Potrebbero piacerti anche

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

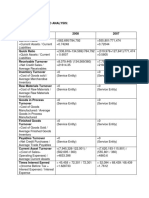

- Ratio Analysis Comparison Liberty Medical GroupDocumento3 pagineRatio Analysis Comparison Liberty Medical GroupAprile AnonuevoNessuna valutazione finora

- Risk Return Analysis of InvestmentDocumento3 pagineRisk Return Analysis of InvestmentAnju PrakashNessuna valutazione finora

- Differential Voting Rights ExplainedDocumento20 pagineDifferential Voting Rights ExplainedRohit Sharma100% (1)

- FIN-469 Investments Analysis Practice Set SolutionsDocumento7 pagineFIN-469 Investments Analysis Practice Set SolutionsGilbert Ansah YirenkyiNessuna valutazione finora

- FS For SKDocumento53 pagineFS For SKRaymond S. PacaldoNessuna valutazione finora

- Training ExercisesDocumento4 pagineTraining ExercisesnyNessuna valutazione finora

- Markets With Frictions: Banks: Guido MenzioDocumento36 pagineMarkets With Frictions: Banks: Guido MenzioDaniel GavidiaNessuna valutazione finora

- Long QuestionsDocumento18 pagineLong Questionssaqlainra50% (2)

- F&N StrengthDocumento232 pagineF&N StrengthMat ProNessuna valutazione finora

- Prudential Financial and Asset Liability ManagementDocumento13 paginePrudential Financial and Asset Liability ManagementYash Agarwal0% (2)

- PSABDocumento3 paginePSABHotman JeffersonNessuna valutazione finora

- Interloop LimitedDocumento7 pagineInterloop LimitedHamza SiddiquiNessuna valutazione finora

- Dr. SchekterDocumento5 pagineDr. SchekterRaja Shaban Qamer Mukhlis100% (1)

- FRP FinalDocumento88 pagineFRP Finalgeeta44Nessuna valutazione finora

- Financing Methods in Professional Football: Dr. Zoltán Imre NagyDocumento19 pagineFinancing Methods in Professional Football: Dr. Zoltán Imre NagyaldywsNessuna valutazione finora

- Interim Order in The Matter of Real Vision International Limited.Documento13 pagineInterim Order in The Matter of Real Vision International Limited.Shyam SunderNessuna valutazione finora

- Introduction To Finance 1Documento11 pagineIntroduction To Finance 1skrzakNessuna valutazione finora

- What Are The Stocks You Have in Your Long Term Portfolio - QuoraDocumento3 pagineWhat Are The Stocks You Have in Your Long Term Portfolio - QuoraAchint KumarNessuna valutazione finora

- A Students Guide To Group Accounts PDFDocumento15 pagineA Students Guide To Group Accounts PDFSyed Ahmad100% (1)

- Financialreportingdevelopments Bb2634 Equitymethodinvestments 15october2013Documento150 pagineFinancialreportingdevelopments Bb2634 Equitymethodinvestments 15october2013tieuquan42Nessuna valutazione finora

- Yell FinalDocumento10 pagineYell Finalbumz1234100% (2)

- Derivatives Interview QuestionsDocumento14 pagineDerivatives Interview Questionsanil100% (3)

- Financial Management - PPT - 2011Documento183 pagineFinancial Management - PPT - 2011ashpika100% (1)

- Exchange Traded Funds: There Are Safer Ways To Invest in Stocks Rebounding Up From LowsDocumento1 paginaExchange Traded Funds: There Are Safer Ways To Invest in Stocks Rebounding Up From LowsRajeshbhai vaghaniNessuna valutazione finora

- 4 5917794287629633159Documento44 pagine4 5917794287629633159alexbemuNessuna valutazione finora

- Bonus Assignment 2Documento4 pagineBonus Assignment 2Zain Zulfiqar67% (3)

- Brigade Enterprises LimitedDocumento36 pagineBrigade Enterprises LimitedAnkur MittalNessuna valutazione finora

- Error RecognitionDocumento9 pagineError RecognitionRisa Nanda YusarNessuna valutazione finora

- LN10 Titman 479536 Valuation 03 LN10Documento48 pagineLN10 Titman 479536 Valuation 03 LN10Sta Ker100% (1)