Potrebbero piacerti anche

- Created By: Susan JonesDocumento246 pagineCreated By: Susan JonesdanitzavgNessuna valutazione finora

- Master Books ListDocumento32 pagineMaster Books ListfhaskellNessuna valutazione finora

- Thermal Physics Questions IB Question BankDocumento43 pagineThermal Physics Questions IB Question BankIBBhuvi Jain100% (1)

- Practical Earned Value Analysis: 25 Project Indicators from 5 MeasurementsDa EverandPractical Earned Value Analysis: 25 Project Indicators from 5 MeasurementsNessuna valutazione finora

- Sample Questions - Accounting For OverheadDocumento4 pagineSample Questions - Accounting For OverheadRedNessuna valutazione finora

- Tax1 (T31920)Documento82 pagineTax1 (T31920)Charles TuazonNessuna valutazione finora

- Process and Job Order Costing - EditedDocumento6 pagineProcess and Job Order Costing - EditedJasper Andrew AdjaraniNessuna valutazione finora

- Engineering and Commercial Functions in BusinessDa EverandEngineering and Commercial Functions in BusinessValutazione: 5 su 5 stelle5/5 (1)

- Isolated Flyback Switching Regulator W - 9V OutputDocumento16 pagineIsolated Flyback Switching Regulator W - 9V OutputCasey DialNessuna valutazione finora

- Process Costing Part 2 IllustrationsDocumento3 pagineProcess Costing Part 2 IllustrationsNCTNessuna valutazione finora

- Strategic Risk ManagementDocumento46 pagineStrategic Risk ManagementNuman Rox100% (1)

- Tutorial 3 - Process CostingDocumento5 pagineTutorial 3 - Process Costingsouayeh wejdenNessuna valutazione finora

- Pa2.M-1403 Process CostingDocumento16 paginePa2.M-1403 Process CostingJeric Israel0% (3)

- Belbis Vs PeopleDocumento1 paginaBelbis Vs Peoplekatherine magbanuaNessuna valutazione finora

- (Computation of Fifo and Wa Eups Case-To-Case) : B.C.VillaluzDocumento2 pagine(Computation of Fifo and Wa Eups Case-To-Case) : B.C.VillaluzBob Ghian ToveraNessuna valutazione finora

- Chap 04 Linear RegressionDocumento99 pagineChap 04 Linear RegressionCharles TuazonNessuna valutazione finora

- CCA LVL 3 Simex QAsDocumento14 pagineCCA LVL 3 Simex QAsRob De CastroNessuna valutazione finora

- Quiz Process Costing CompleteDocumento4 pagineQuiz Process Costing CompleteVea Abegail GarciaNessuna valutazione finora

- Uneven Application of CostsDocumento2 pagineUneven Application of CostsMeghan Kaye LiwenNessuna valutazione finora

- A7 Quiz 3Documento26 pagineA7 Quiz 3Garcia Alizsandra L.Nessuna valutazione finora

- 8 Process CostingDocumento4 pagine8 Process CostingMaria Cristina A. BarrionNessuna valutazione finora

- 2311 Acct6131039 Lhfa TK1-W3-S4-R2 Team8Documento8 pagine2311 Acct6131039 Lhfa TK1-W3-S4-R2 Team8Nadilla NurNessuna valutazione finora

- Process Costing - Sample Problems PDFDocumento3 pagineProcess Costing - Sample Problems PDFalyssa100% (1)

- Process Costing Quiz 2Documento5 pagineProcess Costing Quiz 2Joann CaneteNessuna valutazione finora

- Multiple Choices - TheoreticalDocumento8 pagineMultiple Choices - TheoreticalIsabelle AmbataliNessuna valutazione finora

- Creating a One-Piece Flow and Production Cell: Just-in-time Production with Toyota’s Single Piece FlowDa EverandCreating a One-Piece Flow and Production Cell: Just-in-time Production with Toyota’s Single Piece FlowValutazione: 4 su 5 stelle4/5 (1)

- Process CostingDocumento4 pagineProcess CostingAndrea Nicole MASANGKAY100% (1)

- Process Costing Pa MoreDocumento3 pagineProcess Costing Pa MoreAlle NadroNessuna valutazione finora

- Afar ProcessDocumento2 pagineAfar ProcessRyan Julius RullanNessuna valutazione finora

- DocDocumento8 pagineDocJAY AUBREY PINEDANessuna valutazione finora

- 09 Process CostingDocumento3 pagine09 Process Costing202010461Nessuna valutazione finora

- Take Home Quiz Chapters 7 9Documento5 pagineTake Home Quiz Chapters 7 9Hillarie Albano RarangolNessuna valutazione finora

- Semifinal CostDocumento6 pagineSemifinal CostALMA MORENANessuna valutazione finora

- Process Costing - Equivalent Units IIDocumento8 pagineProcess Costing - Equivalent Units IIaishabadarNessuna valutazione finora

- Sbu Process Costing HandoutsDocumento4 pagineSbu Process Costing HandoutsAngel Alejo AcobaNessuna valutazione finora

- Process Costing Wave QuizzerDocumento3 pagineProcess Costing Wave QuizzerBarbi KyuNessuna valutazione finora

- Michael John C. Ode, CPA: AfarDocumento3 pagineMichael John C. Ode, CPA: AfarYojec RollonNessuna valutazione finora

- Process-Costing Self-Study-Activity With AnswersDocumento9 pagineProcess-Costing Self-Study-Activity With AnswersDane PerezNessuna valutazione finora

- Case 1. Landers CompanyDocumento3 pagineCase 1. Landers CompanyMavel DesamparadoNessuna valutazione finora

- Process Costing SWDocumento2 pagineProcess Costing SWChristine AltamarinoNessuna valutazione finora

- Activity 1 MAS1 AnswersDocumento2 pagineActivity 1 MAS1 Answersangel mae cuevasNessuna valutazione finora

- Process Costing Set B QuestionDocumento4 pagineProcess Costing Set B QuestionTrixie HicaldeNessuna valutazione finora

- Quiz #2 Cost AccountingDocumento6 pagineQuiz #2 Cost AccountingLica CiprianoNessuna valutazione finora

- Chapter # 4 Exercise & Problems - NewDocumento5 pagineChapter # 4 Exercise & Problems - NewZia UddinNessuna valutazione finora

- Process Costing Part 2.1Documento3 pagineProcess Costing Part 2.1Francis Matthew JimenezNessuna valutazione finora

- CPAR PA2 0405 Final PreboardDocumento11 pagineCPAR PA2 0405 Final PreboardErika BucaoNessuna valutazione finora

- Cost Accounting ProblemsDocumento9 pagineCost Accounting ProblemsLia AtilanoNessuna valutazione finora

- ACCTG 201 Illustrative ProblemsDocumento4 pagineACCTG 201 Illustrative ProblemsJewel Anne RentumaNessuna valutazione finora

- Advance Financial Accounting and Reporting Padj/Rf: Process Costing A. ProblemsDocumento4 pagineAdvance Financial Accounting and Reporting Padj/Rf: Process Costing A. ProblemsRoxell CaibogNessuna valutazione finora

- ProbbbDocumento19 pagineProbbbacidoleannamaeNessuna valutazione finora

- Chapter 4 ExercisesDocumento8 pagineChapter 4 ExercisesLy VõNessuna valutazione finora

- ACTIVITY 7 - Process CostingDocumento2 pagineACTIVITY 7 - Process CostingMarga TorresNessuna valutazione finora

- Topic 6 Process Costing: Figure 8-1 Product and Cost Flow in Job Order and Process CostingDocumento11 pagineTopic 6 Process Costing: Figure 8-1 Product and Cost Flow in Job Order and Process CostingChristian Jay-r Abrasaldo BalcitaNessuna valutazione finora

- Assigment Sample ProblemsDocumento5 pagineAssigment Sample ProblemsRamainne RonquilloNessuna valutazione finora

- Chapter V: Process Cost Accounting - General ProceduresDocumento3 pagineChapter V: Process Cost Accounting - General ProceduresSweet Jenesie MirandaNessuna valutazione finora

- ProcessDocumento11 pagineProcessElaine YapNessuna valutazione finora

- AP 1402 CashDocumento13 pagineAP 1402 CashElaine YapNessuna valutazione finora

- Exercises - Process CostingDocumento3 pagineExercises - Process CostingJazzyNessuna valutazione finora

- Process Costing Exercises Series 1Documento23 pagineProcess Costing Exercises Series 1sarahbeeNessuna valutazione finora

- Process CostingDocumento2 pagineProcess CostingwhosccccNessuna valutazione finora

- QUIZZERDocumento4 pagineQUIZZERchowchow123Nessuna valutazione finora

- Kế toán quản trị ngày 9 - 5Documento6 pagineKế toán quản trị ngày 9 - 5Ly BùiNessuna valutazione finora

- Long QuizDocumento4 pagineLong QuizJoshua Rey Sapuras0% (1)

- Process Costing FIFO ER PDFDocumento13 pagineProcess Costing FIFO ER PDFJason CariñoNessuna valutazione finora

- Accounting Principles 8th Edition - Exercises Chapter21Documento7 pagineAccounting Principles 8th Edition - Exercises Chapter21bulealiyi71Nessuna valutazione finora

- 1.1 Overview of International BusinessDocumento27 pagine1.1 Overview of International BusinessCharles TuazonNessuna valutazione finora

- Content ServerDocumento26 pagineContent ServerCharles TuazonNessuna valutazione finora

- Dela Cruz - Cloud Computing-1Documento4 pagineDela Cruz - Cloud Computing-1Charles TuazonNessuna valutazione finora

- 1.2 Factors Impacting International Business OperationsDocumento37 pagine1.2 Factors Impacting International Business OperationsCharles TuazonNessuna valutazione finora

- Updated Annual Per Capita Poverty Threshold Poverty Incidence and Magnitude of Poor FamiDocumento32 pagineUpdated Annual Per Capita Poverty Threshold Poverty Incidence and Magnitude of Poor FamiCharles TuazonNessuna valutazione finora

- Student-Reports and OpinionDocumento44 pagineStudent-Reports and OpinionCharles TuazonNessuna valutazione finora

- PDF h02 Pre TestDocumento8 paginePDF h02 Pre TestCharles TuazonNessuna valutazione finora

- HW On INVESTMENT PROPERTY - 1Documento2 pagineHW On INVESTMENT PROPERTY - 1Charles TuazonNessuna valutazione finora

- Business Report TopicsDocumento4 pagineBusiness Report TopicsCharles TuazonNessuna valutazione finora

- 28S32 High Acres LF 2017.2018-03-01.ARDocumento144 pagine28S32 High Acres LF 2017.2018-03-01.ARCharles TuazonNessuna valutazione finora

- IAASB Main Agenda (September 2004) Page 2004 1949: Prepared By: Alta Prinsloo (August 2004)Documento22 pagineIAASB Main Agenda (September 2004) Page 2004 1949: Prepared By: Alta Prinsloo (August 2004)Charles TuazonNessuna valutazione finora

- AFI Infographics - SignedDocumento1 paginaAFI Infographics - SignedCharles TuazonNessuna valutazione finora

- (Final) 11072018 CNPF 17Q Ytd Nine Months 2018Documento59 pagine(Final) 11072018 CNPF 17Q Ytd Nine Months 2018Charles TuazonNessuna valutazione finora

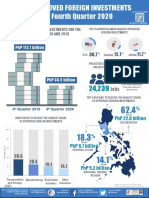

- AFI Infographics - Q4 2020 - SignedDocumento1 paginaAFI Infographics - Q4 2020 - SignedCharles TuazonNessuna valutazione finora

- Q3 WRKSHT Perpetual PDFDocumento1 paginaQ3 WRKSHT Perpetual PDFCharles TuazonNessuna valutazione finora

- MT Set A PDFDocumento6 pagineMT Set A PDFCharles TuazonNessuna valutazione finora

- Q1 Set B PDFDocumento5 pagineQ1 Set B PDFCharles TuazonNessuna valutazione finora

- Gratittude Manufacturing Company Post-Closing Trial Balance DECEMBER 31, 2017Documento3 pagineGratittude Manufacturing Company Post-Closing Trial Balance DECEMBER 31, 2017Charles TuazonNessuna valutazione finora

- Partnership Liquidation: Steps Involved in LiquidationDocumento13 paginePartnership Liquidation: Steps Involved in LiquidationCharles TuazonNessuna valutazione finora

- Sample Problem SolvingDocumento2 pagineSample Problem SolvingCharles TuazonNessuna valutazione finora

- LQ2 Set B PDFDocumento5 pagineLQ2 Set B PDFCharles TuazonNessuna valutazione finora

- Sentence Connectors: 1.contrast 1. A. Direct OppositionDocumento8 pagineSentence Connectors: 1.contrast 1. A. Direct OppositionCathy siganNessuna valutazione finora

- Lesson Plan MP-2Documento7 pagineLesson Plan MP-2VeereshGodiNessuna valutazione finora

- Site Master S113C, S114C, S331C, S332C, Antenna, Cable and Spectrum AnalyzerDocumento95 pagineSite Master S113C, S114C, S331C, S332C, Antenna, Cable and Spectrum AnalyzerKodhamagulla SudheerNessuna valutazione finora

- DigoxinDocumento18 pagineDigoxinApril Mergelle LapuzNessuna valutazione finora

- Google Automatically Generates HTML Versions of Documents As We Crawl The WebDocumento2 pagineGoogle Automatically Generates HTML Versions of Documents As We Crawl The Websuchi ravaliaNessuna valutazione finora

- Delaware Met CSAC Initial Meeting ReportDocumento20 pagineDelaware Met CSAC Initial Meeting ReportKevinOhlandtNessuna valutazione finora

- 2022 Drik Panchang Hindu FestivalsDocumento11 pagine2022 Drik Panchang Hindu FestivalsBikash KumarNessuna valutazione finora

- Spelling Master 1Documento1 paginaSpelling Master 1CristinaNessuna valutazione finora

- Arctic Beacon Forbidden Library - Winkler-The - Thousand - Year - Conspiracy PDFDocumento196 pagineArctic Beacon Forbidden Library - Winkler-The - Thousand - Year - Conspiracy PDFJames JohnsonNessuna valutazione finora

- Physics - TRIAL S1, STPM 2022 - CoverDocumento1 paginaPhysics - TRIAL S1, STPM 2022 - CoverbenNessuna valutazione finora

- CV Michael Naughton 2019Documento2 pagineCV Michael Naughton 2019api-380850234Nessuna valutazione finora

- An Analysis of The PoemDocumento2 pagineAn Analysis of The PoemDayanand Gowda Kr100% (2)

- English Lesson Plan 6 AugustDocumento10 pagineEnglish Lesson Plan 6 AugustKhairunnisa FazilNessuna valutazione finora

- Far Eastern University-Institute of Nursing In-House NursingDocumento25 pagineFar Eastern University-Institute of Nursing In-House Nursingjonasdelacruz1111Nessuna valutazione finora

- Crime Scene Manual FullDocumento19 pagineCrime Scene Manual FullMuhammed MUZZAMMILNessuna valutazione finora

- Speech by His Excellency The Governor of Vihiga County (Rev) Moses Akaranga During The Closing Ceremony of The Induction Course For The Sub-County and Ward Administrators.Documento3 pagineSpeech by His Excellency The Governor of Vihiga County (Rev) Moses Akaranga During The Closing Ceremony of The Induction Course For The Sub-County and Ward Administrators.Moses AkarangaNessuna valutazione finora

- Quadrotor UAV For Wind Profile Characterization: Moyano Cano, JavierDocumento85 pagineQuadrotor UAV For Wind Profile Characterization: Moyano Cano, JavierJuan SebastianNessuna valutazione finora

- Chapter 019Documento28 pagineChapter 019Esteban Tabares GonzalezNessuna valutazione finora

- Sayyid Jamal Al-Din Muhammad B. Safdar Al-Afghani (1838-1897)Documento8 pagineSayyid Jamal Al-Din Muhammad B. Safdar Al-Afghani (1838-1897)Itslee NxNessuna valutazione finora

- Ergonomics For The BlindDocumento8 pagineErgonomics For The BlindShruthi PandulaNessuna valutazione finora

- Mathematics Grade 5 Quarter 2: Answer KeyDocumento4 pagineMathematics Grade 5 Quarter 2: Answer KeyApril Jean Cahoy100% (2)

- Accomplishment Report: For Service Credits (Availment/claim) Election May 2019Documento1 paginaAccomplishment Report: For Service Credits (Availment/claim) Election May 2019Glazy Kim Seco - JorquiaNessuna valutazione finora

- MOA Agri BaseDocumento6 pagineMOA Agri BaseRodj Eli Mikael Viernes-IncognitoNessuna valutazione finora

- Bab 3 - Soal-Soal No. 4 SD 10Documento4 pagineBab 3 - Soal-Soal No. 4 SD 10Vanni LimNessuna valutazione finora