Potrebbero piacerti anche

- Taxation Law: Central Excise Tariff Act, 1985Documento8 pagineTaxation Law: Central Excise Tariff Act, 1985Amit GroverNessuna valutazione finora

- I Direct TaxDocumento155 pagineI Direct TaxRajnish ShastriNessuna valutazione finora

- The Central Excise ActDocumento6 pagineThe Central Excise ActMinu ScariaNessuna valutazione finora

- P 14Documento728 pagineP 14Moaaz Ahmed100% (1)

- 2018 Tariff NotesDocumento23 pagine2018 Tariff NotesYash SawantNessuna valutazione finora

- Central Excise Act Notes For Self PreparationDocumento29 pagineCentral Excise Act Notes For Self PreparationVivek ReddyNessuna valutazione finora

- Overview of Central ExciseDocumento31 pagineOverview of Central ExciseMadhuree PerumallaNessuna valutazione finora

- Types of Custom DutiesDocumento29 pagineTypes of Custom DutiesShikhar AgarwalNessuna valutazione finora

- 4 Applied Indirect TaxationDocumento316 pagine4 Applied Indirect TaxationSanjay VanjayNessuna valutazione finora

- Chapter 03Documento39 pagineChapter 03Ram SskNessuna valutazione finora

- Excise Note 1Documento2 pagineExcise Note 1Mayur UpasaniNessuna valutazione finora

- Central ExciseDocumento53 pagineCentral ExciseSuyash JainNessuna valutazione finora

- Central ExciseDocumento22 pagineCentral ExcisesadathnooriNessuna valutazione finora

- 21797vol3secaidtccp1 PDFDocumento14 pagine21797vol3secaidtccp1 PDFtimirkantaNessuna valutazione finora

- Central Excise DutyDocumento19 pagineCentral Excise DutyGurneet Kaur GujralNessuna valutazione finora

- Excise Duty: Central Excise Tariff Act, 1985Documento9 pagineExcise Duty: Central Excise Tariff Act, 1985Azhar KhanNessuna valutazione finora

- Central Excise Short NotesDocumento27 pagineCentral Excise Short Notestoprascal0% (1)

- Custom LawDocumento88 pagineCustom LawVijay KumarNessuna valutazione finora

- Basic Concepts: 1.1 Constitution of IndiaDocumento34 pagineBasic Concepts: 1.1 Constitution of IndiaJitendra VernekarNessuna valutazione finora

- Introduction To Customs DutyDocumento14 pagineIntroduction To Customs DutyKshitij BasavrajNessuna valutazione finora

- Salient Features of Exise ActDocumento7 pagineSalient Features of Exise ActYogesh Patil0% (1)

- Tally Erp 9.0 Material Excise For Manufacturers in Tally Erp 9.0Documento128 pagineTally Erp 9.0 Material Excise For Manufacturers in Tally Erp 9.0Raghavendra yadav KMNessuna valutazione finora

- Applied Indirect TaxationDocumento349 pagineApplied Indirect TaxationVijetha K Murthy100% (1)

- Basic Concepts of Excise TaxDocumento13 pagineBasic Concepts of Excise Taxk gowtham kumar100% (1)

- Draft Preventive Manual Vol IDocumento654 pagineDraft Preventive Manual Vol Ipooram001Nessuna valutazione finora

- Amendment CustomsDocumento50 pagineAmendment Customsamithamp20Nessuna valutazione finora

- Certificate Course in C.exciseDocumento180 pagineCertificate Course in C.exciseKrishna CheediNessuna valutazione finora

- Notes of Central ExciseDocumento27 pagineNotes of Central Excisesudhir joreegalaNessuna valutazione finora

- TAX LAW - Income From Other SourcesDocumento21 pagineTAX LAW - Income From Other SourcesFahim KhanNessuna valutazione finora

- Tax AssignmentDocumento20 pagineTax AssignmentAnamNessuna valutazione finora

- 9-Legal & Tax ASP of Busn Sem - IDocumento39 pagine9-Legal & Tax ASP of Busn Sem - Iindrajeet_sahaniNessuna valutazione finora

- Central Excise Notes 1Documento29 pagineCentral Excise Notes 1Sakshi SharmaNessuna valutazione finora

- Customs DutyDocumento8 pagineCustoms DutyBhavana GadagNessuna valutazione finora

- Indirect PDFDocumento56 pagineIndirect PDFdhikshaNessuna valutazione finora

- Faculty of Law: Jamia Millia IslamiaDocumento25 pagineFaculty of Law: Jamia Millia IslamiaShimran ZamanNessuna valutazione finora

- Direct TaxDocumento13 pagineDirect TaxRajveer Singh SekhonNessuna valutazione finora

- Central Excise ManualDocumento108 pagineCentral Excise ManualAnand PrakashNessuna valutazione finora

- Indirect Taxes: Excise, VAT and GSTDocumento19 pagineIndirect Taxes: Excise, VAT and GSTmanikaNessuna valutazione finora

- Central Excise Vizag08022021Documento35 pagineCentral Excise Vizag08022021do or dieNessuna valutazione finora

- Central Excise: 1. Levy of Excise DutyDocumento27 pagineCentral Excise: 1. Levy of Excise Dutyvrayapudi79Nessuna valutazione finora

- Export Import Procedures and DocumentationDocumento11 pagineExport Import Procedures and DocumentationTeena RawatNessuna valutazione finora

- 13 - Tax Law - Customs Law - 271219Documento25 pagine13 - Tax Law - Customs Law - 271219Sushil BansalNessuna valutazione finora

- Customs DutyDocumento8 pagineCustoms DutyRanvids100% (1)

- Central Excise Act 1944, Central Excise Rule 2002 and Goods and Sales Tax (GST)Documento42 pagineCentral Excise Act 1944, Central Excise Rule 2002 and Goods and Sales Tax (GST)kushal patilNessuna valutazione finora

- Indirect Tax NotesDocumento61 pagineIndirect Tax NotesSaksham KaushikNessuna valutazione finora

- The Central Excise ACT, 1944: Group MembersDocumento17 pagineThe Central Excise ACT, 1944: Group MembersSaddam HussainNessuna valutazione finora

- Central ExciseDocumento2 pagineCentral ExciseNawab SahabNessuna valutazione finora

- Selective Excise Tax EngDocumento24 pagineSelective Excise Tax Engrizzwan4uNessuna valutazione finora

- Peraturan Pemerintah Nomor - 49 TAHUN 2022 (ENGLISH)Documento57 paginePeraturan Pemerintah Nomor - 49 TAHUN 2022 (ENGLISH)Zahra Calista ArmansyahNessuna valutazione finora

- The Central Excise Act, 1944Documento10 pagineThe Central Excise Act, 1944sandeep1318100% (3)

- Central Excise: 1. Levy of Excise DutyDocumento18 pagineCentral Excise: 1. Levy of Excise Dutynivedita_h42404Nessuna valutazione finora

- Central Excise - A Guide To Assessees: Principles of Excise ControlDocumento8 pagineCentral Excise - A Guide To Assessees: Principles of Excise ControlKIshor SanapNessuna valutazione finora

- Nature of Excise DutyDocumento16 pagineNature of Excise DutyVinod PatelNessuna valutazione finora

- Central Excise ActDocumento19 pagineCentral Excise ActPoonam MehtaNessuna valutazione finora

- KNCCI Vihiga: enabling county revenue raising legislationDa EverandKNCCI Vihiga: enabling county revenue raising legislationNessuna valutazione finora

- KNCCI Vihiga: enabling county revenue raising legislationDa EverandKNCCI Vihiga: enabling county revenue raising legislationNessuna valutazione finora

- Cost Control and Cost ReductionDocumento10 pagineCost Control and Cost Reductiondileepsu100% (2)

- M 2Documento46 pagineM 2dileepsuNessuna valutazione finora

- M 2Documento46 pagineM 2dileepsuNessuna valutazione finora

- Module 1Documento52 pagineModule 1dileepsuNessuna valutazione finora

- Regional Integrations IBMDocumento64 pagineRegional Integrations IBMdileepsuNessuna valutazione finora

- Cost Control and Cost ReductionDocumento10 pagineCost Control and Cost Reductiondileepsu100% (2)

- Subject MappingDocumento2 pagineSubject MappingdileepsuNessuna valutazione finora

- Cost AccountingDocumento10 pagineCost AccountingdileepsuNessuna valutazione finora

- Income From SalariesDocumento14 pagineIncome From SalariesdileepsuNessuna valutazione finora

- Income From SalariesDocumento14 pagineIncome From SalariesdileepsuNessuna valutazione finora

- SyllabusDocumento1 paginaSyllabusdileepsuNessuna valutazione finora

- Rahul Bajaj ProfileDocumento1 paginaRahul Bajaj ProfiledileepsuNessuna valutazione finora

- Good Day Friends: Today's Topic: LeadershipDocumento41 pagineGood Day Friends: Today's Topic: LeadershipdileepsuNessuna valutazione finora

- ControllingDocumento20 pagineControllingdileepsuNessuna valutazione finora

- 1lect Chap1&2 090799Documento13 pagine1lect Chap1&2 090799dileepsuNessuna valutazione finora

- Income From SalariesDocumento14 pagineIncome From SalariesdileepsuNessuna valutazione finora

- Good Day Friends: Today's Topic: LeadershipDocumento29 pagineGood Day Friends: Today's Topic: LeadershipdileepsuNessuna valutazione finora

- Advertisement: My Topic: Impact of AdvertisingDocumento15 pagineAdvertisement: My Topic: Impact of AdvertisingDileepsudupiNessuna valutazione finora

- CH 2 3-9-2019 CompleteDocumento8 pagineCH 2 3-9-2019 CompleteAryan RawatNessuna valutazione finora

- Adobe Scan 01 Mar 2023Documento1 paginaAdobe Scan 01 Mar 2023Appu YNessuna valutazione finora

- Air Freight DocumentationDocumento17 pagineAir Freight DocumentationSubhashis ModakNessuna valutazione finora

- Dwnload Full International Economics 12th Edition Salvatore Solutions Manual PDFDocumento35 pagineDwnload Full International Economics 12th Edition Salvatore Solutions Manual PDFvolapukbubalevoju2100% (9)

- Business Finance12 Q3 M2Documento52 pagineBusiness Finance12 Q3 M2Chriztal TejadaNessuna valutazione finora

- Cash Management CaseDocumento10 pagineCash Management CaseKim CustodioNessuna valutazione finora

- Sample Cases 1-11 With SolutionsDocumento10 pagineSample Cases 1-11 With SolutionsJenina Rose SalvadorNessuna valutazione finora

- Angus Cartwright IV Case WriteupDocumento11 pagineAngus Cartwright IV Case Writeupapi-644958016Nessuna valutazione finora

- Lecture 4 - Evaluating Competition in RetailingDocumento39 pagineLecture 4 - Evaluating Competition in Retailingjefribasiuni1517Nessuna valutazione finora

- Life Line of National EconomyDocumento16 pagineLife Line of National EconomyxyzNessuna valutazione finora

- 5 Kyc Completed 26 April 2023Documento37 pagine5 Kyc Completed 26 April 2023sridhar sNessuna valutazione finora

- Booklet 2023 Indonesia UpdateDocumento50 pagineBooklet 2023 Indonesia UpdateJulius TariganNessuna valutazione finora

- Sejarah Singkat IKEADocumento7 pagineSejarah Singkat IKEAAris SaraunNessuna valutazione finora

- Final Asian Paints SCMDocumento25 pagineFinal Asian Paints SCMsanju0789Nessuna valutazione finora

- International Business Competing in The Global Marketplace 10Th Edition Hill Test Bank Full Chapter PDFDocumento68 pagineInternational Business Competing in The Global Marketplace 10Th Edition Hill Test Bank Full Chapter PDFamandatrangyxogy100% (10)

- API BX - Klt.dinv - CD.WD Ds2 en Excel v2 5872141Documento74 pagineAPI BX - Klt.dinv - CD.WD Ds2 en Excel v2 5872141Mihalciuc VladNessuna valutazione finora

- WEALTHIER Non-Monetary Article 15 Shashank PalDocumento2 pagineWEALTHIER Non-Monetary Article 15 Shashank PalShashank PalNessuna valutazione finora

- PDF cffm6 CH 17 TB 10 06 08 DDDocumento25 paginePDF cffm6 CH 17 TB 10 06 08 DDCaptain ObviousNessuna valutazione finora

- Sri Lankas Economic Crisis ABrief OverviewDocumento12 pagineSri Lankas Economic Crisis ABrief OverviewSadhika MathurNessuna valutazione finora

- Công TH CDocumento9 pagineCông TH CLê Hồng ThuỷNessuna valutazione finora

- World Trade Organisation: A Brief HistoryDocumento46 pagineWorld Trade Organisation: A Brief HistorysonalgargjaipurNessuna valutazione finora

- 02d - AVL For Seamless Line PipesDocumento1 pagina02d - AVL For Seamless Line Pipesraj dosNessuna valutazione finora

- List of Shopping Malls in IndiaDocumento14 pagineList of Shopping Malls in IndiaRaghavendra MishraNessuna valutazione finora

- Swimming Membership Receipt-MulundDocumento1 paginaSwimming Membership Receipt-Mulundchithur DevarajNessuna valutazione finora

- Basic Microeconomics REVIEWER - Theory of ProductionDocumento2 pagineBasic Microeconomics REVIEWER - Theory of ProductionJig PerfectoNessuna valutazione finora

- FINAL Sustainability Report 2017Documento90 pagineFINAL Sustainability Report 2017lucasNessuna valutazione finora

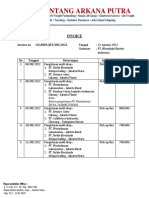

- Pt. Bintang Arkana Putra: InvoiceDocumento2 paginePt. Bintang Arkana Putra: InvoiceSlamet FarhannurdinNessuna valutazione finora

- Fan IndustryDocumento54 pagineFan Industryshani2767% (3)

- Banking Module 1Documento5 pagineBanking Module 1Bilal shujaatNessuna valutazione finora

- Chapter 1 - GST (30 Marks) Time: 1hr 15 MinDocumento2 pagineChapter 1 - GST (30 Marks) Time: 1hr 15 MinRohan MehtaNessuna valutazione finora