Potrebbero piacerti anche

- Electronic Journal of Research in Educational Psychology 1696-2095Documento22 pagineElectronic Journal of Research in Educational Psychology 1696-2095Abdullah HashimNessuna valutazione finora

- Analysis of Competitive Advantage in The Perspective Of: Resources Based ViewDocumento20 pagineAnalysis of Competitive Advantage in The Perspective Of: Resources Based ViewAbdullah HashimNessuna valutazione finora

- Gazi Üniversitesi Ticaret Ve Tur: L) P (÷LWLP) DN OWHVL UG'Ro'U %Dúnhqwhqlyhuvlwhvl6Rv/Do%Lolpohu0Hvohn Nvhnrnxoxg÷U - UDocumento32 pagineGazi Üniversitesi Ticaret Ve Tur: L) P (÷LWLP) DN OWHVL UG'Ro'U %Dúnhqwhqlyhuvlwhvl6Rv/Do%Lolpohu0Hvohn Nvhnrnxoxg÷U - UAbdullah HashimNessuna valutazione finora

- An Evaluation of Performance Using The Balanced Scorecard Model For The University of Malawi's PolytechnicDocumento10 pagineAn Evaluation of Performance Using The Balanced Scorecard Model For The University of Malawi's PolytechnicAbdullah HashimNessuna valutazione finora

- Ajkfluids2015-28124: Optimization of Looped Airfoil Wind Turbine (Lawt) Design Parameters For Maximum Power GenerationDocumento7 pagineAjkfluids2015-28124: Optimization of Looped Airfoil Wind Turbine (Lawt) Design Parameters For Maximum Power GenerationAbdullah HashimNessuna valutazione finora

- EASJDOM 15 83-85 CDocumento4 pagineEASJDOM 15 83-85 CAbdullah Hashim100% (1)

- A Study On Financial Derivatives With Reference To Tata Motors Limited, Chittoor District of Ap, IndiaDocumento5 pagineA Study On Financial Derivatives With Reference To Tata Motors Limited, Chittoor District of Ap, IndiaAbdullah HashimNessuna valutazione finora

- Lubricants For Compaction of P/M ComponentsDocumento10 pagineLubricants For Compaction of P/M ComponentsAbdullah HashimNessuna valutazione finora

- PDFDocumento2 paginePDFAbdullah HashimNessuna valutazione finora

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Bsba Business Economics 2011Documento4 pagineBsba Business Economics 2011clarecieNessuna valutazione finora

- Final Zayredin AssignmentDocumento26 pagineFinal Zayredin AssignmentAmanuelNessuna valutazione finora

- 2 Chapter 2 - Purchasing StrategyDocumento52 pagine2 Chapter 2 - Purchasing StrategyMuhammad Arif FarhanNessuna valutazione finora

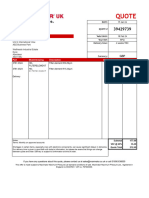

- Maximator Quote No 39429739Documento1 paginaMaximator Quote No 39429739William EvansNessuna valutazione finora

- A Study On Inventory Management in Amara Raja Batteries LTDDocumento4 pagineA Study On Inventory Management in Amara Raja Batteries LTDMadhav Ko0% (1)

- Resumo Cientifico ITIL Niveles de MadurezDocumento11 pagineResumo Cientifico ITIL Niveles de MadurezscapasNessuna valutazione finora

- 1 - Intro To FinanceDocumento23 pagine1 - Intro To FinanceYudna YuNessuna valutazione finora

- Brand Management Course OutlineDocumento8 pagineBrand Management Course OutlinechinmayNessuna valutazione finora

- Venga Tu ReinoDocumento2 pagineVenga Tu ReinoOmar camacho HernandezNessuna valutazione finora

- Project Proposal Guidlines For OOSADDocumento7 pagineProject Proposal Guidlines For OOSADhigh bright appNessuna valutazione finora

- FinMod 2022-2023 Tutorial 2 Exercise + AnswersDocumento41 pagineFinMod 2022-2023 Tutorial 2 Exercise + AnswersjjpasemperNessuna valutazione finora

- Project of Merger Acquisition SANJAYDocumento65 pagineProject of Merger Acquisition SANJAYmangundesanju77% (74)

- GE Countrywide Case StudyDocumento2 pagineGE Countrywide Case StudyPratyush Jaiswal100% (1)

- Literature ReviewDocumento3 pagineLiterature ReviewRohan SharmaNessuna valutazione finora

- FA GP5 Assignment 1Documento4 pagineFA GP5 Assignment 1saurabhNessuna valutazione finora

- h8 Cirr h1 2021Documento2 pagineh8 Cirr h1 2021Fadhlur RahmanNessuna valutazione finora

- A Primer On The Impact of The New Economic Stimulus Laws and IRC 409A On Executive Compensation in Mergers and AcquisitionsDocumento48 pagineA Primer On The Impact of The New Economic Stimulus Laws and IRC 409A On Executive Compensation in Mergers and AcquisitionsArnstein & Lehr LLPNessuna valutazione finora

- 09 Ratio AnalysisDocumento16 pagine09 Ratio AnalysisHimanshu VermaNessuna valutazione finora

- Introduction To Banking: Basics, Savings, Current, CCOD, Remittance, CashDocumento54 pagineIntroduction To Banking: Basics, Savings, Current, CCOD, Remittance, CashcutesunyNessuna valutazione finora

- Justification Letter SampleDocumento2 pagineJustification Letter SampleDinapuanNgLangaw100% (1)

- Bif4 A Guide To Writing A Business PlanDocumento5 pagineBif4 A Guide To Writing A Business PlanericksetiyawanNessuna valutazione finora

- The Future of Work - Insights Into The 2023 Gig Economy WorkforceDocumento13 pagineThe Future of Work - Insights Into The 2023 Gig Economy WorkforceakshayNessuna valutazione finora

- HSE TrainingDocumento12 pagineHSE Trainingpaeg6512100% (1)

- From Renter To OwnerDocumento21 pagineFrom Renter To OwnerAllen & UnwinNessuna valutazione finora

- Personal Financial Statement Template: General Rates Workcover Insurance Other OtherDocumento2 paginePersonal Financial Statement Template: General Rates Workcover Insurance Other OtherBenjiNessuna valutazione finora

- Hola-Kola ComputationsDocumento7 pagineHola-Kola ComputationsKristine Nitzkie SalazarNessuna valutazione finora

- Chapter 1 - Introduction To Management AccountingDocumento32 pagineChapter 1 - Introduction To Management Accountingyến lêNessuna valutazione finora

- Chapter 1 EnterprDocumento11 pagineChapter 1 EnterprSundas FareedNessuna valutazione finora

- Up To Date CVDocumento4 pagineUp To Date CViqbal1439988Nessuna valutazione finora

- Layout Plant PDFDocumento1 paginaLayout Plant PDFswarupNessuna valutazione finora