOwm Close CorporationNessuna valutazione finora

- Oil Sector PDFDocumento15 pagineOil Sector PDFRochak AgarwalNessuna valutazione finora

- Nigerian-Oil-And-Gas-Update-Quarterly-Newsletter - Edition-2021Documento3 pagineNigerian-Oil-And-Gas-Update-Quarterly-Newsletter - Edition-2021cyrilNessuna valutazione finora

- Question: Impact of Currency Devaluation On Foreign Trade/ Oil and Gas Industry. Answer: Overview of Currency DevaluationDocumento3 pagineQuestion: Impact of Currency Devaluation On Foreign Trade/ Oil and Gas Industry. Answer: Overview of Currency DevaluationRIYA MODINessuna valutazione finora

- RIG April 2013Documento40 pagineRIG April 2013cuntingyouNessuna valutazione finora

- GEMD Jan09Documento5 pagineGEMD Jan09Jamie WebsterNessuna valutazione finora

- Market Outlook - May 2011Documento4 pagineMarket Outlook - May 2011alohia82Nessuna valutazione finora

- SeminarDocumento13 pagineSeminarManoj YadavNessuna valutazione finora

- Bangladesh Economic Prospects 2019Documento14 pagineBangladesh Economic Prospects 2019Silvia RozarioNessuna valutazione finora

- AngelTopPicks Oct 2022Documento12 pagineAngelTopPicks Oct 2022dipyaman patgiriNessuna valutazione finora

- Caie As Economics 9708 Model Answers v1Documento11 pagineCaie As Economics 9708 Model Answers v1Uzair siddiqui100% (1)

- MP Statement NovDocumento14 pagineMP Statement NovZainab BadarNessuna valutazione finora

- Kuwait Economic Brief 2009 Part4Documento1 paginaKuwait Economic Brief 2009 Part4mazenkhodr1983Nessuna valutazione finora

- National Refinery Limited: Brief RecordingsDocumento1 paginaNational Refinery Limited: Brief RecordingsAwad TariqNessuna valutazione finora

- Fitch Report On Edible Oil Sector in IndiaDocumento7 pagineFitch Report On Edible Oil Sector in IndiaprashantNessuna valutazione finora

- Oil & Gas: Difficult Times..Documento4 pagineOil & Gas: Difficult Times..Arvind MeenaNessuna valutazione finora

- Task 7 - Abin Som - 21FMCGB5Documento17 pagineTask 7 - Abin Som - 21FMCGB5Abin Som 2028121Nessuna valutazione finora

- Oinl 14 2 24 PLDocumento6 pagineOinl 14 2 24 PLSanjeedeep Mishra , 315Nessuna valutazione finora

- UAE Economic EnvironmentDocumento51 pagineUAE Economic Environmentafrocircus09Nessuna valutazione finora

- Investor Digest: HighlightDocumento14 pagineInvestor Digest: HighlightYua GeorgeusNessuna valutazione finora

- JPM Reliance Industries 2022-07-20 4150945Documento8 pagineJPM Reliance Industries 2022-07-20 4150945Abhishek SaxenaNessuna valutazione finora

- Current State of Indian Economy: December 2008Documento24 pagineCurrent State of Indian Economy: December 2008samwaltonNessuna valutazione finora

- Weekly Economic and Markets Review: International & MENADocumento2 pagineWeekly Economic and Markets Review: International & MENAVáclav NěmecNessuna valutazione finora

- Crash in Oil Prices, How It Is Impacting IndiaDocumento2 pagineCrash in Oil Prices, How It Is Impacting IndiaChinmay DwivediNessuna valutazione finora

- Eco Cia 3 McomDocumento31 pagineEco Cia 3 McomTHAMERAVARUNI N 1917061Nessuna valutazione finora

- CrudeDocumento23 pagineCrudeMuhammad TohamyNessuna valutazione finora

- Energy Monthly Report - JanuaryDocumento5 pagineEnergy Monthly Report - JanuaryLi ZhangNessuna valutazione finora

- Russia Automotive Market and The CIS 2010Documento24 pagineRussia Automotive Market and The CIS 2010SojanuNessuna valutazione finora

- AngelTopPicks July 2022Documento13 pagineAngelTopPicks July 2022cryovikas1975Nessuna valutazione finora

- Nirmal Bang Berger Paints Q3FY22 Result Update 11 February 2022Documento11 pagineNirmal Bang Berger Paints Q3FY22 Result Update 11 February 2022Shinde Chaitanya Sharad C-DOT 5688Nessuna valutazione finora

- What Drives Crude Oil Prices?Documento23 pagineWhat Drives Crude Oil Prices?prdyumnNessuna valutazione finora

- Indian Oil Corporation (IOCL IN) : Q4FY19 Result UpdateDocumento7 pagineIndian Oil Corporation (IOCL IN) : Q4FY19 Result UpdatePraveen KumarNessuna valutazione finora

- Impact Analysis of Emerging Markets:: Oil Demand in China and India FallingDocumento4 pagineImpact Analysis of Emerging Markets:: Oil Demand in China and India FallingRavi SinghNessuna valutazione finora

- CI2315 Bahrain Economic 2022 ENDocumento23 pagineCI2315 Bahrain Economic 2022 ENMaria VidalNessuna valutazione finora

- Currency Wars: Impact On IndiaDocumento7 pagineCurrency Wars: Impact On IndiaAbhishek TalujaNessuna valutazione finora

- 8086 Cpu ArchitectureDocumento9 pagine8086 Cpu Architectureapi-371236783% (6)

- Fiscal Deficit 2003 FormatDocumento19 pagineFiscal Deficit 2003 Formatapi-3712367Nessuna valutazione finora

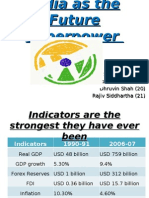

- India As SuperpowerDocumento21 pagineIndia As Superpowerapi-3712367Nessuna valutazione finora

- L & TDocumento9 pagineL & Tapi-3712367Nessuna valutazione finora

- WEight Training ScheduleDocumento2 pagineWEight Training Scheduleapi-3712367100% (1)

- Anti-Inflationary Policy in IndiaDocumento14 pagineAnti-Inflationary Policy in Indiaapi-3712367Nessuna valutazione finora

- Manging Foreign ExchnageDocumento6 pagineManging Foreign Exchnageapi-3712367Nessuna valutazione finora

- Macroeconomics AssignmentsDocumento15 pagineMacroeconomics Assignmentsapi-3712367Nessuna valutazione finora

- Policybrief Nov05Documento6 paginePolicybrief Nov05api-3712367Nessuna valutazione finora

- Report OnDocumento9 pagineReport Onapi-3712367Nessuna valutazione finora

- Manging Foreign ExchnageDocumento6 pagineManging Foreign Exchnageapi-3712367Nessuna valutazione finora

- Macro Economics OutlineDocumento2 pagineMacro Economics Outlineapi-3712367100% (1)

- 72903Documento11 pagine72903api-3712367Nessuna valutazione finora

- Just in TimeDocumento3 pagineJust in Timeapi-3712367Nessuna valutazione finora

- FOREX Management Versus SingaporeDocumento3 pagineFOREX Management Versus Singaporeapi-3712367Nessuna valutazione finora

- Subprime Toxic Debt - Bloomberg July07Documento10 pagineSubprime Toxic Debt - Bloomberg July07api-3712367Nessuna valutazione finora

- FFRChange HistoryDocumento1 paginaFFRChange Historyapi-3712367Nessuna valutazione finora

- US Subprime 070817Documento6 pagineUS Subprime 070817api-3712367Nessuna valutazione finora

- Foreign Exchange Management Policy in IndiaDocumento6 pagineForeign Exchange Management Policy in Indiaapi-371236767% (3)

- D&B Economy Observer November 07Documento3 pagineD&B Economy Observer November 07api-3712367Nessuna valutazione finora

- Fema CDocumento5 pagineFema Capi-3712367Nessuna valutazione finora

- Subprime FinalDocumento34 pagineSubprime Finalapi-3712367Nessuna valutazione finora

- BSC & Knowledge ManagementDocumento3 pagineBSC & Knowledge Managementapi-3712367100% (1)

- SubPrime Mortgage MarketDocumento6 pagineSubPrime Mortgage Marketapi-3712367Nessuna valutazione finora

- SubprimeDocumento31 pagineSubprimeapi-3712367Nessuna valutazione finora

- Sebi TocDocumento33 pagineSebi Tocapi-3712367Nessuna valutazione finora

- Balanced Scorecard 02Documento7 pagineBalanced Scorecard 02api-3712367100% (2)

- Balanced Scorecard Elearning - PresentationDocumento39 pagineBalanced Scorecard Elearning - Presentationapi-3712367Nessuna valutazione finora

- Balanced ScorecardDocumento13 pagineBalanced Scorecardapi-3712367Nessuna valutazione finora

- National Income Accounting and The Balance of PaymentsDocumento29 pagineNational Income Accounting and The Balance of Paymentsanji 1230% (1)

- Module 2Documento41 pagineModule 2bhargaviNessuna valutazione finora

- Nomura Strategy 03 11Documento106 pagineNomura Strategy 03 11Thiago PalaiaNessuna valutazione finora

- Q.No. Question Options AnswerDocumento23 pagineQ.No. Question Options Answerakshaykohli7890Nessuna valutazione finora

- Britain's Middle East Oil and Struggle To Save SterlingDocumento368 pagineBritain's Middle East Oil and Struggle To Save SterlingSohrabNessuna valutazione finora

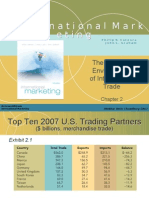

- International Marketing Chapter 2 (The Dynamic Environment of International Trade)Documento39 pagineInternational Marketing Chapter 2 (The Dynamic Environment of International Trade)Nitin Jain0% (1)

- Economic Condition of IndonesiaDocumento38 pagineEconomic Condition of IndonesiaKidal PermonoNessuna valutazione finora

- Foreign Collaborations in IndiaDocumento17 pagineForeign Collaborations in IndiacagopalchaturvediNessuna valutazione finora

- Pob NotesDocumento21 paginePob NotesOneeka Plutoqueenbee Adams91% (11)

- Yemen, Rep. at A Glance: (Average Annual Growth)Documento2 pagineYemen, Rep. at A Glance: (Average Annual Growth)tahaalkibsiNessuna valutazione finora

- Chapter 1 3Documento17 pagineChapter 1 3Hieu Duong Trong100% (3)

- Joachim Becker & Johannes Jaeger - From An Economic Crises To A Crisis of European IntegrationDocumento27 pagineJoachim Becker & Johannes Jaeger - From An Economic Crises To A Crisis of European IntegrationAndraž MaliNessuna valutazione finora

- 122 0704Documento35 pagine122 0704api-27548664Nessuna valutazione finora

- Factors That Influence Exchange RatesDocumento2 pagineFactors That Influence Exchange RatesJoelene ChewNessuna valutazione finora

- Lecture On International Entrepreneurship Opportunities.Documento31 pagineLecture On International Entrepreneurship Opportunities.Rahul Soni100% (2)

- CAD EssayDocumento4 pagineCAD Essayshelterman14Nessuna valutazione finora

- Analysis Central BankingDocumento12 pagineAnalysis Central Bankingjohann_747Nessuna valutazione finora

- 2281 s13 QP 21Documento4 pagine2281 s13 QP 21IslamAltawanayNessuna valutazione finora

- India's Gold Rush Its Impact and SustainabilityDocumento35 pagineIndia's Gold Rush Its Impact and SustainabilitySCRIBDEBMNessuna valutazione finora

- Case Study On NDB and DFCCDocumento34 pagineCase Study On NDB and DFCCRantharu AttanayakeNessuna valutazione finora

- Asian Financial CrisisDocumento7 pagineAsian Financial Crisisdjt10kNessuna valutazione finora

- Economics For Ca-Cpt - Quick Revision VersionDocumento14 pagineEconomics For Ca-Cpt - Quick Revision VersionCA Suman Gadamsetti75% (4)

- Counter TradeDocumento12 pagineCounter TradeRAHULNessuna valutazione finora

- Summer Project ReportDocumento55 pagineSummer Project ReportsunilpratihariNessuna valutazione finora

- International Finance & Forex Management 1Documento102 pagineInternational Finance & Forex Management 1Mr DamphaNessuna valutazione finora

- Bridge Course in EconomicsDocumento17 pagineBridge Course in EconomicsProfessor Tarun DasNessuna valutazione finora

- 3 Years Interim PlanDocumento828 pagine3 Years Interim PlanMenuka ShresthaNessuna valutazione finora

- Fathoming FEMA (Overview of Provisions of Foreign Exchange Management Act, 1999 (FEMA) and Rules and Regulations There Under) by Rajkumar S Adukia 4Documento16 pagineFathoming FEMA (Overview of Provisions of Foreign Exchange Management Act, 1999 (FEMA) and Rules and Regulations There Under) by Rajkumar S Adukia 4Apoorv GogarNessuna valutazione finora

- Full S&P Rating StatementDocumento13 pagineFull S&P Rating StatementFadia SalieNessuna valutazione finora

- Trade Policy Review Pakistan 2015Documento111 pagineTrade Policy Review Pakistan 2015amin jamalNessuna valutazione finora