Potrebbero piacerti anche

- CN Jamesville Development AppealDocumento14 pagineCN Jamesville Development AppealThe Hamilton SpectatorNessuna valutazione finora

- Fire Marshal Report From Dundas Arson MurdersDocumento11 pagineFire Marshal Report From Dundas Arson MurdersThe Hamilton SpectatorNessuna valutazione finora

- Depth Chart For Ticats RosterDocumento2 pagineDepth Chart For Ticats RosterThe Hamilton SpectatorNessuna valutazione finora

- James Kopp Court FilingDocumento19 pagineJames Kopp Court FilingThe Hamilton SpectatorNessuna valutazione finora

- Judicial ReviewDocumento12 pagineJudicial ReviewThe Hamilton SpectatorNessuna valutazione finora

- Supercrawl Festival MapDocumento1 paginaSupercrawl Festival MapThe Hamilton SpectatorNessuna valutazione finora

- Lusitania LetterDocumento6 pagineLusitania LetterThe Hamilton SpectatorNessuna valutazione finora

- McMaster Denies Request To View PNB Legal FeesDocumento2 pagineMcMaster Denies Request To View PNB Legal FeesThe Hamilton SpectatorNessuna valutazione finora

- Eastgate SquareDocumento19 pagineEastgate SquareThe Hamilton SpectatorNessuna valutazione finora

- Regional Reform Survey QuestionsDocumento1 paginaRegional Reform Survey QuestionsThe Hamilton SpectatorNessuna valutazione finora

- Letter From Province About Hamilton Urban BoundaryDocumento16 pagineLetter From Province About Hamilton Urban BoundaryThe Hamilton SpectatorNessuna valutazione finora

- Scarsin Forecast: Scenario 1 - Worst CaseDocumento3 pagineScarsin Forecast: Scenario 1 - Worst CaseThe Hamilton SpectatorNessuna valutazione finora

- Email Sent To PNB Graduate StudentsDocumento2 pagineEmail Sent To PNB Graduate StudentsThe Hamilton SpectatorNessuna valutazione finora

- Road Value For Money AuditDocumento63 pagineRoad Value For Money AuditThe Hamilton SpectatorNessuna valutazione finora

- Tex Watson LetterDocumento1 paginaTex Watson LetterThe Hamilton SpectatorNessuna valutazione finora

- Hamilton Police Discipline Decision For Paul ManningDocumento60 pagineHamilton Police Discipline Decision For Paul ManningThe Hamilton SpectatorNessuna valutazione finora

- Marge Thielke LetterDocumento1 paginaMarge Thielke LetterThe Hamilton SpectatorNessuna valutazione finora

- Heritage Green Inspection Report - May 26Documento2 pagineHeritage Green Inspection Report - May 26The Hamilton SpectatorNessuna valutazione finora

- Clint Hill LetterDocumento1 paginaClint Hill LetterThe Hamilton SpectatorNessuna valutazione finora

- Hamilton Rapid Transit Benefits ReportDocumento119 pagineHamilton Rapid Transit Benefits ReportThe Hamilton SpectatorNessuna valutazione finora

- Stadium Precinct Preliminary DesignDocumento1 paginaStadium Precinct Preliminary DesignThe Hamilton SpectatorNessuna valutazione finora

- Section 22 Order National Steel CarDocumento3 pagineSection 22 Order National Steel CarThe Hamilton SpectatorNessuna valutazione finora

- Grace Villa Inspection Report: Dec 11, 2020Documento3 pagineGrace Villa Inspection Report: Dec 11, 2020The Hamilton SpectatorNessuna valutazione finora

- Grace Villa Ministry Inspection Report Dec 22, 2020Documento3 pagineGrace Villa Ministry Inspection Report Dec 22, 2020The Hamilton SpectatorNessuna valutazione finora

- Code of Conduct Complaint Against Councillor Sam MerullaDocumento30 pagineCode of Conduct Complaint Against Councillor Sam MerullaThe Hamilton SpectatorNessuna valutazione finora

- Victim Impact PoemDocumento2 pagineVictim Impact PoemThe Hamilton SpectatorNessuna valutazione finora

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Structure of Financial SystemDocumento14 pagineStructure of Financial SystemRegina LintuaNessuna valutazione finora

- NRI BankingDocumento33 pagineNRI BankingKrinal Shah0% (1)

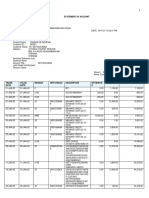

- Statement of AccountDocumento16 pagineStatement of AccountSriNessuna valutazione finora

- LECTURE NO 4 5Cs and 7Ps of CreditDocumento5 pagineLECTURE NO 4 5Cs and 7Ps of CreditJessica Miller79% (14)

- Mortgage Under Transfer of Property Act 1882Documento3 pagineMortgage Under Transfer of Property Act 188218212 NEELESH CHANDRANessuna valutazione finora

- Q#2 ACTFMKT 2021-2: Attempt HistoryDocumento6 pagineQ#2 ACTFMKT 2021-2: Attempt HistorymlaNessuna valutazione finora

- PSL35Documento2 paginePSL35musaismail8863Nessuna valutazione finora

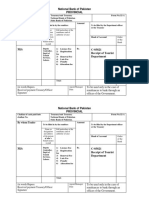

- Know Your CustomerDocumento3 pagineKnow Your CustomerMardi RahardjoNessuna valutazione finora

- BCF+1373521 BCF+1373521 BCF+1373521 BCF+1373521 BCF+1373521Documento1 paginaBCF+1373521 BCF+1373521 BCF+1373521 BCF+1373521 BCF+1373521muhammad rizwanNessuna valutazione finora

- Liability Products: Personal Banking Segment of SBIDocumento4 pagineLiability Products: Personal Banking Segment of SBIapu20090% (2)

- A Study On Credit Management at District CoDocumento86 pagineA Study On Credit Management at District CoIMAM JAVOOR100% (2)

- Reacharge & Balance Inquiry ProcedureDocumento8 pagineReacharge & Balance Inquiry ProcedureiprashNessuna valutazione finora

- Ambit Brochure Core BankingDocumento24 pagineAmbit Brochure Core BankingSwati SamantNessuna valutazione finora

- Dispute FormDocumento1 paginaDispute Formadarsh2dayNessuna valutazione finora

- Audit of Cash and Cash EquivalentsDocumento1 paginaAudit of Cash and Cash EquivalentsEmma Mariz Garcia50% (2)

- CAMELS Ratings Lori Buerger March 2012Documento4 pagineCAMELS Ratings Lori Buerger March 2012Nael Nasir ChiraghNessuna valutazione finora

- Statement of AccountDocumento7 pagineStatement of AccountHamza CollectionNessuna valutazione finora

- CFPB English Spanish Glossary of Financial Terms! PDFDocumento77 pagineCFPB English Spanish Glossary of Financial Terms! PDFruthieNessuna valutazione finora

- Http://202.83.164.226/complaint - Attachments//2019 11 08 07 47 20 1573181240 5457837 5dc4d738aff255.3935adb9d1b58f8c PDFDocumento2 pagineHttp://202.83.164.226/complaint - Attachments//2019 11 08 07 47 20 1573181240 5457837 5dc4d738aff255.3935adb9d1b58f8c PDFNaveed KhanNessuna valutazione finora

- CIMB Islamic Bank BHD V LCL Corp BHD & AnorDocumento20 pagineCIMB Islamic Bank BHD V LCL Corp BHD & Anormuhammad amriNessuna valutazione finora

- BSCS Admission (Phase-2) Fees ChallanDocumento1 paginaBSCS Admission (Phase-2) Fees ChallanAbdullah ChohanNessuna valutazione finora

- NothingDocumento4 pagineNothingSofia Louisse C. FernandezNessuna valutazione finora

- Anaalytics FirmsDocumento6 pagineAnaalytics FirmsAmit RanaNessuna valutazione finora

- Challan 32 A PDFDocumento2 pagineChallan 32 A PDFarshad aliNessuna valutazione finora

- Payment InstructionsDocumento3 paginePayment InstructionsadiksayyuuuuNessuna valutazione finora

- Check Writing Sim 1Documento13 pagineCheck Writing Sim 1api-256424511100% (1)

- Details of Statement: Tran Id Tran Date Remarks Amount (RS.) Balance (RS.)Documento2 pagineDetails of Statement: Tran Id Tran Date Remarks Amount (RS.) Balance (RS.)Ayan DuttaNessuna valutazione finora

- Oct RakbankDocumento2 pagineOct RakbankAditya MehtaNessuna valutazione finora

- Simple InterestDocumento3 pagineSimple InterestlalaNessuna valutazione finora

- List One: Currency, Fund and Precious Metal Codes: Entity Currency Alphabetic Code Numeric Code Minor UnitDocumento7 pagineList One: Currency, Fund and Precious Metal Codes: Entity Currency Alphabetic Code Numeric Code Minor UnitWu ThaNessuna valutazione finora