Potrebbero piacerti anche

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- GST Book Bank AnswersDocumento10 pagineGST Book Bank AnswersAditya DasNessuna valutazione finora

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- Invoice Capture Centre 7.5 SP4 Customizing GuideDocumento221 pagineInvoice Capture Centre 7.5 SP4 Customizing Guideanon_15121315Nessuna valutazione finora

- Tax Invoice SummaryDocumento11 pagineTax Invoice SummaryMahesh Daxini Thakker0% (1)

- TAXATION 2 Chapter 10 Value Added TaxDocumento7 pagineTAXATION 2 Chapter 10 Value Added TaxKim Cristian MaañoNessuna valutazione finora

- 53 Summary On Vat CST and WCTDocumento16 pagine53 Summary On Vat CST and WCTYogesh DeokarNessuna valutazione finora

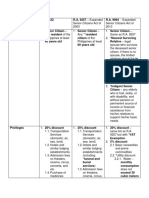

- Title R.A. 7432 R.A. 9257 R.A. 9994 - ExpandedDocumento11 pagineTitle R.A. 7432 R.A. 9257 R.A. 9994 - ExpandedAngel Alejo AcobaNessuna valutazione finora

- SC Rules on Transitional Input Tax CreditDocumento2 pagineSC Rules on Transitional Input Tax CreditVel JuneNessuna valutazione finora

- July 3, 2018: Hermilando Mandanas, Et Al., Petitioners Executive Secretary Paquito Ochoa, Et Al., RespondentsDocumento3 pagineJuly 3, 2018: Hermilando Mandanas, Et Al., Petitioners Executive Secretary Paquito Ochoa, Et Al., RespondentsDayanarah MarandaNessuna valutazione finora

- Module 4 - Value Added TaxDocumento16 pagineModule 4 - Value Added Taxanon_455551365Nessuna valutazione finora

- Liquigaz Philippines Corp. Vs CIR, CTA EB Nos. 1117 and 1119Documento3 pagineLiquigaz Philippines Corp. Vs CIR, CTA EB Nos. 1117 and 1119brendamanganaanNessuna valutazione finora

- Doing Mining Business EnglishDocumento29 pagineDoing Mining Business EnglishAmrinder6Nessuna valutazione finora

- Taxation 3A Assignment 2023Documento5 pagineTaxation 3A Assignment 2023CodyxanssNessuna valutazione finora

- © The Institute of Chartered Accountants of IndiaDocumento3 pagine© The Institute of Chartered Accountants of IndiaDeepak KumarNessuna valutazione finora

- M1 Sep PDFDocumento4 pagineM1 Sep PDFShanmugamNessuna valutazione finora

- Mushak-9.1 VAT Return On 11.JAN.2023Documento6 pagineMushak-9.1 VAT Return On 11.JAN.2023Mac TanzinNessuna valutazione finora

- GCSE 1MA1 - Best Value For Money Mark SchemeDocumento17 pagineGCSE 1MA1 - Best Value For Money Mark SchemeArchit GuptaNessuna valutazione finora

- Invoice - (Cell of Mitutoyo Vernier)Documento1 paginaInvoice - (Cell of Mitutoyo Vernier)Nitish SinghNessuna valutazione finora

- Product Design workflow and field definitionsDocumento60 pagineProduct Design workflow and field definitionsKamran MallickNessuna valutazione finora

- TRAIN LAW UPDATES INCOME TAX RATESDocumento23 pagineTRAIN LAW UPDATES INCOME TAX RATESNikki Estores GonzalesNessuna valutazione finora

- Unit Computation Sheet: Payment SchemesDocumento4 pagineUnit Computation Sheet: Payment SchemesGEN888 IGNessuna valutazione finora

- Questionnaire On GSTDocumento7 pagineQuestionnaire On GSTGourav Pareek100% (1)

- Paleco - BaseportDocumento20 paginePaleco - BaseportAllan P. AborotNessuna valutazione finora

- Financial StatemnetDocumento23 pagineFinancial Statemnetmelaniekudo100% (1)

- Special Lecture Handouts in TaxationDocumento24 pagineSpecial Lecture Handouts in TaxationTep DomingoNessuna valutazione finora

- Minimum Wages and Taxes Concerns of Filipino EntrepreneursDocumento63 pagineMinimum Wages and Taxes Concerns of Filipino EntrepreneursMarie Nicole SalmasanNessuna valutazione finora

- Contractor GCC 2013Documento142 pagineContractor GCC 2013SCReddy0% (1)

- RR No. 15-2018 PDFDocumento2 pagineRR No. 15-2018 PDFmark linganNessuna valutazione finora

- Italy Off Plan Property Investment and OpportunitiesDocumento16 pagineItaly Off Plan Property Investment and Opportunitiespropertyinvestment100% (2)

- Ey 2018 Worldwide RD Incentives Reference Guide PDFDocumento412 pagineEy 2018 Worldwide RD Incentives Reference Guide PDFGaurav KohliNessuna valutazione finora

- Taxation 1Documento11 pagineTaxation 1graciaNessuna valutazione finora