Potrebbero piacerti anche

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Court suit for unpaid Rs. amountDocumento3 pagineCourt suit for unpaid Rs. amountIndranil Roy Choudhuri100% (1)

- The Impact of Urban Land Taxation: The Pittsburgh ExperienceDocumento22 pagineThe Impact of Urban Land Taxation: The Pittsburgh ExperienceFrancisco RodríguezNessuna valutazione finora

- German Hyperinflation-Case 3Documento17 pagineGerman Hyperinflation-Case 3MAYANK YADAV 22GSOB2010351Nessuna valutazione finora

- APQP by Rajeev For Beginners Existing Professionals 1687347193Documento15 pagineAPQP by Rajeev For Beginners Existing Professionals 1687347193Saroj KumarNessuna valutazione finora

- The 10 Types of Pricing StrategiesDocumento9 pagineThe 10 Types of Pricing Strategieskhalid100% (1)

- Theories Chapter 1Documento16 pagineTheories Chapter 1Farhana GuiandalNessuna valutazione finora

- INDICATORSDocumento10 pagineINDICATORSadam.szafranskijdNessuna valutazione finora

- Elanza Export Private Limited: Company ProfileDocumento9 pagineElanza Export Private Limited: Company ProfileKapil SinghNessuna valutazione finora

- Residential Lease Application: Each Occupant and Co-Applicant 18 Years or Older Must Submit A Separate ApplicationDocumento4 pagineResidential Lease Application: Each Occupant and Co-Applicant 18 Years or Older Must Submit A Separate ApplicationMichael KeplingerNessuna valutazione finora

- Chapter 05 Solution of Fundamental of Financial Accouting by EDMONDS (4th Edition)Documento196 pagineChapter 05 Solution of Fundamental of Financial Accouting by EDMONDS (4th Edition)Awais Azeemi100% (3)

- Case 3C - Papa Gino'sDocumento2 pagineCase 3C - Papa Gino'sPatrixia Nyah MifloresNessuna valutazione finora

- ABC Audit Representation LetterDocumento3 pagineABC Audit Representation LetterMatthew TsangNessuna valutazione finora

- Industrial Management Course at Addis Ababa UniversityDocumento2 pagineIndustrial Management Course at Addis Ababa UniversityAman KemalNessuna valutazione finora

- Letter of Engagement Draft Vlad's Emporium LimitedDocumento33 pagineLetter of Engagement Draft Vlad's Emporium LimitedNatali DavydenkoNessuna valutazione finora

- Multifamily Acquisition ModelDocumento4 pagineMultifamily Acquisition Modelw_fibNessuna valutazione finora

- Tumulak, Nichole G. A-234 20577396Documento3 pagineTumulak, Nichole G. A-234 20577396Nichole TumulakNessuna valutazione finora

- Value Chain Analysis HandbookandToolkitDocumento164 pagineValue Chain Analysis HandbookandToolkitBùi Thị Thu HồngNessuna valutazione finora

- 2021 07 24 - Statement 1.pdf PDF ExpertDocumento2 pagine2021 07 24 - Statement 1.pdf PDF ExpertMiki CristinaNessuna valutazione finora

- Research Paper About Food Cart BusinessDocumento4 pagineResearch Paper About Food Cart Businessgw2g2v5p100% (1)

- Linear Asset Management - Operation Level Costing - Pipe VersionDocumento86 pagineLinear Asset Management - Operation Level Costing - Pipe VersionAnil KumarNessuna valutazione finora

- Derivatives Instruments... by Muhammad Al-Bashir M Al-AmineDocumento45 pagineDerivatives Instruments... by Muhammad Al-Bashir M Al-Aminevishvasa11Nessuna valutazione finora

- MKTM503 Ca2Documento9 pagineMKTM503 Ca2vishvjeet singh panwarNessuna valutazione finora

- Project Integration Management Key to Overall SuccessDocumento71 pagineProject Integration Management Key to Overall SuccessMustefa MohammedNessuna valutazione finora

- Landscope (Mauritius) LTD PDFDocumento6 pagineLandscope (Mauritius) LTD PDFircmruNessuna valutazione finora

- T.RAMA KRISHANA RAO (8839271225) Contact For: - Cat, Bank, MbaDocumento35 pagineT.RAMA KRISHANA RAO (8839271225) Contact For: - Cat, Bank, MbaRam KrishnaNessuna valutazione finora

- Anti-Corruption and Bribery Policy - Globeleq CameroonDocumento24 pagineAnti-Corruption and Bribery Policy - Globeleq CameroonhappiNessuna valutazione finora

- OMNIBUS SWORN STATEMENT SampleDocumento2 pagineOMNIBUS SWORN STATEMENT SampleDodong Timbal100% (6)

- Chapter 3Documento2 pagineChapter 3marisNessuna valutazione finora

- 300 Best Mcqs April Part-1: Important DaysDocumento18 pagine300 Best Mcqs April Part-1: Important DaysKeshavVashisthaNessuna valutazione finora

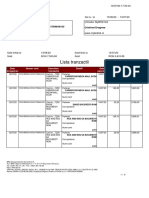

- Lista Tranzactii: Cristinel Dragnea RO81BRDE410SV31789944100 RON Cristinel DragneaDocumento6 pagineLista Tranzactii: Cristinel Dragnea RO81BRDE410SV31789944100 RON Cristinel DragneaSebastian PSNessuna valutazione finora