Potrebbero piacerti anche

- Module 01 Fundamrental Principles of TaxationDocumento21 pagineModule 01 Fundamrental Principles of TaxationDonna Mae FernandezNessuna valutazione finora

- Double TaxationDocumento4 pagineDouble TaxationLou Nonoi TanNessuna valutazione finora

- Chapter 1 Introduction To Taxation: Chapter Overview and ObjectivesDocumento30 pagineChapter 1 Introduction To Taxation: Chapter Overview and ObjectivesNoeme LansangNessuna valutazione finora

- Quiz On Fringe Benefit Tax and Dealings in Properties (ACOBA 2TAY2021 BBINCTAX)Documento7 pagineQuiz On Fringe Benefit Tax and Dealings in Properties (ACOBA 2TAY2021 BBINCTAX)Nicole Daphne FigueroaNessuna valutazione finora

- Income Tax On CorporationDocumento53 pagineIncome Tax On CorporationLyka Mae Palarca IrangNessuna valutazione finora

- General Principles and Concepts of TaxationDocumento10 pagineGeneral Principles and Concepts of TaxationNekki Mae Guinto Dela CernaNessuna valutazione finora

- Classification of TaxesDocumento16 pagineClassification of TaxesJo-Al Gealon100% (1)

- Lecture Notes VII Theories On Government SpendingDocumento6 pagineLecture Notes VII Theories On Government SpendingrichelNessuna valutazione finora

- TaxationDocumento23 pagineTaxationMark Angelo S. Enriquez50% (4)

- Module 1 & 2: at The End of This Topic, We Should Be Able To Learn The FollowingDocumento33 pagineModule 1 & 2: at The End of This Topic, We Should Be Able To Learn The FollowingAlicia FelicianoNessuna valutazione finora

- Module 02 - Taxes, Laws, Systems and AdministrationDocumento22 pagineModule 02 - Taxes, Laws, Systems and AdministrationElla Marie Lopez0% (1)

- Basic Principles of A Sound Tax SystemDocumento6 pagineBasic Principles of A Sound Tax SystemhppddlNessuna valutazione finora

- Income Taxes For CorporationsDocumento35 pagineIncome Taxes For CorporationsKurt SoriaoNessuna valutazione finora

- Prefinals Exam in Income TaxationDocumento3 paginePrefinals Exam in Income TaxationYen YenNessuna valutazione finora

- Gross Income: Module No. 3-4 Inclusive Week: August 23-27, 2021 Module Overview Reference / Research LinksDocumento13 pagineGross Income: Module No. 3-4 Inclusive Week: August 23-27, 2021 Module Overview Reference / Research LinksHeigh Ven100% (1)

- Taxes, Tax Laws, and Tax AdministrationDocumento8 pagineTaxes, Tax Laws, and Tax AdministrationAilene MendozaNessuna valutazione finora

- 801 Value Added TaxDocumento4 pagine801 Value Added TaxHarold Cedric Noleal OsorioNessuna valutazione finora

- Public ExpenditureDocumento6 paginePublic ExpenditureNaruChoudhary0% (1)

- Readingd in Philippine History Fabro, Lesly Ann A. DEC. 15, 2020Documento3 pagineReadingd in Philippine History Fabro, Lesly Ann A. DEC. 15, 2020Agyao Yam Faith100% (1)

- GROUP 10 (Corporation Income Taxation - Regular Corporation)Documento16 pagineGROUP 10 (Corporation Income Taxation - Regular Corporation)Denmark David Gaspar NatanNessuna valutazione finora

- Art. 6 Sec. 28 Limitation On The Power of Taxation - Uniform and EquitableDocumento2 pagineArt. 6 Sec. 28 Limitation On The Power of Taxation - Uniform and EquitableMadeliniaNessuna valutazione finora

- Income TaxationDocumento38 pagineIncome TaxationElson TalotaloNessuna valutazione finora

- Chapter 5 Final Income TaxationDocumento26 pagineChapter 5 Final Income TaxationJason MablesNessuna valutazione finora

- Deductions On Gross IncomeDocumento34 pagineDeductions On Gross IncomeKathlyn PostreNessuna valutazione finora

- History, Concepts, & Principles of TaxationDocumento52 pagineHistory, Concepts, & Principles of TaxationBianca GalindoNessuna valutazione finora

- Business and Transfer Taxation: TO Consumption TaxesDocumento40 pagineBusiness and Transfer Taxation: TO Consumption TaxesKC GutierrezNessuna valutazione finora

- Taxation - Day 01Documento2 pagineTaxation - Day 01Joyce Sherly Ann LuceroNessuna valutazione finora

- Income Taxation by NickAduana (Answer Key)Documento113 pagineIncome Taxation by NickAduana (Answer Key)Samantha Andrea Grefaldia100% (2)

- Polytechnic University of The PhilippinesDocumento60 paginePolytechnic University of The PhilippinesJoseph TrajanoNessuna valutazione finora

- What Is Community Tax?: Speaker: Valerie A. OngDocumento25 pagineWhat Is Community Tax?: Speaker: Valerie A. Ongmarz busaNessuna valutazione finora

- Interest Rates and Their Role in FinanceDocumento17 pagineInterest Rates and Their Role in FinanceClyden Jaile RamirezNessuna valutazione finora

- 3 Income Taxation Final PDFDocumento109 pagine3 Income Taxation Final PDFwilliam0910900% (1)

- Incom Taxation 21 Chapter 3Documento33 pagineIncom Taxation 21 Chapter 3Charl RegenciaNessuna valutazione finora

- Allowable Deductions (Income Taxation) ReviewerDocumento59 pagineAllowable Deductions (Income Taxation) ReviewerAB CloydNessuna valutazione finora

- TaxDocumento22 pagineTaxalphecca_adolfo25Nessuna valutazione finora

- Module 08 Exclusions From Gross Income 2Documento14 pagineModule 08 Exclusions From Gross Income 2Joshua BazarNessuna valutazione finora

- CHAPTER 2 Taxation LawDocumento13 pagineCHAPTER 2 Taxation LawDonna Marie Baluyut100% (1)

- Review Related LiteratureDocumento5 pagineReview Related Literaturejeff60% (5)

- MC1 Income TaxationDocumento5 pagineMC1 Income Taxationjohn carlo tolentinoNessuna valutazione finora

- TaxationDocumento9 pagineTaxationEnitsuj Eam EugarbalNessuna valutazione finora

- Memorandum Train LawDocumento23 pagineMemorandum Train LawKweeng Tayrus FaelnarNessuna valutazione finora

- Business Taxation NotesDocumento2 pagineBusiness Taxation NotesSelene DimlaNessuna valutazione finora

- TX10 Other Percentage TaxDocumento16 pagineTX10 Other Percentage TaxAnna AldaveNessuna valutazione finora

- General Principles of Taxation - Sample CasesDocumento2 pagineGeneral Principles of Taxation - Sample CasesJace Tanaya100% (1)

- Tax1 Prelim Summer 17Documento5 pagineTax1 Prelim Summer 17Sheena CalderonNessuna valutazione finora

- DYBSATax213 - Income Taxation (MODULE 1-14)Documento51 pagineDYBSATax213 - Income Taxation (MODULE 1-14)MARK ANGELO PANGILINANNessuna valutazione finora

- IFRS 9 Financial Instruments - F7Documento39 pagineIFRS 9 Financial Instruments - F7TD2 from Henry HarvinNessuna valutazione finora

- The Regular Corporate Income TaxDocumento4 pagineThe Regular Corporate Income TaxReniel Renz AterradoNessuna valutazione finora

- 68125672575bdf96fc857f403531f1c9-copyDocumento9 pagine68125672575bdf96fc857f403531f1c9-copyyour unreal0% (1)

- Discussion QuestionsDocumento7 pagineDiscussion QuestionsPoison IvyNessuna valutazione finora

- Chapter 6Documento3 pagineChapter 6Marichris AlbuferaNessuna valutazione finora

- Case Study: Gma'S Gozon, Inquirer'S Prieto Slapped With P23-M Tax CaseDocumento6 pagineCase Study: Gma'S Gozon, Inquirer'S Prieto Slapped With P23-M Tax CaseJilliana JacyNessuna valutazione finora

- Intermediate Accounting 3 - Week 1 - Module 2Documento6 pagineIntermediate Accounting 3 - Week 1 - Module 2LuisitoNessuna valutazione finora

- Tax 1 Valencia Solman For Chap 2Documento12 pagineTax 1 Valencia Solman For Chap 2Yeovil Pansacala100% (1)

- Govt Acctg Ch1 Intro of NgasDocumento63 pagineGovt Acctg Ch1 Intro of NgasRachel Sanculi Lustina86% (7)

- Module 01 Fundamrental Principles of Taxation RevisedDocumento21 pagineModule 01 Fundamrental Principles of Taxation RevisedSly BlueNessuna valutazione finora

- Taxation ReviewerDocumento143 pagineTaxation ReviewerChristine Joy V. AlascoNessuna valutazione finora

- Module 01 - General Principles of TaxationDocumento19 pagineModule 01 - General Principles of TaxationblueplaneskiesNessuna valutazione finora

- WarrantyDocumento26 pagineWarrantySumit KumarNessuna valutazione finora

- Paul Laurence C. Dela RosaDocumento2 paginePaul Laurence C. Dela RosaDarius DelacruzNessuna valutazione finora

- HXC-FB80: Three 2/3-Inch Exmor ™ CMOS Sensor HD Colour Studio CameraDocumento10 pagineHXC-FB80: Three 2/3-Inch Exmor ™ CMOS Sensor HD Colour Studio CameraDarius DelacruzNessuna valutazione finora

- Call: + (603) 7890 2880: Starter Enterprise AdvancedDocumento1 paginaCall: + (603) 7890 2880: Starter Enterprise AdvancedTitan KNessuna valutazione finora

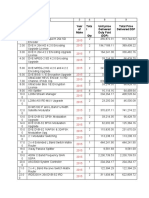

- Year of Make Tota L Qty Unit Price Delivered Duty Paid (DDP) Total Price Delivered DDPDocumento2 pagineYear of Make Tota L Qty Unit Price Delivered Duty Paid (DDP) Total Price Delivered DDPDarius DelacruzNessuna valutazione finora

- Camcorder 4KDocumento108 pagineCamcorder 4KDarius DelacruzNessuna valutazione finora

- Matrix of Changes - CleanDocumento111 pagineMatrix of Changes - CleanJonnel AcobaNessuna valutazione finora

- Module 8 - Budgeting Theories: Basic ConceptsDocumento17 pagineModule 8 - Budgeting Theories: Basic ConceptsPolinar Paul MarbenNessuna valutazione finora

- October 27 - Special DeductionsDocumento3 pagineOctober 27 - Special DeductionsDarius DelacruzNessuna valutazione finora

- BADVAC1X - MOD 6 TemplatesDocumento16 pagineBADVAC1X - MOD 6 TemplatesDarius DelacruzNessuna valutazione finora

- 3 PDFDocumento4 pagine3 PDFDarius DelacruzNessuna valutazione finora

- BADVAC1X - Quiz 2 Finals: (1 Point)Documento9 pagineBADVAC1X - Quiz 2 Finals: (1 Point)Darius DelacruzNessuna valutazione finora

- 2.4 Exercises - Job Oder Costing - Straight Problems (NEW) 1Documento3 pagine2.4 Exercises - Job Oder Costing - Straight Problems (NEW) 1Darius Delacruz50% (2)

- Chapter 07 - Intercompany Inventory TransactionsDocumento38 pagineChapter 07 - Intercompany Inventory Transactions_casals100% (8)

- Year of SaleDocumento12 pagineYear of SaleDarius DelacruzNessuna valutazione finora

- The Country Project: International BusinessDocumento3 pagineThe Country Project: International BusinessDarius DelacruzNessuna valutazione finora

- 08 X07 B Responsibility Accounting and TP Transfer PricingDocumento8 pagine08 X07 B Responsibility Accounting and TP Transfer PricingJericho Pedragosa100% (1)

- CONCLUSIONDocumento2 pagineCONCLUSIONDarius DelacruzNessuna valutazione finora

- Accounting 7 Instructions: Choose The Most Correct Answer For Each of The Following Questions. Write The Letter of YourDocumento43 pagineAccounting 7 Instructions: Choose The Most Correct Answer For Each of The Following Questions. Write The Letter of YourIzzy B100% (2)

- 0619F TM2 Apr2020 PDFDocumento1 pagina0619F TM2 Apr2020 PDFDarius DelacruzNessuna valutazione finora

- Population DensityDocumento4 paginePopulation DensityDarius DelacruzNessuna valutazione finora

- Vii - TechnologicalDocumento1 paginaVii - TechnologicalDarius DelacruzNessuna valutazione finora

- November 6 - CorporationsDocumento2 pagineNovember 6 - CorporationsDarius DelacruzNessuna valutazione finora

- Final Tax Rates Notes: General CoverageDocumento3 pagineFinal Tax Rates Notes: General CoverageDarius DelacruzNessuna valutazione finora

- Abe Post QualDocumento3 pagineAbe Post QualDarius DelacruzNessuna valutazione finora

- 0619F TM2 Apr2020 PDFDocumento1 pagina0619F TM2 Apr2020 PDFDarius DelacruzNessuna valutazione finora

- Monthly Remittance Return of Final Income Taxes Withheld: Kawanihan NG Rentas InternasDocumento2 pagineMonthly Remittance Return of Final Income Taxes Withheld: Kawanihan NG Rentas InternasAlfred BryanNessuna valutazione finora

- 0619F TM2 Apr2020 PDFDocumento1 pagina0619F TM2 Apr2020 PDFDarius DelacruzNessuna valutazione finora

- Franchise Accounting Problem IDocumento1 paginaFranchise Accounting Problem IDarius DelacruzNessuna valutazione finora

- Complaint Form: Kilusang Kooperatiba NG PTV (PTVKO)Documento6 pagineComplaint Form: Kilusang Kooperatiba NG PTV (PTVKO)Darius DelacruzNessuna valutazione finora

- Questions Multiplier Model With KeyDocumento2 pagineQuestions Multiplier Model With Keyaditi shukla100% (1)

- LPC With KeziahDocumento240 pagineLPC With KeziahkeziahNessuna valutazione finora

- 5.) People V MarraDocumento2 pagine5.) People V MarraMarcusNessuna valutazione finora

- TIBAG Dec PDFDocumento48 pagineTIBAG Dec PDFAngelika CalingasanNessuna valutazione finora

- Countries in TransitionDocumento7 pagineCountries in TransitionshackeristNessuna valutazione finora

- Declaration of Scott L. Glabe, Deputy General Counsel For The House Permanent Select Committee On IntelligenceDocumento16 pagineDeclaration of Scott L. Glabe, Deputy General Counsel For The House Permanent Select Committee On IntelligenceN.S.100% (1)

- POINTERS TO REVIEW Philo With AnswersDocumento4 paginePOINTERS TO REVIEW Philo With AnswersGreg BarrogaNessuna valutazione finora

- AUPE - Government Employees and WagesDocumento2 pagineAUPE - Government Employees and WagesEmily MertzNessuna valutazione finora

- NSTP100 Essay #10Documento1 paginaNSTP100 Essay #10Hungry Versatile GamerNessuna valutazione finora

- The Development of Good Governance Model For Performance ImprovementDocumento17 pagineThe Development of Good Governance Model For Performance Improvementarga baswaraNessuna valutazione finora

- Essay On Population ExplosionDocumento16 pagineEssay On Population ExplosionManik ChoudharyNessuna valutazione finora

- Commentary On The HPCR ManualDocumento354 pagineCommentary On The HPCR ManualAshish GautamNessuna valutazione finora

- 1 Lo Cham v. OcampoDocumento2 pagine1 Lo Cham v. OcampoZepht Badilla100% (2)

- MHADA INFORMATION BOOKLET ENGLISH Chap-7Documento4 pagineMHADA INFORMATION BOOKLET ENGLISH Chap-7Joint Chief Officer, MB MHADANessuna valutazione finora

- Display PDFDocumento5 pagineDisplay PDFPrateek ManjulNessuna valutazione finora

- Is The Appointment of Barangay Official and Constitutional?Documento4 pagineIs The Appointment of Barangay Official and Constitutional?Christian Jeru De GuzmanNessuna valutazione finora

- Political Science PojectDocumento16 paginePolitical Science PojectAmogha KonammeNessuna valutazione finora

- Compiled TranscriptDocumento38 pagineCompiled TranscriptTelle MarieNessuna valutazione finora

- JPRS ReportDocumento70 pagineJPRS ReportSintherNessuna valutazione finora

- Art 253. Coverage and Employees' Right To Self-OrganizationDocumento14 pagineArt 253. Coverage and Employees' Right To Self-OrganizationcattaczNessuna valutazione finora

- Eleanor Roosevelt EssayDocumento5 pagineEleanor Roosevelt EssayilovecstNessuna valutazione finora

- IN RE: VICTORIO D. LANUEVO (A.M. No. 1162 August 29, 1975)Documento16 pagineIN RE: VICTORIO D. LANUEVO (A.M. No. 1162 August 29, 1975)Donato Vergara IIINessuna valutazione finora

- A1.4 - UcspDocumento2 pagineA1.4 - UcspGrenlee KhenNessuna valutazione finora

- Dharmashastra National Law University, Jabalpur (M.P.)Documento3 pagineDharmashastra National Law University, Jabalpur (M.P.)Raman PatelNessuna valutazione finora

- Lacson vs. Perez DigestDocumento2 pagineLacson vs. Perez DigestNiq Polido80% (5)

- Pale Canon 5Documento41 paginePale Canon 5Nemei SantiagoNessuna valutazione finora

- La Influencia Del Sueño Americano en La Inmigracion LatinaDocumento64 pagineLa Influencia Del Sueño Americano en La Inmigracion Latinaalejandra_ferreiro_2Nessuna valutazione finora

- Race & EthnicDocumento5 pagineRace & EthnicVethashri NarasingamNessuna valutazione finora

- The Knife and The Message The Roots of The New Palestinian UprisingDocumento80 pagineThe Knife and The Message The Roots of The New Palestinian UprisingJerusalem Center for Public AffairsNessuna valutazione finora

- PTI History & Ideology. (Downloaded With 1stbrowser)Documento7 paginePTI History & Ideology. (Downloaded With 1stbrowser)Ayesha KhanNessuna valutazione finora