Potrebbero piacerti anche

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- O'gilvie Et Al., Minors v. United StatesDocumento1 paginaO'gilvie Et Al., Minors v. United StatesVel JuneNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5795)

- AaDocumento64 pagineAaFRIENDS CYBERCAFENessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Feldblum (Discounting Note)Documento8 pagineFeldblum (Discounting Note)Anna KrylovaNessuna valutazione finora

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Icici Lombard Health Care Insurance Claim FormDocumento5 pagineIcici Lombard Health Care Insurance Claim FormsperoNessuna valutazione finora

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Torts Case Digest Baliwag V CADocumento1 paginaTorts Case Digest Baliwag V CAKristine Joy TumbagaNessuna valutazione finora

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- Financial OrganiserDocumento4 pagineFinancial OrganiserAbhay MishraNessuna valutazione finora

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Marine InsuranceDocumento8 pagineMarine InsuranceSandeep Kumar BNessuna valutazione finora

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Guide For Veterans - Indian ArmyDocumento95 pagineGuide For Veterans - Indian Armypitchi100% (2)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

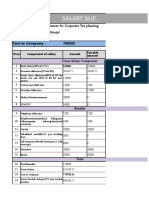

- Salary Slip: Submitted As Part of Assignment For Corporate Tax Planning Student Name: Vaibhav Gunjal Roll No: P81117Documento5 pagineSalary Slip: Submitted As Part of Assignment For Corporate Tax Planning Student Name: Vaibhav Gunjal Roll No: P81117D'quorNessuna valutazione finora

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Brief Scope of Work:: Greenesol Power Services PVT Ltd.,/Boiler/ENQ/SanghiDocumento8 pagineBrief Scope of Work:: Greenesol Power Services PVT Ltd.,/Boiler/ENQ/SanghiJKKNessuna valutazione finora

- Consumer Behaviour200813 0Documento36 pagineConsumer Behaviour200813 0monuNessuna valutazione finora

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- Form 1583Documento2 pagineForm 1583LukmanNessuna valutazione finora

- AckoPolicy-DBTR00006902247 00Documento1 paginaAckoPolicy-DBTR00006902247 00VijayaNessuna valutazione finora

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Historic Returns - Multi Cap Fund, Multi Cap Fund Performance Tracker Mutual Funds With Highest ReturnsDocumento3 pagineHistoric Returns - Multi Cap Fund, Multi Cap Fund Performance Tracker Mutual Funds With Highest Returnsakash bangaNessuna valutazione finora

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Solvency II - Introductory GuideDocumento12 pagineSolvency II - Introductory Guiderushdi36Nessuna valutazione finora

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Pfizer Pharmaceutical London United Kingdom Employment Agreement-Suresh.k.mDocumento5 paginePfizer Pharmaceutical London United Kingdom Employment Agreement-Suresh.k.mDeepanshu Gupta100% (1)

- Pension QuestionaireDocumento8 paginePension Questionaireharam moNessuna valutazione finora

- Care (Health Insurance Product) - BrochureDocumento10 pagineCare (Health Insurance Product) - Brochuresanjay4u4allNessuna valutazione finora

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- Chapter 5 Receivables and SalesDocumento80 pagineChapter 5 Receivables and SalesCecil MillerNessuna valutazione finora

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Contract For Artist and Gallery AgreementDocumento7 pagineContract For Artist and Gallery AgreementMirelaStefanNessuna valutazione finora

- FIN 580 - MidtermDocumento4 pagineFIN 580 - Midtermumair098Nessuna valutazione finora

- p2 Revision PackDocumento233 paginep2 Revision PackRana Hasan RahmanNessuna valutazione finora

- Rejda Rmi Ppt05 PBDocumento31 pagineRejda Rmi Ppt05 PBraygains23Nessuna valutazione finora

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Updated List of Insurance Entities in Good Standing As at November 20, 2020Documento5 pagineUpdated List of Insurance Entities in Good Standing As at November 20, 2020Fuaad DodooNessuna valutazione finora

- Loksabhaquestions Annex 1711 AS363Documento2 pagineLoksabhaquestions Annex 1711 AS363kishor saladiNessuna valutazione finora

- Settlement of Claim and Payment of MoneyDocumento9 pagineSettlement of Claim and Payment of MoneyVarnika TayaNessuna valutazione finora

- Tenant Land LordDocumento68 pagineTenant Land LordloweloweNessuna valutazione finora

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Time Fuze, by Gordon Randall Garrett 1Documento10 pagineTime Fuze, by Gordon Randall Garrett 1Valentina IonelaNessuna valutazione finora

- AbhinavDocumento3 pagineAbhinavpraveen kumarNessuna valutazione finora

- Structure of Production Cost in FootwearDocumento28 pagineStructure of Production Cost in FootwearSagar Raj Giri100% (1)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)