Potrebbero piacerti anche

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- CIR Vs CA (GR NO. 117982)Documento5 pagineCIR Vs CA (GR NO. 117982)Moon BeamsNessuna valutazione finora

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Essential of A Valid ContractDocumento3 pagineEssential of A Valid ContractMohammad HasanNessuna valutazione finora

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Cc202 - Contract ProcedureDocumento12 pagineCc202 - Contract ProcedurePhilimond SegieNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Adr 2-01 Am2 EsDocumento5 pagineAdr 2-01 Am2 EsFWEFWEFWNessuna valutazione finora

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- TDI-2013 Insurance Licensing HandbookDocumento39 pagineTDI-2013 Insurance Licensing Handbookjupode100% (1)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- 1-Personal Fitness Trainer License Application FormDocumento5 pagine1-Personal Fitness Trainer License Application FormSathish KumarNessuna valutazione finora

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Construction Delay Claims Khalil HassanDocumento38 pagineConstruction Delay Claims Khalil HassanØwięs MØhãmmedNessuna valutazione finora

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- IIA Response To Basel Internal Audit Function in Banks - Comment LetterDocumento3 pagineIIA Response To Basel Internal Audit Function in Banks - Comment Lettergalal2720006810Nessuna valutazione finora

- MCQ Taxes Tax Laws and Tax AdministrationDocumento4 pagineMCQ Taxes Tax Laws and Tax AdministrationImthe OneNessuna valutazione finora

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- DNFBP AML-CFT Regulatory Guidelines-18-5-18-FOR POSTINGDocumento38 pagineDNFBP AML-CFT Regulatory Guidelines-18-5-18-FOR POSTINGAndrea Lyn Salonga CacayNessuna valutazione finora

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

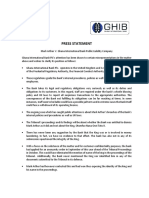

- Ghana International Bank's Press Statement On Otumfuor Money Laundering ScandalDocumento2 pagineGhana International Bank's Press Statement On Otumfuor Money Laundering ScandalGhanaWebNessuna valutazione finora

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

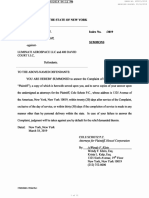

- Hexcel Corporation V Luminati Aerospace Summons and ComplaintDocumento12 pagineHexcel Corporation V Luminati Aerospace Summons and ComplaintRiverheadLOCALNessuna valutazione finora

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- 215 Scra 436Documento1 pagina215 Scra 436Dan LocsinNessuna valutazione finora

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- University of Petroleum and Energy Studies Act, 2003 UttrakhandDocumento63 pagineUniversity of Petroleum and Energy Studies Act, 2003 UttrakhandLatest Laws TeamNessuna valutazione finora

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- Secured Transactions and Collateral Registries A Global PerspectiveDocumento36 pagineSecured Transactions and Collateral Registries A Global PerspectiveADBI EventsNessuna valutazione finora

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Safety of Escalators and Moving Walks: BSI Standards PublicationDocumento36 pagineSafety of Escalators and Moving Walks: BSI Standards PublicationLorena Pertierra100% (1)

- Control of Asbestos Regulations 2006 ACOP L143 HSEDocumento98 pagineControl of Asbestos Regulations 2006 ACOP L143 HSEIbrahim IbrahimNessuna valutazione finora

- ISQ List of Reference Books PDFDocumento4 pagineISQ List of Reference Books PDFMuhammad NajeebNessuna valutazione finora

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Code of Ethics (PrPrac)Documento82 pagineCode of Ethics (PrPrac)nafsikah100% (1)

- FCP Business Plan Draft Dated April 16Documento19 pagineFCP Business Plan Draft Dated April 16api-252010520Nessuna valutazione finora

- Cebu Salvage and Home Insurance CaseDocumento2 pagineCebu Salvage and Home Insurance CaseIleenMaeNessuna valutazione finora

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- 01 Insular Life v. EbradoDocumento1 pagina01 Insular Life v. EbradoBasil MaguigadNessuna valutazione finora

- Sample Project Confidentiality AgreementDocumento1 paginaSample Project Confidentiality AgreementAditya Lakhani100% (1)

- Ilac G8 03 2009Documento8 pagineIlac G8 03 2009lauradimaNessuna valutazione finora

- Chapter Sixteen Cell SignalingDocumento96 pagineChapter Sixteen Cell SignalingRu LiliNessuna valutazione finora

- Companies Act, 1956: Presented To: Professor Sucheta JawleDocumento31 pagineCompanies Act, 1956: Presented To: Professor Sucheta JawleAbbas Haider NaqviNessuna valutazione finora

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Supply Chain Risk Management: NIST 800-53 Rev. 5 Compliance ChecklistDocumento29 pagineSupply Chain Risk Management: NIST 800-53 Rev. 5 Compliance ChecklistHasib100% (1)

- ManoDocumento15 pagineManoraaziqNessuna valutazione finora

- Ftbend Payroll Audit ProgghframDocumento6 pagineFtbend Payroll Audit ProgghframJenofDulwnNessuna valutazione finora

- IRDAI AddressesDocumento2 pagineIRDAI Addresseskgn1Nessuna valutazione finora

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)