Potrebbero piacerti anche

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Tratamentul Total Al CanceruluiDocumento71 pagineTratamentul Total Al CanceruluiAntal98% (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (894)

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- US Internal Revenue Service: 2290rulesty2007v4 0Documento6 pagineUS Internal Revenue Service: 2290rulesty2007v4 0IRSNessuna valutazione finora

- Tratamentul Total Al CanceruluiDocumento71 pagineTratamentul Total Al CanceruluiAntal98% (98)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- 2008 Objectives Report To Congress v2Documento153 pagine2008 Objectives Report To Congress v2IRSNessuna valutazione finora

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 2008 Credit Card Bulk Provider RequirementsDocumento112 pagine2008 Credit Card Bulk Provider RequirementsIRSNessuna valutazione finora

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Tratamentul Total Al CanceruluiDocumento71 pagineTratamentul Total Al CanceruluiAntal98% (98)

- Tratamentul Total Al CanceruluiDocumento71 pagineTratamentul Total Al CanceruluiAntal98% (98)

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 2008 Data DictionaryDocumento260 pagine2008 Data DictionaryIRSNessuna valutazione finora

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Tratamentul Total Al CanceruluiDocumento71 pagineTratamentul Total Al CanceruluiAntal98% (98)

- 6th Central Pay Commission Salary CalculatorDocumento15 pagine6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Chapter 2 and 3 Lopez BookDocumento4 pagineChapter 2 and 3 Lopez BookSam CorsigaNessuna valutazione finora

- Case 8 - 2 - 826315Documento4 pagineCase 8 - 2 - 826315fitriNessuna valutazione finora

- Advantages of Multinational CompaniesDocumento20 pagineAdvantages of Multinational CompaniesPraveen Kumar PiarNessuna valutazione finora

- ESCRA - Malayan Insurance vs. St. FrancisDocumento72 pagineESCRA - Malayan Insurance vs. St. FrancisGuiller MagsumbolNessuna valutazione finora

- Integrichain Offer Letter ArtifactDocumento3 pagineIntegrichain Offer Letter Artifactapi-449844328Nessuna valutazione finora

- Pinto Pm2 Ch03Documento22 paginePinto Pm2 Ch03Focus ArthamediaNessuna valutazione finora

- About Warren BuffetDocumento14 pagineAbout Warren BuffetPadregarcia Mps100% (1)

- CH 04Documento110 pagineCH 04Angela Kuswandi100% (1)

- Kesan Hair Oil 1Documento27 pagineKesan Hair Oil 1AlpeshNessuna valutazione finora

- Rbi 8 % Bond TdsDocumento3 pagineRbi 8 % Bond TdssunnycccccNessuna valutazione finora

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Project Report for a 500 Bird Per Week Broiler Poultry FarmDocumento3 pagineProject Report for a 500 Bird Per Week Broiler Poultry FarmRajesh Jangir100% (1)

- CURRICULUM VITAE-FP SPV Tax Widasa Group Update 2Documento11 pagineCURRICULUM VITAE-FP SPV Tax Widasa Group Update 2febrikafitriantiNessuna valutazione finora

- Marks and Spencer Marketing MixDocumento27 pagineMarks and Spencer Marketing MixTushar Sharma50% (4)

- Sales ManagementDocumento185 pagineSales Managementzhuntar100% (1)

- REALLY MODIFIED DU PONT ANALYSIS: FIVE WAYS TO IMPROVE RETURN ON EQUITYDocumento5 pagineREALLY MODIFIED DU PONT ANALYSIS: FIVE WAYS TO IMPROVE RETURN ON EQUITYKhadija NalghatNessuna valutazione finora

- Disney CaseDocumento4 pagineDisney CaseMedrx TradingNessuna valutazione finora

- Standardize Cosmo's Balance SheetDocumento5 pagineStandardize Cosmo's Balance SheetRakshit SharmaNessuna valutazione finora

- Financial Accounting 2 Assignment 2Documento3 pagineFinancial Accounting 2 Assignment 2BhodzaNessuna valutazione finora

- All Template Chapter 6 As of September 10 2019Documento32 pagineAll Template Chapter 6 As of September 10 2019Aira Dizon50% (2)

- Transfer of Property Act - BelDocumento36 pagineTransfer of Property Act - Belshaikhnazneen67% (3)

- Cash Flow Statement GuideDocumento37 pagineCash Flow Statement GuideAshekin MahadiNessuna valutazione finora

- P1.PROO - .L Question CMA September 2022 ExaminationDocumento7 pagineP1.PROO - .L Question CMA September 2022 ExaminationS.M.A AwalNessuna valutazione finora

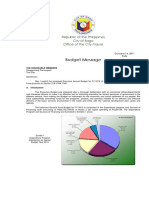

- Bago City 2012 Budget MessageDocumento3 pagineBago City 2012 Budget MessageAl SimbajonNessuna valutazione finora

- Total Care Foundation by LawsDocumento6 pagineTotal Care Foundation by LawstotalcareinternationalNessuna valutazione finora

- Chapter 12 Capital Marketing ResearchDocumento11 pagineChapter 12 Capital Marketing ResearchThomas HWNessuna valutazione finora

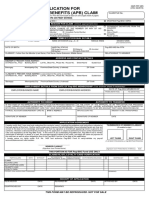

- Pag-IBIG Provident Benefits Claim FormDocumento2 paginePag-IBIG Provident Benefits Claim FormCarlo Beltran Valerio0% (2)

- Ms - MuffDocumento17 pagineMs - MuffDayuman LagasiNessuna valutazione finora

- Lone Pine Cafe-CaseDocumento28 pagineLone Pine Cafe-CaseNadya Rizkita100% (2)

- Final Exam Sample1Documento21 pagineFinal Exam Sample1JiaFengNessuna valutazione finora

- How Much Is The Distributable Income of The GPP?Documento2 pagineHow Much Is The Distributable Income of The GPP?Katrina Dela CruzNessuna valutazione finora

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingDa EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingValutazione: 4.5 su 5 stelle4.5/5 (97)

- Buffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorDa EverandBuffettology: The Previously Unexplained Techniques That Have Made Warren Buffett American's Most Famous InvestorValutazione: 4.5 su 5 stelle4.5/5 (132)

- Getting Through: Cold Calling Techniques To Get Your Foot In The DoorDa EverandGetting Through: Cold Calling Techniques To Get Your Foot In The DoorValutazione: 4.5 su 5 stelle4.5/5 (63)

- Disloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpDa EverandDisloyal: A Memoir: The True Story of the Former Personal Attorney to President Donald J. TrumpValutazione: 4 su 5 stelle4/5 (214)

- Introduction to Negotiable Instruments: As per Indian LawsDa EverandIntroduction to Negotiable Instruments: As per Indian LawsValutazione: 5 su 5 stelle5/5 (1)