Potrebbero piacerti anche

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- An Overview of Islamic Banking-MergedDocumento335 pagineAn Overview of Islamic Banking-MergedThineshNessuna valutazione finora

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Shariah Governance Framework-MergedDocumento125 pagineShariah Governance Framework-MergedThineshNessuna valutazione finora

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- 9 Operational Risk - IdentificationDocumento13 pagine9 Operational Risk - IdentificationThineshNessuna valutazione finora

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (894)

- Maybank Annual Report 2019 - Corporate (English)Documento129 pagineMaybank Annual Report 2019 - Corporate (English)Gopal AggarwalNessuna valutazione finora

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- 8 Operational Risk Fundamentals and FrameworkDocumento10 pagine8 Operational Risk Fundamentals and FrameworkThineshNessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- 7 Market Risk - Mitigation and Regulatory RequirementsDocumento20 pagine7 Market Risk - Mitigation and Regulatory RequirementsThineshNessuna valutazione finora

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- 12 Model LimitationsDocumento6 pagine12 Model LimitationsThineshNessuna valutazione finora

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Islamic Retail Banking: Sources of FundsDocumento106 pagineIslamic Retail Banking: Sources of FundsThineshNessuna valutazione finora

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- Final Exam 1 - 7 January 2022Documento4 pagineFinal Exam 1 - 7 January 2022ThineshNessuna valutazione finora

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- Global FinanceDocumento25 pagineGlobal FinanceThineshNessuna valutazione finora

- Global FinanceDocumento25 pagineGlobal FinanceThineshNessuna valutazione finora

- Report ContentDocumento18 pagineReport ContentYou Wei WongNessuna valutazione finora

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Solution Manual For Financial Statements Analysis Subramanyam Wild 11th EditionDocumento48 pagineSolution Manual For Financial Statements Analysis Subramanyam Wild 11th EditionKatrinaYoungqtoki100% (83)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- Custom DutyDocumento40 pagineCustom DutyVijayasarathi VenugopalNessuna valutazione finora

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Documents Used in Transaction ProcessDocumento11 pagineDocuments Used in Transaction ProcessmbeosameerNessuna valutazione finora

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Institutions and Regional Integration in AfricaDocumento24 pagineInstitutions and Regional Integration in AfricaOrnela FabaniNessuna valutazione finora

- TITAN-MERCH-JOURNALDocumento2 pagineTITAN-MERCH-JOURNALElsa MendozaNessuna valutazione finora

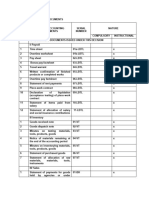

- List of Accounting DocumentsDocumento3 pagineList of Accounting DocumentsKhánh HuyềnNessuna valutazione finora

- NF902 Stock StatementDocumento5 pagineNF902 Stock Statementthangavel.fpclNessuna valutazione finora

- Materi Accounting AdvancedDocumento12 pagineMateri Accounting AdvancedRianty AstaniaNessuna valutazione finora

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- VN CB Vietnam Consumer Retail 2019Documento32 pagineVN CB Vietnam Consumer Retail 2019Huy Võ QuangNessuna valutazione finora

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- Oxford IB Diploma Programme IB Economics Course Book (JOCELYN. DORTON BLINK (IAN.), Ian Dorton)Documento601 pagineOxford IB Diploma Programme IB Economics Course Book (JOCELYN. DORTON BLINK (IAN.), Ian Dorton)sophieperervinNessuna valutazione finora

- I CT Block TypesDocumento12 pagineI CT Block TypesDedi NurhadiNessuna valutazione finora

- FIN102-Chapter 5 - Understanding CreditDocumento31 pagineFIN102-Chapter 5 - Understanding CreditmartinmuebejayiNessuna valutazione finora

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- A Study On Impact of GST On The Prices in Odisha: Samira PatraDocumento14 pagineA Study On Impact of GST On The Prices in Odisha: Samira PatraBiplab SwainNessuna valutazione finora

- ECO Exam IMP Questions (March-23) HM Hasnan PDFDocumento54 pagineECO Exam IMP Questions (March-23) HM Hasnan PDFMuhammad ZubairNessuna valutazione finora

- Esther Joy Velthoen - 2002 - (Thesis Doctor of Philosophy) Contested Coastlines Colonial Expansion Eastern Sulawesi 1680 1905Documento358 pagineEsther Joy Velthoen - 2002 - (Thesis Doctor of Philosophy) Contested Coastlines Colonial Expansion Eastern Sulawesi 1680 1905Rizaldi MaadjiNessuna valutazione finora

- Chapter 2 Why Do Cities ExistDocumento6 pagineChapter 2 Why Do Cities ExistMoayed Mohamed100% (2)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Aberdeen Budget For Fiscal Year 2022-2023Documento66 pagineAberdeen Budget For Fiscal Year 2022-2023Jaymie BaxleyNessuna valutazione finora

- Vat Math 2021Documento83 pagineVat Math 2021Fakharuddin Ahmed ShahNessuna valutazione finora

- Fair Trade in IndiaDocumento13 pagineFair Trade in IndiaLekshmy Surendran100% (1)

- Gloablisation Free Trade WorksheetDocumento1 paginaGloablisation Free Trade Worksheetapi-308477337Nessuna valutazione finora

- MOTSHEWA MABEL MOKHACHANE - eiFALwr4 - ArchivedDocumento2 pagineMOTSHEWA MABEL MOKHACHANE - eiFALwr4 - Archivedmabelblack02Nessuna valutazione finora

- L-NU AA-23-02-01-18 Finals Exam ReviewDocumento10 pagineL-NU AA-23-02-01-18 Finals Exam ReviewAmie Jane MirandaNessuna valutazione finora

- Entrep Chapter 6, 4MSDocumento15 pagineEntrep Chapter 6, 4MSJacel GadonNessuna valutazione finora

- Accounting for Merchandising Businesses Inventory SystemsDocumento15 pagineAccounting for Merchandising Businesses Inventory SystemsAple Balisi100% (1)

- Proforma: Port To Port or Combined Transport Bill of LadingDocumento2 pagineProforma: Port To Port or Combined Transport Bill of LadingRandy Idris SafatullahNessuna valutazione finora

- Sourcing and Costing of Apparel ProductsDocumento9 pagineSourcing and Costing of Apparel ProductsVaisistha BalNessuna valutazione finora

- International Trade TheoryDocumento53 pagineInternational Trade TheoryFaraz SiddiquiNessuna valutazione finora

- Acct Statement - XX0310 - 30012023Documento13 pagineAcct Statement - XX0310 - 30012023IRSHAD SHAN KNessuna valutazione finora

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Cad JpyDocumento7 pagineCad Jpyhung tranNessuna valutazione finora