Potrebbero piacerti anche

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Uber Service AuditDocumento12 pagineUber Service AuditAdeelNessuna valutazione finora

- DSE ClearingDocumento6 pagineDSE ClearingMohammed Anwaruzzaman100% (1)

- AMUL's Distribution ChannelDocumento16 pagineAMUL's Distribution ChannelPrateek Jain100% (1)

- Case Study Market LeadershipDocumento5 pagineCase Study Market LeadershipDanish RehmanNessuna valutazione finora

- Auto Trend ForecasterDocumento15 pagineAuto Trend ForecasterherbakNessuna valutazione finora

- BFSI Clients ListDocumento3 pagineBFSI Clients ListSarita JoshiNessuna valutazione finora

- Factors Affecting Promotion Mix - Top 10 Factors Affecting Promotion MixDocumento49 pagineFactors Affecting Promotion Mix - Top 10 Factors Affecting Promotion MixJoyjit SanyalNessuna valutazione finora

- IA1 Cash and Cash EquivalentsDocumento20 pagineIA1 Cash and Cash EquivalentsJohn Rainier QuijadaNessuna valutazione finora

- Chapter 4 Marketing Department: Company 1-Apollo Hospitals Enterprises LTD (Apollo)Documento20 pagineChapter 4 Marketing Department: Company 1-Apollo Hospitals Enterprises LTD (Apollo)TYB92BINDRA GURSHEEN KAUR R.Nessuna valutazione finora

- Food Truck Business Plan Instructions Rubric-1Documento4 pagineFood Truck Business Plan Instructions Rubric-1Lara WNessuna valutazione finora

- Entrepreneur Development NotesDocumento20 pagineEntrepreneur Development NotesAnish YadavNessuna valutazione finora

- Vikash Kumar LL.M Dissertation 2022Documento145 pagineVikash Kumar LL.M Dissertation 2022Raj SinhaNessuna valutazione finora

- USJ-R College of Commerce - Acctg 101 RM 403 MWF 8:30 AM - 10:30 AM - NEF, CPADocumento3 pagineUSJ-R College of Commerce - Acctg 101 RM 403 MWF 8:30 AM - 10:30 AM - NEF, CPAJerah Marie PepitoNessuna valutazione finora

- Merger and AcquisitionDocumento4 pagineMerger and Acquisitionshady emadNessuna valutazione finora

- Mondelez: Sales and Distribution ReportDocumento17 pagineMondelez: Sales and Distribution ReportSaumya MittalNessuna valutazione finora

- Call Letter 1-41Documento41 pagineCall Letter 1-41majeedkalavNessuna valutazione finora

- Session1 gnp1112Documento24 pagineSession1 gnp1112Santosh MishraNessuna valutazione finora

- Swift MT RulesDocumento2 pagineSwift MT RulesJit JackNessuna valutazione finora

- Project Report MyDocumento102 pagineProject Report MySana MoidNessuna valutazione finora

- Aos287-2951631991 (ABET)Documento9 pagineAos287-2951631991 (ABET)Elisabet Permata SariNessuna valutazione finora

- Strategies in Media Planning PDFDocumento6 pagineStrategies in Media Planning PDFSaraNessuna valutazione finora

- Mini Case - Blades - Decision To Expand InternationallyDocumento2 pagineMini Case - Blades - Decision To Expand InternationallyTrường Nguyễn VănNessuna valutazione finora

- Business Plan Giga Bubble by AsmilDocumento3 pagineBusiness Plan Giga Bubble by AsmilAnonymous cu5JFkINessuna valutazione finora

- Homework: 1. Here Is A Definition of Marketing. Complete It Inserting The Following Verbs in The GapsDocumento12 pagineHomework: 1. Here Is A Definition of Marketing. Complete It Inserting The Following Verbs in The GapsMares TeodoraNessuna valutazione finora

- Economics Today The Macro View 19th Edition Miller Solutions ManualDocumento19 pagineEconomics Today The Macro View 19th Edition Miller Solutions Manualtusseh.itemm0lh100% (22)

- How To Buy and Sell StockDocumento9 pagineHow To Buy and Sell StockwaelNessuna valutazione finora

- Risk & Return: Risk of A Portfolio-Uncertainty Main View Two AspectsDocumento36 pagineRisk & Return: Risk of A Portfolio-Uncertainty Main View Two AspectsAminul Islam AmuNessuna valutazione finora

- The Impact of Online Recommendations and Consumer Feedback On SalesDocumento15 pagineThe Impact of Online Recommendations and Consumer Feedback On SalesashleysavetNessuna valutazione finora

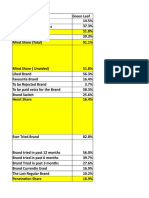

- Brand Health Analysis TemplateDocumento4 pagineBrand Health Analysis Templateanon_493704527Nessuna valutazione finora

- Limited Brands PresentationDocumento49 pagineLimited Brands PresentationIda ManNessuna valutazione finora