Potrebbero piacerti anche

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Financial Statements, Cash Flow and TaxesDocumento44 pagineFinancial Statements, Cash Flow and TaxesAli JumaniNessuna valutazione finora

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- 11 Foreign Currency Transactionsxx PDFDocumento111 pagine11 Foreign Currency Transactionsxx PDFAnjell Reyes71% (17)

- REG-04 108d871Documento54 pagineREG-04 108d871Vidyadhar TRNessuna valutazione finora

- 14 Consolidated FS Pt1 PDFDocumento2 pagine14 Consolidated FS Pt1 PDFRiselle Ann Sanchez53% (15)

- Audit of PpeDocumento35 pagineAudit of Ppelordaiztrand50% (2)

- Test Bank Aa Part 2 2015 EdDocumento143 pagineTest Bank Aa Part 2 2015 EdNyang Santos72% (25)

- Shipping Industry Almanac 2014 (EY)Documento476 pagineShipping Industry Almanac 2014 (EY)Far CeurNessuna valutazione finora

- Session 2 - Deductions From Gross Income, Part 1Documento10 pagineSession 2 - Deductions From Gross Income, Part 1ABBIE GRACE DELA CRUZNessuna valutazione finora

- Acc Der HedgeDocumento78 pagineAcc Der HedgeEnrique Paolo Mendoza73% (11)

- Accounting For Business Combinations First Grading ExaminationDocumento18 pagineAccounting For Business Combinations First Grading Examinationjoyce77% (13)

- Post Test Regular Income Taxation For PartnershipsDocumento6 paginePost Test Regular Income Taxation For Partnershipslena cpaNessuna valutazione finora

- Post Test Regular Income Taxation For PartnershipsDocumento6 paginePost Test Regular Income Taxation For Partnershipslena cpaNessuna valutazione finora

- Vergara, Gian Bianca F. BSAT-4A Recitation: Compensation IncomeDocumento3 pagineVergara, Gian Bianca F. BSAT-4A Recitation: Compensation Incomelena cpa100% (2)

- TAXATION Finals ReviewerDocumento38 pagineTAXATION Finals ReviewerJunivenReyUmadhay100% (1)

- Business Tax IntroductionDocumento5 pagineBusiness Tax IntroductionJessica MalijanNessuna valutazione finora

- Solution: A. Gross Business Income, PhilippinesDocumento9 pagineSolution: A. Gross Business Income, Philippineslena cpa78% (9)

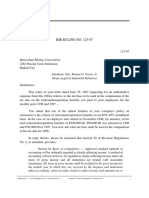

- ECONOMIC BENEFIT THEORY - BIR Ruling No. 123-97 (Retirement and Separation Benefits Paid To Employees)Documento2 pagineECONOMIC BENEFIT THEORY - BIR Ruling No. 123-97 (Retirement and Separation Benefits Paid To Employees)KriszanFrancoManiponNessuna valutazione finora

- Tax Rev Digest Mindanao II Geothermal Partnership V CirDocumento4 pagineTax Rev Digest Mindanao II Geothermal Partnership V CirCalypso75% (4)

- ANSWERS Post Test Regular Income Taxation For PartnershipsDocumento8 pagineANSWERS Post Test Regular Income Taxation For Partnershipslena cpa100% (1)

- Vergara, Gian Bianca F. BSAT-4A Recitation: Compensation IncomeDocumento4 pagineVergara, Gian Bianca F. BSAT-4A Recitation: Compensation Incomelena cpaNessuna valutazione finora

- 1.1.1 Quiz 1 - Answer KeyDocumento5 pagine1.1.1 Quiz 1 - Answer KeyMark Emil BaritNessuna valutazione finora

- CIR vs. Placer DomeDocumento4 pagineCIR vs. Placer DomeAngelo Castillo100% (1)

- BIR Ruling 555-12Documento4 pagineBIR Ruling 555-12Rebecca ChanNessuna valutazione finora

- Chapter 12Documento22 pagineChapter 12lena cpaNessuna valutazione finora

- CHP 23Documento19 pagineCHP 23lena cpaNessuna valutazione finora

- Post-Test L1 Introduction To Internal AuditingDocumento6 paginePost-Test L1 Introduction To Internal Auditinglena cpaNessuna valutazione finora

- JACEN-CODocumento27 pagineJACEN-COlena cpaNessuna valutazione finora

- Powerpoint Presentation Slide Contents For The ECE Thesis Proposal Defense 2019Documento2 paginePowerpoint Presentation Slide Contents For The ECE Thesis Proposal Defense 2019lena cpaNessuna valutazione finora

- Formatting A Document: Prepared By: Ma. Elaine M. RegaladoDocumento36 pagineFormatting A Document: Prepared By: Ma. Elaine M. Regaladolena cpaNessuna valutazione finora

- Research Proposal DraftDocumento6 pagineResearch Proposal Draftlena cpaNessuna valutazione finora

- Article IJJMC 122 PDFDocumento7 pagineArticle IJJMC 122 PDFjovie cornitaNessuna valutazione finora

- Quiz 6 Accounting For MaterialsDocumento2 pagineQuiz 6 Accounting For MaterialsVanessa AbellaNessuna valutazione finora

- Microsoft Word Basics: Prepared By: Ma. Elaine M. RegaladoDocumento23 pagineMicrosoft Word Basics: Prepared By: Ma. Elaine M. Regaladolena cpaNessuna valutazione finora

- Formatting A Document: Prepared By: Ma. Elaine M. RegaladoDocumento36 pagineFormatting A Document: Prepared By: Ma. Elaine M. Regaladolena cpaNessuna valutazione finora

- Microsoft Word Basics: Prepared By: Ma. Elaine M. RegaladoDocumento23 pagineMicrosoft Word Basics: Prepared By: Ma. Elaine M. Regaladolena cpaNessuna valutazione finora

- Why Do People Form GroupsDocumento2 pagineWhy Do People Form GroupsAphze Bautista Vlog50% (4)

- Quiz 11 Joint Product and by ProductDocumento1 paginaQuiz 11 Joint Product and by Productlena cpaNessuna valutazione finora

- Income Taxation 2015 Edition Solman PDFDocumento53 pagineIncome Taxation 2015 Edition Solman PDFPrincess AlqueroNessuna valutazione finora

- May GraphDocumento10 pagineMay Graphlena cpaNessuna valutazione finora

- Process Costing Solution To QuizDocumento19 pagineProcess Costing Solution To Quizlena cpaNessuna valutazione finora

- Certain To Happen, Though The Time of Happening Be UncertainDocumento1 paginaCertain To Happen, Though The Time of Happening Be Uncertainlena cpaNessuna valutazione finora

- Liddell and Co. vs. CIRDocumento7 pagineLiddell and Co. vs. CIRJohn Mark ReyesNessuna valutazione finora

- International Tax United Kingdom Highlights 2022: Updated January 2022Documento13 pagineInternational Tax United Kingdom Highlights 2022: Updated January 2022Paulo PatrãoNessuna valutazione finora

- Features of Philippine Income Tax SystemDocumento9 pagineFeatures of Philippine Income Tax SystemPATRICIA ANGELICA VINUYANessuna valutazione finora

- Chapter 1 - Succession & Transfer Taxes: Solutions Manual Transfer & Business Taxation, 2018 Edition By: Tabag & GarciaDocumento49 pagineChapter 1 - Succession & Transfer Taxes: Solutions Manual Transfer & Business Taxation, 2018 Edition By: Tabag & GarciaLanceNessuna valutazione finora

- Request For Taxpayer Identification Number and CertificationDocumento4 pagineRequest For Taxpayer Identification Number and CertificationZak CascaNessuna valutazione finora

- TAX QsDocumento131 pagineTAX QsUser 010897020197Nessuna valutazione finora

- Ra 11534 - Corporate Recovery & Tax Incentives For Enterprises Act (Create) Prepared By: Dr. Virginia Jeannie P. Lim Salient Changes Introduced AreDocumento9 pagineRa 11534 - Corporate Recovery & Tax Incentives For Enterprises Act (Create) Prepared By: Dr. Virginia Jeannie P. Lim Salient Changes Introduced AreAlicia Jane NavarroNessuna valutazione finora

- BIR Ruling (DA-456-99) - All Others' Per FCDU ITR Subject To GRTDocumento6 pagineBIR Ruling (DA-456-99) - All Others' Per FCDU ITR Subject To GRTCkey ArNessuna valutazione finora

- Additional Questions in FR (Ed 5 To Ed 6)Documento67 pagineAdditional Questions in FR (Ed 5 To Ed 6)shivam kukrejaNessuna valutazione finora

- Deduction PDFDocumento207 pagineDeduction PDFdeepluthra6Nessuna valutazione finora

- Foreign Retirement Plans Forms 3520 Forms 3520-A and Rev. Proc. 2020-17Documento14 pagineForeign Retirement Plans Forms 3520 Forms 3520-A and Rev. Proc. 2020-17e1chin0Nessuna valutazione finora

- Chapter 1: General Principles in Taxation: Aranea, 98 Phil. 148)Documento12 pagineChapter 1: General Principles in Taxation: Aranea, 98 Phil. 148)Rover RossNessuna valutazione finora

- Tax1 Final Landmark Case DigestDocumento29 pagineTax1 Final Landmark Case DigestasterNessuna valutazione finora

- Northern Cpa Review: Taxation Regular Income Taxation: Deductions From Gross IncomeDocumento16 pagineNorthern Cpa Review: Taxation Regular Income Taxation: Deductions From Gross IncomePauline EchanoNessuna valutazione finora

- GR 175410Documento28 pagineGR 175410Eins BalagtasNessuna valutazione finora

- Tax Notes Aban CabanDocumento3 pagineTax Notes Aban CabanWuwu WuswewuNessuna valutazione finora

- Documentation - AR RedesignDocumento9 pagineDocumentation - AR RedesignIrina CastroNessuna valutazione finora

- Answer: D : Statement 1: Uniformity Rule Is Not Violated When Different Articles Are Taxed at DifferentDocumento3 pagineAnswer: D : Statement 1: Uniformity Rule Is Not Violated When Different Articles Are Taxed at DifferentROSEMARIE CRUZNessuna valutazione finora

- ESSO Standard Eastern Inc Vs CIRDocumento6 pagineESSO Standard Eastern Inc Vs CIRToya MochizukieNessuna valutazione finora