Potrebbero piacerti anche

- Business Laws Amendment Act 2021Documento15 pagineBusiness Laws Amendment Act 2021Cyrus KNessuna valutazione finora

- The Central Goods and Services Tax (Amendment) BILL, 2018Documento26 pagineThe Central Goods and Services Tax (Amendment) BILL, 2018Mystic MysteryNessuna valutazione finora

- Inland Revenue (Amendment) Bill PublishedDocumento40 pagineInland Revenue (Amendment) Bill PublishedDarshana Sanjeewa100% (1)

- Piltdtml: @0egu, TdeDocumento4 paginePiltdtml: @0egu, TdeNawabNessuna valutazione finora

- CGST Amendment Act 2018Documento9 pagineCGST Amendment Act 2018sridharanNessuna valutazione finora

- BILL - The Written Laws (Financial Provisions) (Amendment) Act, 2022 - MD, MendezDocumento9 pagineBILL - The Written Laws (Financial Provisions) (Amendment) Act, 2022 - MD, MendezLucas MaduhuNessuna valutazione finora

- FINANCE ACT, No. 35 OF 2018Documento24 pagineFINANCE ACT, No. 35 OF 2018janithbogahawattaNessuna valutazione finora

- Vatactno7 (E) 2003Documento19 pagineVatactno7 (E) 2003jing qiangNessuna valutazione finora

- Le Road Traffic (Amendment) Act 2018Documento43 pagineLe Road Traffic (Amendment) Act 2018L'express Maurice100% (2)

- Act 20 of 2020Documento8 pagineAct 20 of 2020Kriti KumarNessuna valutazione finora

- VATActNo15 (E) 2008Documento12 pagineVATActNo15 (E) 2008jing qiangNessuna valutazione finora

- Finance Bill, 16 June 2022Documento73 pagineFinance Bill, 16 June 2022grayson moshiNessuna valutazione finora

- FIN - BILL - 2019 MalaysiaDocumento36 pagineFIN - BILL - 2019 MalaysiaTedNessuna valutazione finora

- Finance Bill 2011Documento23 pagineFinance Bill 2011sherafghan_97Nessuna valutazione finora

- Public Procurement and Disposal of Public Assets (Amendment) ActDocumento28 paginePublic Procurement and Disposal of Public Assets (Amendment) Actiam ianneNessuna valutazione finora

- Tax 4Documento3 pagineTax 4JK Lights TradingNessuna valutazione finora

- 2020 AmendmentsDocumento5 pagine2020 AmendmentsAAKASH BATRANessuna valutazione finora

- FinanceBill 2011Documento39 pagineFinanceBill 2011Shawkat ZafarNessuna valutazione finora

- Finance Act (No. 2) (No. 10 of 2020)Documento40 pagineFinance Act (No. 2) (No. 10 of 2020)Christina TambalaNessuna valutazione finora

- The Public Benefits (Amendment) Bill, 2014Documento33 pagineThe Public Benefits (Amendment) Bill, 2014HonMosesKuriaNessuna valutazione finora

- Graham-Cassidy Obamacare Replacement PlanDocumento140 pagineGraham-Cassidy Obamacare Replacement PlanSarahNessuna valutazione finora

- The Income Tax Amendment Act 10 2017Documento8 pagineThe Income Tax Amendment Act 10 2017Nyeko FrancisNessuna valutazione finora

- Act Supplement No. 6 22 February, 2019: The United Republic of TanzaniaDocumento11 pagineAct Supplement No. 6 22 February, 2019: The United Republic of TanzaniaFrancisco Hagai GeorgeNessuna valutazione finora

- Income Tax (Amendment) Bill, 2023Documento14 pagineIncome Tax (Amendment) Bill, 2023Frank WadidiNessuna valutazione finora

- ValueAddedTaxAmendmentAct2022 PDFDocumento17 pagineValueAddedTaxAmendmentAct2022 PDFDesmar WhitfieldNessuna valutazione finora

- Finance (Supplementary) Act, 2023Documento9 pagineFinance (Supplementary) Act, 2023Umair NeoronNessuna valutazione finora

- Act 39 of 2021Documento9 pagineAct 39 of 2021Kriti KumarNessuna valutazione finora

- Changes in GST LawDocumento31 pagineChanges in GST LawSUNIL PUJARINessuna valutazione finora

- Act 32 of 2023Documento12 pagineAct 32 of 2023Kriti KumarNessuna valutazione finora

- DR 12 - 2022 - BiDocumento22 pagineDR 12 - 2022 - BiDevan MollyNessuna valutazione finora

- A Bill: 111 Congress 2 SDocumento3 pagineA Bill: 111 Congress 2 Sapi-25909546Nessuna valutazione finora

- Act No. 5 of 2022 The Finance Act 2022 Act No. 5 of 2022Documento48 pagineAct No. 5 of 2022 The Finance Act 2022 Act No. 5 of 2022Mathias MhinaNessuna valutazione finora

- Finance Act 2015v1Documento42 pagineFinance Act 2015v1Anonymous 3RNEd6CK3Nessuna valutazione finora

- Finance Act - No. 8 of 2020Documento17 pagineFinance Act - No. 8 of 2020Jos NyangletNessuna valutazione finora

- Finance Bill Punjab 2020Documento12 pagineFinance Bill Punjab 2020muddassirayazNessuna valutazione finora

- AKTA 831 - BI - WJW015xxx BIDocumento42 pagineAKTA 831 - BI - WJW015xxx BIWei LinNessuna valutazione finora

- Finance Act 2009Documento66 pagineFinance Act 2009Antony Paul OregeNessuna valutazione finora

- Malaysia Amendments To Income Tax Act 1967Documento52 pagineMalaysia Amendments To Income Tax Act 1967Abd MuisNessuna valutazione finora

- The Finance Act, 2017Documento33 pagineThe Finance Act, 2017Simo WifkaouiNessuna valutazione finora

- P F M A: Ublic Inance Anagement MendmentDocumento24 pagineP F M A: Ublic Inance Anagement MendmentJoshua TamaraNessuna valutazione finora

- Insolvency Amendment Regulations 2017 PDFDocumento34 pagineInsolvency Amendment Regulations 2017 PDFJoy SitatiNessuna valutazione finora

- Act A1651 Employment (Amendment) Act 2022Documento21 pagineAct A1651 Employment (Amendment) Act 2022fahiraNessuna valutazione finora

- Finance Bill 2014Documento75 pagineFinance Bill 2014Irfan KhanNessuna valutazione finora

- Legal Aspects GSTDocumento46 pagineLegal Aspects GSTtharani1771_32442248Nessuna valutazione finora

- Taxation Laws (A) Bill, 2016Documento9 pagineTaxation Laws (A) Bill, 2016p6a4nduNessuna valutazione finora

- Description: Tags: s152Documento3 pagineDescription: Tags: s152anon-109600Nessuna valutazione finora

- (B18-2019) (Taxation Laws)Documento56 pagine(B18-2019) (Taxation Laws)Khayakazi NtondiniNessuna valutazione finora

- Insolvency Ammendment Act-No-16-Of-2022-1669884315Documento12 pagineInsolvency Ammendment Act-No-16-Of-2022-1669884315Moses KayimaNessuna valutazione finora

- ANTIGUA and BARBUDA Law Miscellaneous Amendments Bill 2018-PVDocumento10 pagineANTIGUA and BARBUDA Law Miscellaneous Amendments Bill 2018-PVOw EmanNessuna valutazione finora

- The Sindh Government GazetteDocumento8 pagineThe Sindh Government GazettepakistanhrfNessuna valutazione finora

- Service-Turnover-Tax-Repeal 2020Documento3 pagineService-Turnover-Tax-Repeal 2020vaishnaviNessuna valutazione finora

- The Income Tax (Amendment) Act, 2018Documento13 pagineThe Income Tax (Amendment) Act, 2018mark1matthewsNessuna valutazione finora

- Finance Bill, 2024 E-GazetteDocumento27 pagineFinance Bill, 2024 E-GazettecaakhileshvashishthaNessuna valutazione finora

- Act 13 of 2023 Finance Act 2024 FinalDocumento62 pagineAct 13 of 2023 Finance Act 2024 FinaladdyNessuna valutazione finora

- Finance Act 2022Documento43 pagineFinance Act 2022Mark GechureNessuna valutazione finora

- Health Care Freedom ActDocumento8 pagineHealth Care Freedom ActAnonymous 2lblWUW6rSNessuna valutazione finora

- Policies and Investments to Address Climate Change and Air Quality in the Beijing–Tianjin–Hebei RegionDa EverandPolicies and Investments to Address Climate Change and Air Quality in the Beijing–Tianjin–Hebei RegionNessuna valutazione finora

- Protocol For The Prevention of The Crime of Genocide War Crimes and Crimes Against Humanity and All Forms of DiscriminationDocumento15 pagineProtocol For The Prevention of The Crime of Genocide War Crimes and Crimes Against Humanity and All Forms of DiscriminationwalalrNessuna valutazione finora

- Coram: Maraga, CJ &P, Ibrahim, Wanjala, Njoki & Lenaola, SCJJDocumento42 pagineCoram: Maraga, CJ &P, Ibrahim, Wanjala, Njoki & Lenaola, SCJJwalalrNessuna valutazione finora

- Kenya Gazette Supplement: 20 Jul Zoib IaDocumento20 pagineKenya Gazette Supplement: 20 Jul Zoib IawalalrNessuna valutazione finora

- Kenya Gazette Supplement: ACTS, 2020Documento6 pagineKenya Gazette Supplement: ACTS, 2020walalrNessuna valutazione finora

- National Assembly: Official ReportDocumento51 pagineNational Assembly: Official ReportwalalrNessuna valutazione finora

- Foreign Service Bill 2018 South AfricaDocumento12 pagineForeign Service Bill 2018 South AfricawalalrNessuna valutazione finora

- The Traffic ActDocumento232 pagineThe Traffic ActtmakauNessuna valutazione finora

- Sample Minutes of Stock Approval by BoardDocumento2 pagineSample Minutes of Stock Approval by BoardwalalrNessuna valutazione finora

- Sample Mandate LetterDocumento10 pagineSample Mandate Letterwalalr86% (21)

- Danny SyDocumento2 pagineDanny SyJael AmorNessuna valutazione finora

- 6352 Pract Exam Part 1Documento5 pagine6352 Pract Exam Part 1iluvumiNessuna valutazione finora

- Harsiddhi To HPDocumento6 pagineHarsiddhi To HPME-B AMAN SHAIKHNessuna valutazione finora

- QESCO BILL NewDocumento1 paginaQESCO BILL NewBilal AhmedNessuna valutazione finora

- Unit Cost Analysis.2019Documento1 paginaUnit Cost Analysis.2019Edwin Tapit JrNessuna valutazione finora

- 134 Maddiralasaiushasree Salary 2021-07Documento1 pagina134 Maddiralasaiushasree Salary 2021-07SAI USHA SREE MADDIRALANessuna valutazione finora

- Gel Cash FlowDocumento3 pagineGel Cash Flowravibhartia1978Nessuna valutazione finora

- MbhjbsDocumento1 paginaMbhjbskjdguysgsgNessuna valutazione finora

- Dazn InvoiceDocumento2 pagineDazn InvoicesergsxrNessuna valutazione finora

- Allied Engineering & Services (PVT.) LTDDocumento2 pagineAllied Engineering & Services (PVT.) LTDmuhammad omerNessuna valutazione finora

- ADIT Syllabus 2016Documento68 pagineADIT Syllabus 2016Ali ZafaarNessuna valutazione finora

- Commissioner of Internal Revenue (CIR) Vs Algue Inc 158 SCRA 9Documento3 pagineCommissioner of Internal Revenue (CIR) Vs Algue Inc 158 SCRA 9Epictitus StoicNessuna valutazione finora

- PT. HPA Indonesia - HPAI Sales Integrated SystemDocumento1 paginaPT. HPA Indonesia - HPAI Sales Integrated SystemZul KhaidirNessuna valutazione finora

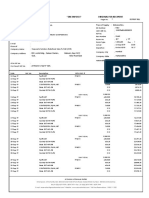

- No Article Code Article Decsription Article Group Qty Amount Qty Return Return Amount Qty Nett Amount NettoDocumento1 paginaNo Article Code Article Decsription Article Group Qty Amount Qty Return Return Amount Qty Nett Amount Nettomabaranjay1987Nessuna valutazione finora

- Lenovo Cashback Offer T&CsDocumento3 pagineLenovo Cashback Offer T&CsChiragNessuna valutazione finora

- Weekly Payment ProofDocumento34 pagineWeekly Payment ProofVIKASH KHICHARNessuna valutazione finora

- Nysboe Financial Disclosure Report - August 13Documento22 pagineNysboe Financial Disclosure Report - August 13Elizabeth BenjaminNessuna valutazione finora

- Income Taxation Banggawan - Chapter 1Documento5 pagineIncome Taxation Banggawan - Chapter 1Frances Garrovillas100% (13)

- Hotel BillDocumento3 pagineHotel BillAbbas FakhruddinNessuna valutazione finora

- Laporan Cash Flow ANTAM KomengDocumento2 pagineLaporan Cash Flow ANTAM KomengNiky SuryadiNessuna valutazione finora

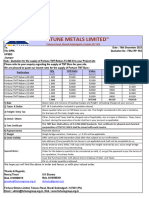

- "Fortune Metals Limited": Talwara Road, Mandi Gobindgarh, Punjab-147 301Documento1 pagina"Fortune Metals Limited": Talwara Road, Mandi Gobindgarh, Punjab-147 301S K SharmaNessuna valutazione finora

- Mutasi Livin Juli-JuniDocumento3 pagineMutasi Livin Juli-JuniAhmadFadzliNessuna valutazione finora

- 1-12 Inv-Gb-123115881-2023-14512 33.64Documento1 pagina1-12 Inv-Gb-123115881-2023-14512 33.64pravasunfilteredNessuna valutazione finora

- Cryptocurrency Advantages and DisadvantagesDocumento6 pagineCryptocurrency Advantages and DisadvantagesResearch Park100% (1)

- Tax Dabu Rev.-Notes-2022Documento32 pagineTax Dabu Rev.-Notes-2022april75Nessuna valutazione finora

- Transaction - Dispute - Written - Claim 2 PDFDocumento2 pagineTransaction - Dispute - Written - Claim 2 PDFSheila LiknessNessuna valutazione finora

- Proforma Invoice Kyocera Document Solutions India Pvt. LTD.Documento1 paginaProforma Invoice Kyocera Document Solutions India Pvt. LTD.Tushar patilNessuna valutazione finora

- DBM Compensation Policy Guidelines No. 98-1 (Page 1 of 2)Documento1 paginaDBM Compensation Policy Guidelines No. 98-1 (Page 1 of 2)Rej Francisco100% (1)

- Unit Wise Center Taxpayers ListDocumento8.526 pagineUnit Wise Center Taxpayers Listaman3327Nessuna valutazione finora

- TCS Configuration Reference DocumentDocumento34 pagineTCS Configuration Reference DocumentPrateek MohapatraNessuna valutazione finora