Potrebbero piacerti anche

- Authors: 1. Dr. Parimal Kr. SenDocumento8 pagineAuthors: 1. Dr. Parimal Kr. SenDebojyoti DasNessuna valutazione finora

- Foreign Investment in IndiaDocumento11 pagineForeign Investment in IndiaMandar BorkarNessuna valutazione finora

- Attracting Foreign Direct Investment (FDI) To IndiaDocumento30 pagineAttracting Foreign Direct Investment (FDI) To IndiamintukNessuna valutazione finora

- Fdi and FiisDocumento38 pagineFdi and Fiisssneha1989Nessuna valutazione finora

- Tajikistan: Promoting Export Diversification and GrowthDa EverandTajikistan: Promoting Export Diversification and GrowthNessuna valutazione finora

- China Inside Out: China Going Global: Key TrendsDocumento40 pagineChina Inside Out: China Going Global: Key TrendsTon ChockNessuna valutazione finora

- FDI's Impact On Indian EconomyDocumento3 pagineFDI's Impact On Indian Economypwd001Nessuna valutazione finora

- FDI in IndiaDocumento4 pagineFDI in IndiaPratik RambhiaNessuna valutazione finora

- Economic Indicators for East Asia: Input–Output TablesDa EverandEconomic Indicators for East Asia: Input–Output TablesNessuna valutazione finora

- Submitted By: Ananya Mishra Khushbu Aggarwala Nilofar Naaz Priyadarshi Mohanty Sushovit Sarthak Simli MisraDocumento27 pagineSubmitted By: Ananya Mishra Khushbu Aggarwala Nilofar Naaz Priyadarshi Mohanty Sushovit Sarthak Simli MisrasimlimisraNessuna valutazione finora

- Factors Affecting The Export Intensity of Chinese Manufacturing FirmDocumento24 pagineFactors Affecting The Export Intensity of Chinese Manufacturing Firmmtahir777945Nessuna valutazione finora

- Foreign Direct InvestmentDocumento7 pagineForeign Direct InvestmentShivani SharmaNessuna valutazione finora

- Tcs v. InfosysDocumento40 pagineTcs v. Infosysneetapai3859Nessuna valutazione finora

- Please Read: A Personal Appeal From A Wikipedia Contributor of 18,000 EditsDocumento8 paginePlease Read: A Personal Appeal From A Wikipedia Contributor of 18,000 EditsRakesh SharmaNessuna valutazione finora

- Low Soo Peng Singapore BusinessDocumento16 pagineLow Soo Peng Singapore BusinessLow Soo PengNessuna valutazione finora

- Sapm Final DeckDocumento45 pagineSapm Final DeckShasank JalanNessuna valutazione finora

- Indian Economy Opportunities Unlimited: Click To Edit Master Subtitle StyleDocumento15 pagineIndian Economy Opportunities Unlimited: Click To Edit Master Subtitle StyleShivang UnadkatNessuna valutazione finora

- India & Development: 14 March 2013Documento62 pagineIndia & Development: 14 March 2013nagmaniii26Nessuna valutazione finora

- 10 DK Jha CGDocumento4 pagine10 DK Jha CGdkrirayNessuna valutazione finora

- FdiDocumento7 pagineFdiankit109Nessuna valutazione finora

- M & A Fisrt DraftDocumento19 pagineM & A Fisrt Draftrahul422Nessuna valutazione finora

- Foreign Direct Investment and Its Impact: Vivekanandha College of Arts and Sciences For Womens ElayampalayamDocumento8 pagineForeign Direct Investment and Its Impact: Vivekanandha College of Arts and Sciences For Womens Elayampalayamanon_209785390Nessuna valutazione finora

- Status Indian Auto IndustryDocumento31 pagineStatus Indian Auto Industrymanjas234Nessuna valutazione finora

- Current Status of FdiDocumento9 pagineCurrent Status of FdiGrishma KothariNessuna valutazione finora

- Financial Soundness Indicators for Financial Sector Stability in Viet NamDa EverandFinancial Soundness Indicators for Financial Sector Stability in Viet NamNessuna valutazione finora

- Infosys vs. TcsDocumento30 pagineInfosys vs. TcsRohit KumarNessuna valutazione finora

- Study of Impact of Fdi On Indian Economy: Dr. D.B. Bhanagade Dr. Pallavi A. ShahDocumento4 pagineStudy of Impact of Fdi On Indian Economy: Dr. D.B. Bhanagade Dr. Pallavi A. ShahDeepti GyanchandaniNessuna valutazione finora

- Implications of Foreign Trade Policy and Facilitation of Foreign TradeDocumento32 pagineImplications of Foreign Trade Policy and Facilitation of Foreign TradeTamal BiswasNessuna valutazione finora

- Exim Bank NFTP PresentationDocumento30 pagineExim Bank NFTP PresentationSagar GadaNessuna valutazione finora

- Reserve Bank of IndiaDocumento45 pagineReserve Bank of IndiaAamir SaleemNessuna valutazione finora

- Piper Jaffray FinalDocumento32 paginePiper Jaffray FinalGirish VarmaNessuna valutazione finora

- BSB119 COUNTRY ANALYSIS - FinalDocumento18 pagineBSB119 COUNTRY ANALYSIS - FinalAshleigh KindredNessuna valutazione finora

- Impact of MNCs On Indian EconomyDocumento37 pagineImpact of MNCs On Indian EconomyShrey Sampat0% (1)

- India PresentationDocumento84 pagineIndia Presentationnishantraj94Nessuna valutazione finora

- Foreign Direct Investment: Presenter: Pankaj GaurDocumento15 pagineForeign Direct Investment: Presenter: Pankaj GaurNikhil AlwalNessuna valutazione finora

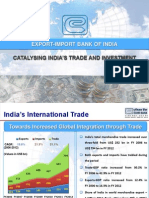

- Export-Import Bank of India: Catalysing India'S Trade and InvestmentDocumento9 pagineExport-Import Bank of India: Catalysing India'S Trade and Investmentashu9026Nessuna valutazione finora

- F.D.I. in India: Suneel GuptaDocumento37 pagineF.D.I. in India: Suneel GuptaYash PatelNessuna valutazione finora

- Live Project: Financial Planning For Hawkers GROUP 4 (PG SEC-B 2011-2012)Documento15 pagineLive Project: Financial Planning For Hawkers GROUP 4 (PG SEC-B 2011-2012)Shakthi ShankaranNessuna valutazione finora

- GIFT Corporate PresentationDocumento10 pagineGIFT Corporate PresentationRom LeeNessuna valutazione finora

- Business Research Report On Retail Sector: Prof. S.P.KETKARDocumento15 pagineBusiness Research Report On Retail Sector: Prof. S.P.KETKARRadhika BhardwajNessuna valutazione finora

- FDI in IndiaDocumento22 pagineFDI in IndiachaturvediprateekNessuna valutazione finora

- Article 2b - 2021-22 - FDI in IndiaDocumento4 pagineArticle 2b - 2021-22 - FDI in IndiaKiniNessuna valutazione finora

- Gagbm2023 308 315Documento8 pagineGagbm2023 308 315MarkWeberNessuna valutazione finora

- (Approved by AICTE, New Delhi & Affiliated To Rajasthan Technical University, KotaDocumento13 pagine(Approved by AICTE, New Delhi & Affiliated To Rajasthan Technical University, KotaNeelu Tuteja NikhanjNessuna valutazione finora

- Presentation Impact of Economic Liberal Is at Ion On Indian248Documento34 paginePresentation Impact of Economic Liberal Is at Ion On Indian248Mukesh PanwarNessuna valutazione finora

- State of Venture Capital - October 2004Documento19 pagineState of Venture Capital - October 2004Vinit SonawaneNessuna valutazione finora

- Foreign Direct Investment in IndiaDocumento6 pagineForeign Direct Investment in IndiaIOSRjournalNessuna valutazione finora

- IB - Doing Business in China - 2011Documento27 pagineIB - Doing Business in China - 2011Srikanth Kumar KonduriNessuna valutazione finora

- Preface To The Information TechnologyDocumento12 paginePreface To The Information TechnologyGrieshma CherianNessuna valutazione finora

- Impact of Globalization On Indian EconomyDocumento33 pagineImpact of Globalization On Indian EconomySrikanth ReddyNessuna valutazione finora

- Essay On FDIDocumento10 pagineEssay On FDIpagluNessuna valutazione finora

- Oreign Direct InvestmentDocumento4 pagineOreign Direct InvestmentJvsn ReddyNessuna valutazione finora

- Mba Bms Foreign InvestmentsDocumento19 pagineMba Bms Foreign InvestmentsAkash HalankarNessuna valutazione finora

- FDI in China Dullien 2005Documento29 pagineFDI in China Dullien 2005Hans Grungilungi ChristianNessuna valutazione finora

- Foreign Direct InvestmentDocumento11 pagineForeign Direct InvestmentSuraj SinghNessuna valutazione finora

- Document 9Documento91 pagineDocument 9Amol MahajanNessuna valutazione finora

- Ranking India's Transnational CompaniesDocumento9 pagineRanking India's Transnational CompaniesdualballersNessuna valutazione finora

- Session 20-21 Final - Open Economy MacroeconomicsDocumento76 pagineSession 20-21 Final - Open Economy MacroeconomicsBbbbbNessuna valutazione finora

- HDFCDocumento78 pagineHDFCsam04050Nessuna valutazione finora

- Annual 030502Documento40 pagineAnnual 030502Ajay DesaiNessuna valutazione finora

- PricelistDocumento3 paginePricelist4 fruit companyNessuna valutazione finora

- 5-Minute Chocolate Balls PDFDocumento10 pagine5-Minute Chocolate Balls PDFDiana ArunNessuna valutazione finora

- Rufino Tan Vs Ramon Del RosarioDocumento1 paginaRufino Tan Vs Ramon Del RosarioJocelyn MagbanuaNessuna valutazione finora

- Ticket PDFDocumento1 paginaTicket PDFVenkatesh VakamulluNessuna valutazione finora

- Business Level StrategyDocumento28 pagineBusiness Level StrategyMohammad Raihanul HasanNessuna valutazione finora

- Retainage Release Invoices in Oracle AP - ErpSchoolsDocumento9 pagineRetainage Release Invoices in Oracle AP - ErpSchoolsK.rajesh Kumar ReddyNessuna valutazione finora

- Harish NatarajanDocumento10 pagineHarish NatarajanbananiacorpNessuna valutazione finora

- Sfo ShippersDocumento2 pagineSfo ShippersNishant ChandraNessuna valutazione finora

- Apartment Community BrochureDocumento7 pagineApartment Community Brochureapi-327678777Nessuna valutazione finora

- Air India - Balance Score CardDocumento6 pagineAir India - Balance Score Cardramyavenugopal100% (1)

- EnglishtoMath##1Documento8 pagineEnglishtoMath##1zubairNessuna valutazione finora

- Fundraising Blueprint Plan TemplateDocumento3 pagineFundraising Blueprint Plan Templateoxade21Nessuna valutazione finora

- SOLAS - Verified Gross Mass (VGM)Documento2 pagineSOLAS - Verified Gross Mass (VGM)Mary Joy Dela MasaNessuna valutazione finora

- Case Study-1 SHEENADocumento2 pagineCase Study-1 SHEENARushikesh Dandagwhal100% (1)

- Accounting For NotesDocumento3 pagineAccounting For NotesRaffay MaqboolNessuna valutazione finora

- PGM-199 R1Documento5 paginePGM-199 R1Faraz Ali Khan0% (1)

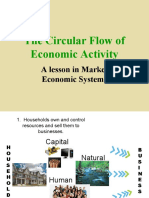

- Circular FlowDocumento21 pagineCircular FlowSheryl BorromeoNessuna valutazione finora

- Brand Licensing PDFDocumento3 pagineBrand Licensing PDFalberto micheliniNessuna valutazione finora

- Chapter 7Documento18 pagineChapter 7dheerajm88Nessuna valutazione finora

- VisuSon - Business Stress TestingDocumento7 pagineVisuSon - Business Stress TestingAmira Nur Afiqah Agus SalimNessuna valutazione finora

- Appendix 8 - Instructions - RAPALDocumento1 paginaAppendix 8 - Instructions - RAPALTesa GDNessuna valutazione finora

- StartUp India - Case AnalysisDocumento3 pagineStartUp India - Case AnalysisIrshad AzeezNessuna valutazione finora

- Diebold Case StudyDocumento2 pagineDiebold Case StudySagnik Debnath67% (3)

- Uganda Bureau of Statistics Census of Business Establishments, 2010/11 Report OnDocumento169 pagineUganda Bureau of Statistics Census of Business Establishments, 2010/11 Report OnCano KaluNessuna valutazione finora

- TWSS CFA Level I - Planner and TrackerDocumento6 pagineTWSS CFA Level I - Planner and TrackerSai Ranjit TummalapalliNessuna valutazione finora

- Short AnswerDocumento4 pagineShort AnswerMichiko Kyung-soonNessuna valutazione finora

- Bangkok Retail 4q13Documento1 paginaBangkok Retail 4q13Bea LorinczNessuna valutazione finora

- Gat PreparationDocumento21 pagineGat PreparationHAFIZ IMRAN AKHTERNessuna valutazione finora

- Capital StructureDocumento44 pagineCapital Structure26155152Nessuna valutazione finora

- Walt Disney Company PDFDocumento20 pagineWalt Disney Company PDFGabriella VenturinaNessuna valutazione finora