Potrebbero piacerti anche

- Bir Ruling 418-03 PDFDocumento2 pagineBir Ruling 418-03 PDFSor Elle100% (1)

- 112034-2005-Commissioner of Internal Revenue v. Toshiba20180404-1159-12ci6skDocumento15 pagine112034-2005-Commissioner of Internal Revenue v. Toshiba20180404-1159-12ci6skCamshtNessuna valutazione finora

- CIR VS. Sekisui Jushi Philippines, Inc.Documento1 paginaCIR VS. Sekisui Jushi Philippines, Inc.Abdulateef SahibuddinNessuna valutazione finora

- Cir vs. Amex, GR No. 152609Documento5 pagineCir vs. Amex, GR No. 152609Jani MisterioNessuna valutazione finora

- Petitioner Respondent Litigation Division (BIR) Avisado Agan Montenegro & AssociatesDocumento17 paginePetitioner Respondent Litigation Division (BIR) Avisado Agan Montenegro & AssociatesRobert Jayson UyNessuna valutazione finora

- Sec 107 VatDocumento3 pagineSec 107 VatPatti Ramos-SysonNessuna valutazione finora

- I. Title: Tax Refund Case of Philippine Airlines On Its Imported Cigarettes, Wines, and LiquorsDocumento16 pagineI. Title: Tax Refund Case of Philippine Airlines On Its Imported Cigarettes, Wines, and LiquorsEina Rivera TapnioNessuna valutazione finora

- VAT Ruling No. 16-09Documento4 pagineVAT Ruling No. 16-09Rieland CuevasNessuna valutazione finora

- CIR Vs American ExpressDocumento3 pagineCIR Vs American ExpressRepolyo Ket CabbageNessuna valutazione finora

- Commissioner of Internal Revenue vs. Sekisui JushiDocumento6 pagineCommissioner of Internal Revenue vs. Sekisui Jushivince005Nessuna valutazione finora

- DomondonDocumento40 pagineDomondonCharles TamNessuna valutazione finora

- Coral Bay Tax DigestDocumento3 pagineCoral Bay Tax DigestJonathan Dela Cruz100% (1)

- Cir Vs American ExpressDocumento2 pagineCir Vs American ExpressAnonymous ubixYANessuna valutazione finora

- Week 3 BCDocumento173 pagineWeek 3 BCA GrafiloNessuna valutazione finora

- Silkair Singapore V. CirDocumento6 pagineSilkair Singapore V. CirConie NovelaNessuna valutazione finora

- Business Taxes: Certified Accounting Technician NIAT Office 2015Documento33 pagineBusiness Taxes: Certified Accounting Technician NIAT Office 2015Anonymous Lz2qH7Nessuna valutazione finora

- Bir Ruling Da (Vat 050) 282 09Documento3 pagineBir Ruling Da (Vat 050) 282 09doraemoanNessuna valutazione finora

- VAT Ruling 75-99Documento2 pagineVAT Ruling 75-99Marlene TongsonNessuna valutazione finora

- Week 3 Tax 2 - Assignment - MIPRANUM, RJAYDocumento2 pagineWeek 3 Tax 2 - Assignment - MIPRANUM, RJAYAileen Mifranum IINessuna valutazione finora

- BIR RULING (DA-203-06) : April 3, 2006Documento2 pagineBIR RULING (DA-203-06) : April 3, 2006Richard100% (1)

- Revenue Regulations No. 13-18: CD Technologies Asia, Inc. © 2019Documento17 pagineRevenue Regulations No. 13-18: CD Technologies Asia, Inc. © 2019Lance MorilloNessuna valutazione finora

- Bar Review Lecture - VATDocumento71 pagineBar Review Lecture - VATIsagani DionelaNessuna valutazione finora

- Articles About VAT Zero-RatingDocumento8 pagineArticles About VAT Zero-RatingkmoNessuna valutazione finora

- 8 CIR v. American ExpressDocumento21 pagine8 CIR v. American ExpressHannah MedNessuna valutazione finora

- RR 13-2018Documento20 pagineRR 13-2018Nikka Bianca Remulla-IcallaNessuna valutazione finora

- RR No. 13-2018 (VAT Refund)Documento23 pagineRR No. 13-2018 (VAT Refund)Hailin QuintosNessuna valutazione finora

- CIR vs. ToshibaDocumento3 pagineCIR vs. ToshibaKayelyn Lat100% (1)

- Secretary Vs Lazatin: FactsDocumento6 pagineSecretary Vs Lazatin: FactsArah Mae BonillaNessuna valutazione finora

- Bir Train Vat 20180418Documento54 pagineBir Train Vat 20180418DanaNessuna valutazione finora

- Business Taxation Midterm Quiz 1 2 PhineeeDocumento4 pagineBusiness Taxation Midterm Quiz 1 2 PhineeeKaxy PHNessuna valutazione finora

- G.R. No. 150154Documento19 pagineG.R. No. 150154Henson MontalvoNessuna valutazione finora

- VAT Tax CasesDocumento12 pagineVAT Tax CasesAnna AbadNessuna valutazione finora

- Introduction To Business TaxesDocumento32 pagineIntroduction To Business TaxesGracelle Mae Oraller100% (2)

- Atlas Consolidated Mining V CIR (Case Digest)Documento2 pagineAtlas Consolidated Mining V CIR (Case Digest)Jeng Pion100% (1)

- RR No. 13-2018 CorrectedDocumento20 pagineRR No. 13-2018 CorrectedRap BaguioNessuna valutazione finora

- Commissioner OF Internal REVENUE, Petitioner, vs. American Express International, Inc. (Philippine BRANCH), RespondentDocumento18 pagineCommissioner OF Internal REVENUE, Petitioner, vs. American Express International, Inc. (Philippine BRANCH), RespondentJasfher CallejoNessuna valutazione finora

- Business Tax ReviewerDocumento22 pagineBusiness Tax ReviewereysiNessuna valutazione finora

- Tax - Special TopicsDocumento28 pagineTax - Special TopicsPrincess Diane VicenteNessuna valutazione finora

- 2 Value Added TaxDocumento216 pagine2 Value Added TaxnichNessuna valutazione finora

- Atlas Consolidated Mining and Development Corp. v. CIRDocumento1 paginaAtlas Consolidated Mining and Development Corp. v. CIRms_paupauNessuna valutazione finora

- Cir vs. Toshiba Information Equipment (Phils.), Inc.Documento2 pagineCir vs. Toshiba Information Equipment (Phils.), Inc.brendamanganaan100% (2)

- Value-Added Tax: Secs. 105 To 115Documento71 pagineValue-Added Tax: Secs. 105 To 115louise carinoNessuna valutazione finora

- CIR V Sekisui Jushi DigestDocumento2 pagineCIR V Sekisui Jushi DigestJomel ManaigNessuna valutazione finora

- Reviewer BTTDocumento14 pagineReviewer BTTAlthea Frances VasalloNessuna valutazione finora

- G.R. No. 178090 Panasonic Vs CIRDocumento4 pagineG.R. No. 178090 Panasonic Vs CIRRene ValentosNessuna valutazione finora

- Full Blown Case Commissioner Vs PhilphosDocumento4 pagineFull Blown Case Commissioner Vs PhilphosMary Imogen GdlNessuna valutazione finora

- 5 Cir Vs Toshiba Information Equipment Phils IncDocumento2 pagine5 Cir Vs Toshiba Information Equipment Phils Incsamaral bentesinkoNessuna valutazione finora

- Tax 56 Activity 2Documento2 pagineTax 56 Activity 2Hannah Alvarado BandolaNessuna valutazione finora

- VatDocumento50 pagineVatnikolaevnavalentinaNessuna valutazione finora

- Cir Vs Toshiba Information Equipment Phils IncDocumento1 paginaCir Vs Toshiba Information Equipment Phils IncJoseph FullNessuna valutazione finora

- Bureau of Internal RevenueDocumento11 pagineBureau of Internal RevenueRomer LesondatoNessuna valutazione finora

- Zero-Rated Sales PDFDocumento24 pagineZero-Rated Sales PDFNEstandaNessuna valutazione finora

- Excel Professional Services, Inc.: Management Firm of Professional Review and Training Center (PRTC)Documento3 pagineExcel Professional Services, Inc.: Management Firm of Professional Review and Training Center (PRTC)Mae Angiela TansecoNessuna valutazione finora

- Toshiba Information Equipment, Inc. v. CIRDocumento3 pagineToshiba Information Equipment, Inc. v. CIRJoshua AbadNessuna valutazione finora

- Cir V Gonzales FactsDocumento6 pagineCir V Gonzales FactsDawn BarondaNessuna valutazione finora

- CIR Vs Toshiba Information Equipment (Phils) Inc: 150154: August 9, 2005: J.Documento12 pagineCIR Vs Toshiba Information Equipment (Phils) Inc: 150154: August 9, 2005: J.Iris MendiolaNessuna valutazione finora

- Bar Review Companion: Taxation: Anvil Law Books Series, #4Da EverandBar Review Companion: Taxation: Anvil Law Books Series, #4Nessuna valutazione finora

- Impact assessment AAK: The impact of Tax on the Local Manufacture of PesticidesDa EverandImpact assessment AAK: The impact of Tax on the Local Manufacture of PesticidesNessuna valutazione finora

- Impact Assessment AAK: Taxes and the Local Manufacture of PesticidesDa EverandImpact Assessment AAK: Taxes and the Local Manufacture of PesticidesNessuna valutazione finora

- KNCCI Vihiga: enabling county revenue raising legislationDa EverandKNCCI Vihiga: enabling county revenue raising legislationNessuna valutazione finora

- RMC No. 18-2020Documento1 paginaRMC No. 18-2020preNessuna valutazione finora

- Republic of The Philippines, Petitioner: vs. MARELYN TANEDO MANALO, ResponsdentDocumento3 pagineRepublic of The Philippines, Petitioner: vs. MARELYN TANEDO MANALO, ResponsdentSor Elle100% (2)

- RMC No. 18-2020Documento1 paginaRMC No. 18-2020preNessuna valutazione finora

- RMC No. 18-2020Documento1 paginaRMC No. 18-2020preNessuna valutazione finora

- 0504 JMC Dofdti PDFDocumento11 pagine0504 JMC Dofdti PDFBryan Yee LaborNessuna valutazione finora

- Batas Pambansa Bilang 68Documento29 pagineBatas Pambansa Bilang 68Sor ElleNessuna valutazione finora

- CITY of ManilaDocumento4 pagineCITY of ManilaSor ElleNessuna valutazione finora

- Guzman Bocaling Vs BonnevieDocumento2 pagineGuzman Bocaling Vs BonnevieSor Elle100% (1)

- Guzman Bocaling Vs BonnevieDocumento2 pagineGuzman Bocaling Vs BonnevieSor Elle100% (1)

- Ohio vs. RobinetteDocumento2 pagineOhio vs. RobinetteSor ElleNessuna valutazione finora

- Ignacio Barzaga v. CADocumento2 pagineIgnacio Barzaga v. CASor ElleNessuna valutazione finora

- Bill of Rights (Philippines)Documento2 pagineBill of Rights (Philippines)Jen100% (3)

- Yaptinchay vs. TorresDocumento2 pagineYaptinchay vs. TorresSor ElleNessuna valutazione finora

- Rule 70 MCQDocumento7 pagineRule 70 MCQSor ElleNessuna valutazione finora

- Negros SlashersDocumento4 pagineNegros SlashersSor ElleNessuna valutazione finora

- Naldoza, V. RepublicDocumento2 pagineNaldoza, V. RepublicSor ElleNessuna valutazione finora

- Paterno v. PaternoDocumento2 paginePaterno v. PaternoSor Elle100% (1)

- Belle Notes - SalesDocumento33 pagineBelle Notes - SalesSor ElleNessuna valutazione finora

- Terre vs. TerreDocumento2 pagineTerre vs. TerreSor ElleNessuna valutazione finora

- Gomez v. LipanaDocumento2 pagineGomez v. LipanaSor ElleNessuna valutazione finora

- Pedro de Guzman Vs CaDocumento11 paginePedro de Guzman Vs CaSor ElleNessuna valutazione finora

- Sun LifeDocumento4 pagineSun LifeSor ElleNessuna valutazione finora

- International Covenant On Civil and Political RightsDocumento92 pagineInternational Covenant On Civil and Political Rightsaudzgusi100% (1)

- Civil Law Rev Le Belle NotesDocumento10 pagineCivil Law Rev Le Belle NotesSor ElleNessuna valutazione finora

- Forcible Entry and Unlawful Detainer Applicable LawsDocumento10 pagineForcible Entry and Unlawful Detainer Applicable LawsSor ElleNessuna valutazione finora

- Katarungang Pambarangay: A HandbookDocumento134 pagineKatarungang Pambarangay: A HandbookCarl92% (101)

- BOC 2015 Civil Law Reviewer (Final)Documento602 pagineBOC 2015 Civil Law Reviewer (Final)Joshua Laygo Sengco88% (17)

- Primer On GrievanceDocumento67 paginePrimer On Grievanceymervegim02Nessuna valutazione finora

- Electronic Reservation Slip (ERS) : 4361490073 22503/Dbrg Vivek Exp Sleeper Class (SL)Documento3 pagineElectronic Reservation Slip (ERS) : 4361490073 22503/Dbrg Vivek Exp Sleeper Class (SL)vishnuvardhini121Nessuna valutazione finora

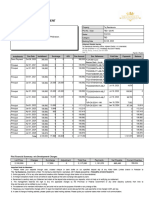

- Payroll Workshop: Alaras, Arla Gabrielle (A0012)Documento15 paginePayroll Workshop: Alaras, Arla Gabrielle (A0012)ellaine villafaniaNessuna valutazione finora

- Sumit PassbookDocumento5 pagineSumit PassbookSumitNessuna valutazione finora

- 6 Months Bank Statement Moaz MohsinDocumento2 pagine6 Months Bank Statement Moaz MohsinYuchu Asif100% (1)

- Bain Online Test PDFDocumento21 pagineBain Online Test PDFAvedeoNessuna valutazione finora

- Taj Residencia: Customer Account StatementDocumento1 paginaTaj Residencia: Customer Account StatementGohar SaeedNessuna valutazione finora

- Answers Bus Ad 4 MIDTERMDocumento3 pagineAnswers Bus Ad 4 MIDTERMJophie AndreilleNessuna valutazione finora

- MT760 HSBC PLC LondonDocumento2 pagineMT760 HSBC PLC LondonEdwin W Ng87% (15)

- Invoice DocumentDocumento1 paginaInvoice DocumentALL IN ONENessuna valutazione finora

- Mastering QuickBooks Payroll 2013Documento105 pagineMastering QuickBooks Payroll 2013Chanty Sridhar100% (2)

- Blessing Plastic: Tax Invoice Original For CompanyDocumento1 paginaBlessing Plastic: Tax Invoice Original For CompanyCharles NaveenNessuna valutazione finora

- Liechtenstein's New Tax LawDocumento8 pagineLiechtenstein's New Tax LawMaksim DyachukNessuna valutazione finora

- Advance Payment of TaxDocumento3 pagineAdvance Payment of TaxsadathnooriNessuna valutazione finora

- Incometaxation Chapter8Documento14 pagineIncometaxation Chapter8monneNessuna valutazione finora

- Resident Income Tax Return: Warning: Please Use A Different PDF ViewerDocumento5 pagineResident Income Tax Return: Warning: Please Use A Different PDF ViewermattNessuna valutazione finora

- Bill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountDocumento1 paginaBill To / Ship To:: Qty Gross Amount Discount Other Charges Taxable Amount CGST SGST/ Ugst Igst Cess Total AmountSidhant Singh100% (1)

- BALANCE CASH HOLDING AssignDocumento3 pagineBALANCE CASH HOLDING AssignJarra Abdurahman100% (2)

- выписка месяцDocumento3 pagineвыписка месяцeskanderzunisbaevNessuna valutazione finora

- 22 06 2023 - External Fund Transfer - AllDocumento17 pagine22 06 2023 - External Fund Transfer - Allmeliodas dragonNessuna valutazione finora

- Trimurti Travels: Igst SGST CGSTDocumento1 paginaTrimurti Travels: Igst SGST CGSTWORLD BINNessuna valutazione finora

- A/c Hoglo (876: AdjustmentDocumento1 paginaA/c Hoglo (876: AdjustmentUshat KanharNessuna valutazione finora

- A211 MC 7 - StudentDocumento4 pagineA211 MC 7 - StudentWon HaNessuna valutazione finora

- Company Unit 4th - Aug - 2021Documento17 pagineCompany Unit 4th - Aug - 2021cubadesignstudNessuna valutazione finora

- How To Understand Payment Industry in BrazilDocumento32 pagineHow To Understand Payment Industry in BrazilVictor SantosNessuna valutazione finora

- TGL AP - List Doc - Owner Code Supplier Vendor Invoice SistemDocumento4 pagineTGL AP - List Doc - Owner Code Supplier Vendor Invoice SistemBego BangetNessuna valutazione finora

- Black Book of GSTDocumento3 pagineBlack Book of GSTDeepak YadavNessuna valutazione finora

- Invoice OD119939448063285000Documento1 paginaInvoice OD119939448063285000ShivNessuna valutazione finora

- CAM-Accounting For Income Taxes - Nike 2020 10KDocumento1 paginaCAM-Accounting For Income Taxes - Nike 2020 10KnofeNessuna valutazione finora

- Chapter 4 Gross IncomeDocumento11 pagineChapter 4 Gross IncomeGlomarie Gonayon100% (1)

- 0ZQ73 0ZQ73 2075 20220101 W2Report W2Report 001Documento2 pagine0ZQ73 0ZQ73 2075 20220101 W2Report W2Report 001ligia vazquezNessuna valutazione finora