Potrebbero piacerti anche

- World Bank Insider Blows Whistle On Corruption - Federal Reserve May 2013Documento8 pagineWorld Bank Insider Blows Whistle On Corruption - Federal Reserve May 2013CarrieonicNessuna valutazione finora

- Outline Foreclosure Defense - Tila & RespaDocumento13 pagineOutline Foreclosure Defense - Tila & RespaEdward BrownNessuna valutazione finora

- Fannie Mae Term Sheet For The Citigroup - New Century Mortgage Deal 2006-09-07 Cmlti 2006-NC2Documento50 pagineFannie Mae Term Sheet For The Citigroup - New Century Mortgage Deal 2006-09-07 Cmlti 2006-NC283jjmackNessuna valutazione finora

- FCA Citi Mortgage Complaint-In-InterventionDocumento36 pagineFCA Citi Mortgage Complaint-In-InterventionjodiebrittNessuna valutazione finora

- Class V III ProspectusDocumento209 pagineClass V III ProspectusCarrieonicNessuna valutazione finora

- SEC Vs Citigroup CDOs RMBS and Class V III Funding Comp-Pr2011-214Documento21 pagineSEC Vs Citigroup CDOs RMBS and Class V III Funding Comp-Pr2011-214CarrieonicNessuna valutazione finora

- Citigroup Whistle-Blower Says Bank's Brute Force' Hid Bad Loans From U.SDocumento5 pagineCitigroup Whistle-Blower Says Bank's Brute Force' Hid Bad Loans From U.SCarrieonicNessuna valutazione finora

- FHFA V Citigroup Inc. (09-02-11)Documento95 pagineFHFA V Citigroup Inc. (09-02-11)Master ChiefNessuna valutazione finora

- Bloomberg Markets Magazine - Citifraud July 2012Documento10 pagineBloomberg Markets Magazine - Citifraud July 2012CarrieonicNessuna valutazione finora

- r01c 079901Documento522 paginer01c 079901CarrieonicNessuna valutazione finora

- Citi V SMITH WDocumento4 pagineCiti V SMITH WCarrieonicNessuna valutazione finora

- In RE CitiGroup Inc Securities Litigation 1Documento547 pagineIn RE CitiGroup Inc Securities Litigation 1CarrieonicNessuna valutazione finora

- Citi Subsidiarys 2010 Exhibit 21-01Documento4 pagineCiti Subsidiarys 2010 Exhibit 21-01CarrieonicNessuna valutazione finora

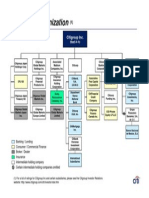

- Corp Struct CitigroupDocumento1 paginaCorp Struct CitigroupCarrieonicNessuna valutazione finora

- Citi Portfolio CorpDocumento2 pagineCiti Portfolio CorpCarrieonicNessuna valutazione finora

- Subsidiarys of Citigroup Inc. 2009 Exhibit21-01Documento5 pagineSubsidiarys of Citigroup Inc. 2009 Exhibit21-01CarrieonicNessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- A 2 - Roles and Functions of Various Participants in Financial MarketDocumento2 pagineA 2 - Roles and Functions of Various Participants in Financial MarketOsheen Singh100% (1)

- Bank ReconciliationDocumento2 pagineBank ReconciliationPatrick BacongalloNessuna valutazione finora

- IAE Student Prospective Guide San DiegoDocumento15 pagineIAE Student Prospective Guide San DiegoNatalia Díaz GarcíaNessuna valutazione finora

- Basel III Endgame 1682938205Documento147 pagineBasel III Endgame 1682938205rpk51088Nessuna valutazione finora

- Chanakya National Law University: Topic-Pledge and Hypothecation Subject - Law of Contract IiDocumento23 pagineChanakya National Law University: Topic-Pledge and Hypothecation Subject - Law of Contract IiashishNessuna valutazione finora

- Sbi Corporate Credit CardDocumento9 pagineSbi Corporate Credit CardArvindNessuna valutazione finora

- Assessment Jolly Amusements Commenced Operations in January With A Minigolf Course and Games Parlour. The AccountsDocumento23 pagineAssessment Jolly Amusements Commenced Operations in January With A Minigolf Course and Games Parlour. The AccountsPriti “Pihu” kumari AgarwalNessuna valutazione finora

- Third Div PNB Vs Pasimio 2015Documento16 pagineThird Div PNB Vs Pasimio 2015Jan Veah CaabayNessuna valutazione finora

- Statement of Fees 04 May 2023Documento4 pagineStatement of Fees 04 May 2023wendyclaridg75Nessuna valutazione finora

- Petty Cash Summary FillableDocumento7 paginePetty Cash Summary FillableLukman HakimNessuna valutazione finora

- Financial Literacy For StudentsDocumento34 pagineFinancial Literacy For StudentsLM FernandezNessuna valutazione finora

- GuggenheimDocumento5 pagineGuggenheimRochester Democrat and ChronicleNessuna valutazione finora

- Marketing Strategy of ICICI BankDocumento10 pagineMarketing Strategy of ICICI BankHunny VermaNessuna valutazione finora

- Unit 6: Rectification of Errors: Learning OutcomesDocumento32 pagineUnit 6: Rectification of Errors: Learning OutcomesKhushi MehtaNessuna valutazione finora

- Accounting Systems For Thrift Co-Operatives Promoted by Co-OperativeDocumento42 pagineAccounting Systems For Thrift Co-Operatives Promoted by Co-OperativemadhanagopalNessuna valutazione finora

- Economics Art IntegrationDocumento19 pagineEconomics Art IntegrationAditi AKNessuna valutazione finora

- TifrDocumento3 pagineTifrgrasheedNessuna valutazione finora

- ExportDocumento28 pagineExportNagarjun AithaNessuna valutazione finora

- Joshua P. Salce Bsabm Case Digest 6Documento2 pagineJoshua P. Salce Bsabm Case Digest 6Joshua P. SalceNessuna valutazione finora

- Global FinanceDocumento49 pagineGlobal FinanceAnisha JhawarNessuna valutazione finora

- On Buy Back of ShareDocumento30 pagineOn Buy Back of Shareranjay260Nessuna valutazione finora

- Unit - 3 Bank Reconciliation StatementDocumento21 pagineUnit - 3 Bank Reconciliation StatementMrutyunjay SaramandalNessuna valutazione finora

- Module 4 - Double Entry Bookkeeping System and The Accounting EquationDocumento9 pagineModule 4 - Double Entry Bookkeeping System and The Accounting EquationMark Christian BrlNessuna valutazione finora

- FINANCIAL-MARKETS Prelims RevDocumento13 pagineFINANCIAL-MARKETS Prelims RevJasmine TamayoNessuna valutazione finora

- MyTW Bill 900032858649 21 02 2022Documento5 pagineMyTW Bill 900032858649 21 02 2022avelik ukNessuna valutazione finora

- Balloon Loan Calculator: InputsDocumento9 pagineBalloon Loan Calculator: Inputsmy.nafi.pmp5283Nessuna valutazione finora

- How To Trade It For Serious Profit (Even If You're A Complete Beginner)Documento124 pagineHow To Trade It For Serious Profit (Even If You're A Complete Beginner)Johannes CajegasNessuna valutazione finora

- Yanapuma - Spanish Schools in QuitoDocumento9 pagineYanapuma - Spanish Schools in QuitoYanapuma SpanishNessuna valutazione finora

- Basics of Islamic BankingDocumento6 pagineBasics of Islamic BankingMnk BhkNessuna valutazione finora

- Cleaners WorksheetDocumento1 paginaCleaners WorksheetSeijuro Akashi100% (1)