Potrebbero piacerti anche

- Applied Economic Analysis of Information and RiskDa EverandApplied Economic Analysis of Information and RiskMoriki HosoeNessuna valutazione finora

- Perfect Competition in Markets With Adverse SelectionDocumento40 paginePerfect Competition in Markets With Adverse SelectionRAHMADANY HANINDA AKMAL 1Nessuna valutazione finora

- Azevedo and Gottlieb - Competition With Adverse SelectionDocumento36 pagineAzevedo and Gottlieb - Competition With Adverse SelectionsouzajoseNessuna valutazione finora

- Economia Salud UDocumento24 pagineEconomia Salud UDavid CeledonNessuna valutazione finora

- Linear Price Equilibria in A Non-Exclusive Insurance MarketDocumento32 pagineLinear Price Equilibria in A Non-Exclusive Insurance MarketgpiaserNessuna valutazione finora

- Characterization and Uniqueness of Equilibrium in Competitive InsuranceDocumento43 pagineCharacterization and Uniqueness of Equilibrium in Competitive InsuranceAndré Medeiros SztutmanNessuna valutazione finora

- Foundations of International Strategy (Tilburg University) Foundations of International Strategy (Tilburg University)Documento8 pagineFoundations of International Strategy (Tilburg University) Foundations of International Strategy (Tilburg University)Еmil KostovNessuna valutazione finora

- Sample Ecopnomics EssayDocumento20 pagineSample Ecopnomics EssayduhneesNessuna valutazione finora

- Louberge and WattDocumento42 pagineLouberge and WattNadz EstrellaNessuna valutazione finora

- Need To RephraseDocumento7 pagineNeed To RephraseMushtaq Hussain KhanNessuna valutazione finora

- Dionne 1992Documento17 pagineDionne 1992Naveenkumar Ashok YaranalNessuna valutazione finora

- Competitive Insurance Markets With Two UnobservablesDocumento22 pagineCompetitive Insurance Markets With Two UnobservablespostscriptNessuna valutazione finora

- Pareto y Mercados Stanford NCDocumento27 paginePareto y Mercados Stanford NCaluevNessuna valutazione finora

- Kinh Te VI Mo DichDocumento28 pagineKinh Te VI Mo Dichtho.tnm.62ktptNessuna valutazione finora

- Active Screening in Insurance Markets: Corresponding AuthorDocumento22 pagineActive Screening in Insurance Markets: Corresponding AuthorYen SiangNessuna valutazione finora

- Chapter Eleven The Cost of Capital An Axiomatic ApproachDocumento21 pagineChapter Eleven The Cost of Capital An Axiomatic ApproachJoydeep AdakNessuna valutazione finora

- Competition With Hidden Knowledge (Riley, JPE 1985)Documento20 pagineCompetition With Hidden Knowledge (Riley, JPE 1985)Muhammad AbubakrNessuna valutazione finora

- Maskin y Riley - Monopoly With Incomplete Information - 1984 PDFDocumento27 pagineMaskin y Riley - Monopoly With Incomplete Information - 1984 PDFFernando FCNessuna valutazione finora

- Utility Multiname Credit WWWDocumento23 pagineUtility Multiname Credit WWWeeeeeeeeNessuna valutazione finora

- R L L I - W H B D W N B D ?: Esearch On Apse in IFE Nsurance HAT AS EEN One and HAT Eeds TO E ONEDocumento28 pagineR L L I - W H B D W N B D ?: Esearch On Apse in IFE Nsurance HAT AS EEN One and HAT Eeds TO E ONE3rlangNessuna valutazione finora

- A Comprehensive Note On The Informed Principal With Private Values and Independent TypesDocumento19 pagineA Comprehensive Note On The Informed Principal With Private Values and Independent TypesLucía QuesadaNessuna valutazione finora

- The Role of Repetition and Observability in DeterrDocumento15 pagineThe Role of Repetition and Observability in DeterrMohmmad QadiNessuna valutazione finora

- JEL Classification Keywords: BstractDocumento35 pagineJEL Classification Keywords: BstractsexscansexNessuna valutazione finora

- Risks 03 00445 PDFDocumento10 pagineRisks 03 00445 PDFNishi TaraiNessuna valutazione finora

- Report On Asymmetrical Information: by Charulata Das (15045) Gurpreet Kaur (15058)Documento19 pagineReport On Asymmetrical Information: by Charulata Das (15045) Gurpreet Kaur (15058)gurpreetNessuna valutazione finora

- Reinventing Consumer Protection: David Adam FriedmanDocumento48 pagineReinventing Consumer Protection: David Adam FriedmanSuprim ShresthaNessuna valutazione finora

- Multi ProjectDocumento2 pagineMulti ProjectAbdulaiAbubakarNessuna valutazione finora

- Notes Capital Structre TheoryDocumento24 pagineNotes Capital Structre TheoryJim MathilakathuNessuna valutazione finora

- A Simulation of The Insurance Industry The ProblemDocumento43 pagineA Simulation of The Insurance Industry The ProblemDavidon JaniNessuna valutazione finora

- Why People Buy Insurance: A Modern Answer To An Old QuestionDocumento42 pagineWhy People Buy Insurance: A Modern Answer To An Old QuestionGordo Yoel Alan MangiwaNessuna valutazione finora

- In Sur SymposiumDocumento30 pagineIn Sur Symposiumtsioney70Nessuna valutazione finora

- The Market For Catastrophic RiskDocumento43 pagineThe Market For Catastrophic Riskaaharis100% (1)

- Research Article On Comparison of Models For Count Data With Excessive Zeros in Non-Life InsuranceDocumento11 pagineResearch Article On Comparison of Models For Count Data With Excessive Zeros in Non-Life Insuranceእስክንድር ተፈሪNessuna valutazione finora

- Exclusive Contracts and Market Dominance: American Economic Review 2015, 105 (11) : 3321-3351Documento31 pagineExclusive Contracts and Market Dominance: American Economic Review 2015, 105 (11) : 3321-3351tataroi2307Nessuna valutazione finora

- Abstracts Source - The Journal of Risk and InsuranceDocumento18 pagineAbstracts Source - The Journal of Risk and InsurancedimmiNessuna valutazione finora

- Article 1Documento39 pagineArticle 1Bel Bahadur BoharaNessuna valutazione finora

- Asymmetric Information in Insurance Field: Some General ConsiderationsDocumento11 pagineAsymmetric Information in Insurance Field: Some General ConsiderationsAmmi JulianNessuna valutazione finora

- Actuarial Applications of A Hierarchical Insurance Claims ModelDocumento33 pagineActuarial Applications of A Hierarchical Insurance Claims ModelAprijon AnasNessuna valutazione finora

- Summary Of: The Value of Saving A Life: Evidence From The Labor MarketDocumento2 pagineSummary Of: The Value of Saving A Life: Evidence From The Labor MarketFreed DragsNessuna valutazione finora

- Summary Of: The Value of Saving A Life: Evidence From The Labor MarketDocumento2 pagineSummary Of: The Value of Saving A Life: Evidence From The Labor MarketFreed DragsNessuna valutazione finora

- Bernard Paper 2012Documento26 pagineBernard Paper 2012JuanCamiloGonzálezTrujilloNessuna valutazione finora

- Competition Law: Lerner's IndexDocumento7 pagineCompetition Law: Lerner's IndexRakshit Raj SinghNessuna valutazione finora

- Mba - Iii Sem Security Analysis & Portfolio Management - MF0001 Set - 2Documento10 pagineMba - Iii Sem Security Analysis & Portfolio Management - MF0001 Set - 2Dilipk86Nessuna valutazione finora

- Devt Vs EquityDocumento51 pagineDevt Vs EquityRania RebaiNessuna valutazione finora

- Structure, Development and Actuarial Valuation of Unit-Linked Policies in Life InsuranceDocumento55 pagineStructure, Development and Actuarial Valuation of Unit-Linked Policies in Life InsuranceRiccardo EspositoNessuna valutazione finora

- Risks 05 00029Documento21 pagineRisks 05 00029Rishi KumarNessuna valutazione finora

- SSRN Id702641Documento26 pagineSSRN Id702641Elina WagenaarNessuna valutazione finora

- Automobile Insurance Pric-2Documento8 pagineAutomobile Insurance Pric-2Initiald RazdNessuna valutazione finora

- This Content Downloaded From 152.58.177.231 On Sat, 15 Apr 2023 20:03:56 UTCDocumento30 pagineThis Content Downloaded From 152.58.177.231 On Sat, 15 Apr 2023 20:03:56 UTCRishabNessuna valutazione finora

- To Insure or Not To Insure?: An Insurance Puzzle: 2003 The Geneva AssociationDocumento20 pagineTo Insure or Not To Insure?: An Insurance Puzzle: 2003 The Geneva AssociationKusum Kali MitraNessuna valutazione finora

- Moral Hazard and Optimal Unemployment Insurance in An Economy With Heterogeneous SkillsDocumento18 pagineMoral Hazard and Optimal Unemployment Insurance in An Economy With Heterogeneous SkillspostscriptNessuna valutazione finora

- Literature Review On Insurance CompanyDocumento25 pagineLiterature Review On Insurance Companyjusmi86% (7)

- Probabilistic Estimation Based Data Mining For Discovering Insurance RisksDocumento19 pagineProbabilistic Estimation Based Data Mining For Discovering Insurance RisksDeepak TRNessuna valutazione finora

- The Costs of Financial Distress Across Industries: Arthur Korteweg September 20, 2007Documento59 pagineThe Costs of Financial Distress Across Industries: Arthur Korteweg September 20, 2007Fathimah Azzahra JafrilNessuna valutazione finora

- Objectives of The StudyDocumento7 pagineObjectives of The StudyPatel Akki100% (3)

- Bates Crash Risk MarketDocumento48 pagineBates Crash Risk Markettmp01@jesperlund.comNessuna valutazione finora

- Guia Act U7 A U10Documento21 pagineGuia Act U7 A U10Pedro FelipettiNessuna valutazione finora

- Risk Estimation Through The Analysis of Stock's Real ValueDocumento35 pagineRisk Estimation Through The Analysis of Stock's Real Valuebutch28butch28Nessuna valutazione finora

- Bookshop - Researchreports - Risk Pricing - Abi Research Paper No 11 - 2Documento22 pagineBookshop - Researchreports - Risk Pricing - Abi Research Paper No 11 - 2Akash BhatiaNessuna valutazione finora

- Is Insurance A Luxury?Documento3 pagineIs Insurance A Luxury?BobNessuna valutazione finora

- Principles of Managerial Finance Brief 8th Edition Zutter Solutions ManualDocumento35 paginePrinciples of Managerial Finance Brief 8th Edition Zutter Solutions Manualbosomdegerml971yf100% (25)

- Chapter 6: Risk and Risk AversionDocumento7 pagineChapter 6: Risk and Risk Aversionchm01989Nessuna valutazione finora

- HW6 2014Documento11 pagineHW6 2014Seung Pyo Son0% (1)

- Risk and Return Risk and ReturnDocumento33 pagineRisk and Return Risk and ReturnIxhaq motiwalaNessuna valutazione finora

- Introduction To Portfolio TheoryDocumento36 pagineIntroduction To Portfolio TheorySaish ChavanNessuna valutazione finora

- Chapter 6: Risk Aversion and Capital Allocation To Risky AssetsDocumento14 pagineChapter 6: Risk Aversion and Capital Allocation To Risky AssetsnouraNessuna valutazione finora

- ACTL3182 2018 Sem 2 Annotated Lecture NotesDocumento120 pagineACTL3182 2018 Sem 2 Annotated Lecture NotesAlex WuNessuna valutazione finora

- Examining Risk Tolerance in Project-Driven OrganizationDocumento5 pagineExamining Risk Tolerance in Project-Driven Organizationapi-3707091Nessuna valutazione finora

- Introduction To Investment MGMTDocumento6 pagineIntroduction To Investment MGMTShailendra AryaNessuna valutazione finora

- Behavioral Finance Foundations For InvestorsDocumento46 pagineBehavioral Finance Foundations For InvestorsMUHAMMAD IRFAN KHAN0% (1)

- Specific Performance 2Documento39 pagineSpecific Performance 2Shubham PandeyNessuna valutazione finora

- Holmstrom1982 Moral Hazard in TeamsDocumento18 pagineHolmstrom1982 Moral Hazard in TeamsfaqeveaNessuna valutazione finora

- An Introduction To Portfolio Theory: John NorstadDocumento29 pagineAn Introduction To Portfolio Theory: John NorstadAIP10Nessuna valutazione finora

- A Literature Review On Analyzing Investors Perceptions Towards Mutual Funds PDFDocumento6 pagineA Literature Review On Analyzing Investors Perceptions Towards Mutual Funds PDFSangam Sahoo100% (1)

- Solution Manual PDFDocumento73 pagineSolution Manual PDFJavid Far Disi100% (4)

- Danthine ExercisesDocumento22 pagineDanthine ExercisesmattNessuna valutazione finora

- CFA Level III Outline-Notes (2010)Documento114 pagineCFA Level III Outline-Notes (2010)Mark Oblad100% (2)

- Journal of Behavioral and Experimental Finance Volume 2 Issue 2014 (Doi 10.1016/j.jbef.2014.02.005) Nawrocki, David Viole, Fred - Behavioral Finance in Financial Market Theory, Utility Theory, Por PDFDocumento8 pagineJournal of Behavioral and Experimental Finance Volume 2 Issue 2014 (Doi 10.1016/j.jbef.2014.02.005) Nawrocki, David Viole, Fred - Behavioral Finance in Financial Market Theory, Utility Theory, Por PDFvan tinh khucNessuna valutazione finora

- CML Vs SMLDocumento9 pagineCML Vs SMLJoanna JacksonNessuna valutazione finora

- Risk & Return Analysis - Prime BookDocumento25 pagineRisk & Return Analysis - Prime Bookßïshñü PhüyãlNessuna valutazione finora

- Brownley Chap OneDocumento32 pagineBrownley Chap OneSara MaysNessuna valutazione finora

- Chapter 3 - Utility Theory: ST Petersburg ParadoxDocumento77 pagineChapter 3 - Utility Theory: ST Petersburg Paradoxabc123Nessuna valutazione finora

- Chapter 1Documento13 pagineChapter 1babak84Nessuna valutazione finora

- 10.chapter 1 (Introduction To Investments)Documento41 pagine10.chapter 1 (Introduction To Investments)nagsen thokeNessuna valutazione finora

- 07 - Chapter 2Documento60 pagine07 - Chapter 2Ritesh ChatterjeeNessuna valutazione finora

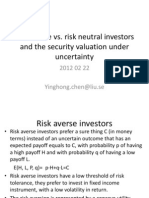

- Risk Averse Vs Risk Neutral InvestorsDocumento9 pagineRisk Averse Vs Risk Neutral InvestorsYinghong chenNessuna valutazione finora

- Behavioral Bias, Vaiuation, and Active ManagementDocumento10 pagineBehavioral Bias, Vaiuation, and Active ManagementDS ReishenNessuna valutazione finora

- 5 Written Questions: No Answer GivenDocumento4 pagine5 Written Questions: No Answer GivenBinod ThakurNessuna valutazione finora

- Behavioral Finance PPT Sept 1419 2022Documento40 pagineBehavioral Finance PPT Sept 1419 2022Ann RosoladaNessuna valutazione finora

- Money Banking and Financial Markets 5th Edition Cecchetti Test Bank 1Documento37 pagineMoney Banking and Financial Markets 5th Edition Cecchetti Test Bank 1david100% (49)

- A History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationDa EverandA History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationValutazione: 4 su 5 stelle4/5 (11)

- Look Again: The Power of Noticing What Was Always ThereDa EverandLook Again: The Power of Noticing What Was Always ThereValutazione: 5 su 5 stelle5/5 (3)

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassDa EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassNessuna valutazione finora

- Narrative Economics: How Stories Go Viral and Drive Major Economic EventsDa EverandNarrative Economics: How Stories Go Viral and Drive Major Economic EventsValutazione: 4.5 su 5 stelle4.5/5 (94)

- The Technology Trap: Capital, Labor, and Power in the Age of AutomationDa EverandThe Technology Trap: Capital, Labor, and Power in the Age of AutomationValutazione: 4.5 su 5 stelle4.5/5 (46)

- The Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumDa EverandThe Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumValutazione: 3 su 5 stelle3/5 (12)

- The Trillion-Dollar Conspiracy: How the New World Order, Man-Made Diseases, and Zombie Banks Are Destroying AmericaDa EverandThe Trillion-Dollar Conspiracy: How the New World Order, Man-Made Diseases, and Zombie Banks Are Destroying AmericaNessuna valutazione finora

- The New Elite: Inside the Minds of the Truly WealthyDa EverandThe New Elite: Inside the Minds of the Truly WealthyValutazione: 4 su 5 stelle4/5 (10)

- The War Below: Lithium, Copper, and the Global Battle to Power Our LivesDa EverandThe War Below: Lithium, Copper, and the Global Battle to Power Our LivesValutazione: 4.5 su 5 stelle4.5/5 (8)

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingDa EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingValutazione: 4.5 su 5 stelle4.5/5 (97)

- Vulture Capitalism: Corporate Crimes, Backdoor Bailouts, and the Death of FreedomDa EverandVulture Capitalism: Corporate Crimes, Backdoor Bailouts, and the Death of FreedomNessuna valutazione finora

- Chip War: The Quest to Dominate the World's Most Critical TechnologyDa EverandChip War: The Quest to Dominate the World's Most Critical TechnologyValutazione: 4.5 su 5 stelle4.5/5 (227)

- Economics 101: How the World WorksDa EverandEconomics 101: How the World WorksValutazione: 4.5 su 5 stelle4.5/5 (34)

- The Meth Lunches: Food and Longing in an American CityDa EverandThe Meth Lunches: Food and Longing in an American CityValutazione: 5 su 5 stelle5/5 (5)

- Principles for Dealing with the Changing World Order: Why Nations Succeed or FailDa EverandPrinciples for Dealing with the Changing World Order: Why Nations Succeed or FailValutazione: 4.5 su 5 stelle4.5/5 (237)

- Poor Economics: A Radical Rethinking of the Way to Fight Global PovertyDa EverandPoor Economics: A Radical Rethinking of the Way to Fight Global PovertyValutazione: 4.5 su 5 stelle4.5/5 (263)

- The Sovereign Individual: Mastering the Transition to the Information AgeDa EverandThe Sovereign Individual: Mastering the Transition to the Information AgeValutazione: 4.5 su 5 stelle4.5/5 (89)

- Doughnut Economics: Seven Ways to Think Like a 21st-Century EconomistDa EverandDoughnut Economics: Seven Ways to Think Like a 21st-Century EconomistValutazione: 4.5 su 5 stelle4.5/5 (37)

- The Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetDa EverandThe Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetNessuna valutazione finora

- Nudge: The Final Edition: Improving Decisions About Money, Health, And The EnvironmentDa EverandNudge: The Final Edition: Improving Decisions About Money, Health, And The EnvironmentValutazione: 4.5 su 5 stelle4.5/5 (92)

- Rewired: The McKinsey Guide to Outcompeting in the Age of Digital and AIDa EverandRewired: The McKinsey Guide to Outcompeting in the Age of Digital and AIValutazione: 5 su 5 stelle5/5 (1)