Potrebbero piacerti anche

- Supreme CourtDocumento15 pagineSupreme CourtDinSFLA100% (1)

- CAAP 14 0001115mopDocumento21 pagineCAAP 14 0001115mopDinSFLANessuna valutazione finora

- CAAP 17 0000553sdoDocumento5 pagineCAAP 17 0000553sdoDinSFLANessuna valutazione finora

- SCWC 16 0000319Documento29 pagineSCWC 16 0000319DinSFLANessuna valutazione finora

- Case: 14-14544 Date Filed: 05/03/2019 Page: 1 of 76Documento76 pagineCase: 14-14544 Date Filed: 05/03/2019 Page: 1 of 76DinSFLANessuna valutazione finora

- CAAP 18 0000477sdoDocumento15 pagineCAAP 18 0000477sdoDinSFLA100% (1)

- Electronically Filed Intermediate Court of Appeals CAAP-17-0000402 22-MAY-2019 08:23 AMDocumento7 pagineElectronically Filed Intermediate Court of Appeals CAAP-17-0000402 22-MAY-2019 08:23 AMDinSFLANessuna valutazione finora

- (J-67-2018) in The Supreme Court of Pennsylvania Eastern District Saylor, C.J., Baer, Todd, Donohue, Dougherty, Wecht, Mundy, JJDocumento18 pagine(J-67-2018) in The Supreme Court of Pennsylvania Eastern District Saylor, C.J., Baer, Todd, Donohue, Dougherty, Wecht, Mundy, JJDinSFLANessuna valutazione finora

- Electronically Filed Intermediate Court of Appeals CAAP-15-0000734 13-MAY-2019 08:14 AMDocumento15 pagineElectronically Filed Intermediate Court of Appeals CAAP-15-0000734 13-MAY-2019 08:14 AMDinSFLANessuna valutazione finora

- Electronically Filed Intermediate Court of Appeals CAAP-18-0000298 19-MAR-2019 08:43 AMDocumento7 pagineElectronically Filed Intermediate Court of Appeals CAAP-18-0000298 19-MAR-2019 08:43 AMDinSFLA100% (1)

- Supreme Court of The State of New York Appellate Division: Second Judicial DepartmentDocumento6 pagineSupreme Court of The State of New York Appellate Division: Second Judicial DepartmentDinSFLA100% (1)

- Electronically Filed Intermediate Court of Appeals CAAP-15-0000316 21-MAR-2019 07:51 AMDocumento3 pagineElectronically Filed Intermediate Court of Appeals CAAP-15-0000316 21-MAR-2019 07:51 AMDinSFLANessuna valutazione finora

- Certified For Publication: Filed 4/30/19 Reposted With Page NumbersDocumento10 pagineCertified For Publication: Filed 4/30/19 Reposted With Page NumbersDinSFLANessuna valutazione finora

- Filed 4/2/19 On Transfer: Enner LockDocumento39 pagineFiled 4/2/19 On Transfer: Enner LockDinSFLANessuna valutazione finora

- Electronically Filed Intermediate Court of Appeals CAAP-17-0000848 28-DEC-2018 07:54 AMDocumento7 pagineElectronically Filed Intermediate Court of Appeals CAAP-17-0000848 28-DEC-2018 07:54 AMDinSFLANessuna valutazione finora

- Electronically Filed Intermediate Court of Appeals CAAP-14-0001093 28-JAN-2019 07:52 AMDocumento13 pagineElectronically Filed Intermediate Court of Appeals CAAP-14-0001093 28-JAN-2019 07:52 AMDinSFLANessuna valutazione finora

- Supreme Court of Florida: Marie Ann GlassDocumento15 pagineSupreme Court of Florida: Marie Ann GlassDinSFLANessuna valutazione finora

- Electronically Filed Intermediate Court of Appeals CAAP-15-0000442 28-FEB-2019 08:04 AMDocumento6 pagineElectronically Filed Intermediate Court of Appeals CAAP-15-0000442 28-FEB-2019 08:04 AMDinSFLANessuna valutazione finora

- Electronically Filed Intermediate Court of Appeals CAAP-16-0000178 27-DEC-2018 07:55 AMDocumento13 pagineElectronically Filed Intermediate Court of Appeals CAAP-16-0000178 27-DEC-2018 07:55 AMDinSFLANessuna valutazione finora

- Electronically Filed Intermediate Court of Appeals CAAP-17-0000884 29-JAN-2019 08:15 AMDocumento7 pagineElectronically Filed Intermediate Court of Appeals CAAP-17-0000884 29-JAN-2019 08:15 AMDinSFLA50% (2)

- United States Court of Appeals For The Ninth CircuitDocumento17 pagineUnited States Court of Appeals For The Ninth CircuitDinSFLANessuna valutazione finora

- Not To Be Published in Official Reports: Filed 2/14/19 The Bank of New York Mellon v. Horner CA4/3Documento10 pagineNot To Be Published in Official Reports: Filed 2/14/19 The Bank of New York Mellon v. Horner CA4/3DinSFLA100% (1)

- Obduskey Brief in Opposition 17-1307Documento30 pagineObduskey Brief in Opposition 17-1307DinSFLA100% (1)

- Califorina ForeclosuresDocumento48 pagineCaliforina ForeclosuresCelebguard100% (1)

- CAAP 16 0000806sdoDocumento5 pagineCAAP 16 0000806sdoDinSFLANessuna valutazione finora

- Electronically Filed Supreme Court SCWC-15-0000005 09-OCT-2018 07:59 AMDocumento44 pagineElectronically Filed Supreme Court SCWC-15-0000005 09-OCT-2018 07:59 AMDinSFLA100% (1)

- Electronically Filed Intermediate Court of Appeals CAAP-16-0000042 21-DEC-2018 08:02 AMDocumento4 pagineElectronically Filed Intermediate Court of Appeals CAAP-16-0000042 21-DEC-2018 08:02 AMDinSFLA100% (1)

- Califorina ForeclosuresDocumento48 pagineCaliforina ForeclosuresCelebguard100% (1)

- D C O A O T S O F: Merlande Richard and Elie RichardDocumento5 pagineD C O A O T S O F: Merlande Richard and Elie RichardDinSFLANessuna valutazione finora

- Obduskey - Cert. Reply - FILEDDocumento15 pagineObduskey - Cert. Reply - FILEDDinSFLANessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- An Insider's Guide To SFTR For The Buy-SideDocumento12 pagineAn Insider's Guide To SFTR For The Buy-SideMalika DwarkaNessuna valutazione finora

- Srs ATMDocumento17 pagineSrs ATMsaitejaNessuna valutazione finora

- Water and Sanitation Services Company - WSSC D.I. Khan: Eligibility CriteriaDocumento4 pagineWater and Sanitation Services Company - WSSC D.I. Khan: Eligibility CriteriakabirNessuna valutazione finora

- Chap 006Documento4 pagineChap 006mallumainhunmailNessuna valutazione finora

- Billing BlockDocumento58 pagineBilling BlockSourav KumarNessuna valutazione finora

- Zoho - GoAir Ticket PDFDocumento2 pagineZoho - GoAir Ticket PDFJaikumar Janarthanan0% (1)

- "Role of SBI in The Indian Banking Sector" Presented By:-Karan Patel-201104100710010 Jignesh Mehta-201104100710048Documento10 pagine"Role of SBI in The Indian Banking Sector" Presented By:-Karan Patel-201104100710010 Jignesh Mehta-201104100710048Jignesh MehtaNessuna valutazione finora

- Legal EnglishDocumento8 pagineLegal EnglishJuliana Perez PolancoNessuna valutazione finora

- Mortgage - S. 58 TPADocumento3 pagineMortgage - S. 58 TPAAbhinav SrivastavNessuna valutazione finora

- Sabarimala Up Ticket 2Documento1 paginaSabarimala Up Ticket 2Ravi PattabiramanNessuna valutazione finora

- Glackin 1Documento64 pagineGlackin 1thestorydotieNessuna valutazione finora

- Cash ManagementDocumento79 pagineCash ManagementVinayaka Mc100% (3)

- Internship Report of Jamuna Bank About Loans & AdvanceDocumento60 pagineInternship Report of Jamuna Bank About Loans & AdvanceMd. Shahnaj Kader100% (3)

- KYC Know Your CustomerDocumento29 pagineKYC Know Your CustomerAsad AliNessuna valutazione finora

- Liquidity Analysis of Nepal Investment Bank LTDDocumento39 pagineLiquidity Analysis of Nepal Investment Bank LTDsuraj banNessuna valutazione finora

- Complete List of Indian Banks and Their Heads - CMDs - CEOs - Gr8AmbitionZ PDFDocumento8 pagineComplete List of Indian Banks and Their Heads - CMDs - CEOs - Gr8AmbitionZ PDFNageswara ReddyNessuna valutazione finora

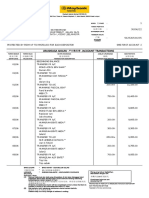

- Statement of Account - 08 - 25 - 16Documento3 pagineStatement of Account - 08 - 25 - 16Radhe ShyamNessuna valutazione finora

- TazaTicket PresentationDocumento13 pagineTazaTicket Presentationilyas shabbirNessuna valutazione finora

- Failure of Lehman Brothers: Jitendra SoniDocumento4 pagineFailure of Lehman Brothers: Jitendra Sonijitu222soni3386Nessuna valutazione finora

- Bank Code DUITNOW PAY TO ACCOUNT 2Documento1 paginaBank Code DUITNOW PAY TO ACCOUNT 2Mishhak MunanginNessuna valutazione finora

- Case Study R. Thyagarajan PDFDocumento65 pagineCase Study R. Thyagarajan PDFAnkit JainNessuna valutazione finora

- NRI Account Opening FormDocumento6 pagineNRI Account Opening FormAnkush JainNessuna valutazione finora

- Regulatory Framework - OutsourcingDocumento25 pagineRegulatory Framework - Outsourcingmohanp71Nessuna valutazione finora

- Agency Enrollment FormDocumento4 pagineAgency Enrollment FormprasannzaNessuna valutazione finora

- BA303 - Tutorial 10Documento2 pagineBA303 - Tutorial 10Vin ShyangNessuna valutazione finora

- Summer Internship Project Report Axis Bank For MBA StudentDocumento79 pagineSummer Internship Project Report Axis Bank For MBA StudentTrailer takNessuna valutazione finora

- MBBcurrent 562526534235 2022-06-30 PDFDocumento6 pagineMBBcurrent 562526534235 2022-06-30 PDFmuhamad faidzalNessuna valutazione finora

- Sample MemorandumDocumento3 pagineSample MemorandumchrisNessuna valutazione finora

- Conclusion It or EbankDocumento1 paginaConclusion It or EbankchandamatlaniNessuna valutazione finora

- 4305 01 PDFDocumento28 pagine4305 01 PDFSimra RiyazNessuna valutazione finora