Potrebbero piacerti anche

- CertificateDocumento1 paginaCertificatedatsnoNessuna valutazione finora

- Labpractice 2Documento29 pagineLabpractice 2Rajashree Das100% (2)

- A Brief Introduction to MATLAB: Taken From the Book "MATLAB for Beginners: A Gentle Approach"Da EverandA Brief Introduction to MATLAB: Taken From the Book "MATLAB for Beginners: A Gentle Approach"Valutazione: 2.5 su 5 stelle2.5/5 (2)

- Combinatorial Optimization: Alexander SchrijverDocumento34 pagineCombinatorial Optimization: Alexander SchrijverWilfredo FelixNessuna valutazione finora

- Tasks A TreesDocumento14 pagineTasks A TreesAmos Keli MutuaNessuna valutazione finora

- Matlab OverviewDocumento11 pagineMatlab OverviewAhmad HosseinbeigNessuna valutazione finora

- Matlab Report File: Amity School of Engineering and TechnologyDocumento8 pagineMatlab Report File: Amity School of Engineering and TechnologySagar WadhwaNessuna valutazione finora

- 20BCE1205 Lab3Documento9 pagine20BCE1205 Lab3SHUBHAM OJHANessuna valutazione finora

- 20BCE1205 Lab3Documento9 pagine20BCE1205 Lab3SHUBHAM OJHANessuna valutazione finora

- 2.3 SciPy-1Documento17 pagine2.3 SciPy-1Aman RajNessuna valutazione finora

- Introduction To Matlab: Muhammad AbdullahDocumento14 pagineIntroduction To Matlab: Muhammad AbdullahMuhammad Abdullah ButtNessuna valutazione finora

- Kelompok 3 - Latihan 1 Setup Python Dan Aljabar LinierDocumento12 pagineKelompok 3 - Latihan 1 Setup Python Dan Aljabar LinierSatrya Budi PratamaNessuna valutazione finora

- Functions and PackagesDocumento7 pagineFunctions and PackagesNur SyazlianaNessuna valutazione finora

- Feedback and Control Systems Laboratory: ECEA107L/E02/2Q2021Documento26 pagineFeedback and Control Systems Laboratory: ECEA107L/E02/2Q2021Kim Andre Macaraeg100% (2)

- Assignment 1 - Replication of Outputs From "Torfs+Brauer-Short-R-Intro - PDF" Business ForecastingDocumento8 pagineAssignment 1 - Replication of Outputs From "Torfs+Brauer-Short-R-Intro - PDF" Business ForecastingHarshith HirisaveNessuna valutazione finora

- Assignment 2: Introduction To R: Text Like This Will Be Problems For You To Do and Turn In. (There Are 7 in All.)Documento15 pagineAssignment 2: Introduction To R: Text Like This Will Be Problems For You To Do and Turn In. (There Are 7 in All.)keyojeliNessuna valutazione finora

- SciPy 1Documento17 pagineSciPy 1mNessuna valutazione finora

- Halstead Software ScienceDocumento2 pagineHalstead Software Scienceyusra22100% (1)

- Lecture 4Documento2 pagineLecture 4datsnoNessuna valutazione finora

- ML Ex8Documento2 pagineML Ex8yefigoh133Nessuna valutazione finora

- R Studio Practicals-1Documento29 pagineR Studio Practicals-1rajshukla7748Nessuna valutazione finora

- Wxmaxima File - WXMXDocumento24 pagineWxmaxima File - WXMXSneha KBNessuna valutazione finora

- RECON BRX 2017 r2m2Documento73 pagineRECON BRX 2017 r2m2paulNessuna valutazione finora

- 3 LabDocumento6 pagine3 LabkhawarNessuna valutazione finora

- Homework Assignment 3 Homework Assignment 3Documento10 pagineHomework Assignment 3 Homework Assignment 3Ido AkovNessuna valutazione finora

- Sas/Iml: Departemen Statistika Fakultas Matematika Dan IPA 2013Documento14 pagineSas/Iml: Departemen Statistika Fakultas Matematika Dan IPA 2013MUHAMADFR11sNessuna valutazione finora

- An Introduction To Sci LabDocumento9 pagineAn Introduction To Sci Labهانى خيرNessuna valutazione finora

- 10 Minutos Con MaximaDocumento9 pagine10 Minutos Con Maximadeivis William gonzales aldazNessuna valutazione finora

- A Tour of Sage: Release 6.0Documento13 pagineA Tour of Sage: Release 6.0mohsindalvi87Nessuna valutazione finora

- C6713 Lab ManualDocumento51 pagineC6713 Lab Manualsmganorkar100% (1)

- Par - 1 In-Term Exam - Course 2017/18-Q2Documento7 paginePar - 1 In-Term Exam - Course 2017/18-Q2JuanNessuna valutazione finora

- DeltapdfDocumento3 pagineDeltapdfVIJAY YADAVNessuna valutazione finora

- Hackerrank NodejsDocumento19 pagineHackerrank NodejsSHIVAM SHRIVASTAVA67% (3)

- 2D Array ExamplesDocumento11 pagine2D Array Examplesmehar kashifNessuna valutazione finora

- 1 - Standard Linear Regression: Numpy NP PandasDocumento4 pagine1 - Standard Linear Regression: Numpy NP PandasWahib NakhoulNessuna valutazione finora

- Decision-Tree-Lab 3Documento4 pagineDecision-Tree-Lab 3api-559045701Nessuna valutazione finora

- '/content/data - PKL' 'RB': Open PrintDocumento5 pagine'/content/data - PKL' 'RB': Open PrintRavi KNessuna valutazione finora

- Introduction To MATLABDocumento38 pagineIntroduction To MATLABMukt ShahNessuna valutazione finora

- Machine Learning LabDocumento23 pagineMachine Learning Labops sksNessuna valutazione finora

- Bab Iii, Iv, V FixDocumento27 pagineBab Iii, Iv, V FixNela MuetzNessuna valutazione finora

- Norwegian Spruces - Main Effects and Interaction: 1 ModelDocumento4 pagineNorwegian Spruces - Main Effects and Interaction: 1 Modelaraz artaNessuna valutazione finora

- A Zeros (3,5) B Ones (3,4) C Eye (3) % Diagonal MatrixDocumento4 pagineA Zeros (3,5) B Ones (3,4) C Eye (3) % Diagonal MatrixshodmonNessuna valutazione finora

- Chapter 15 Loss DistributionsDocumento13 pagineChapter 15 Loss DistributionsBryanNessuna valutazione finora

- Pseudo Code of Mpi ProgramsDocumento22 paginePseudo Code of Mpi ProgramsAshfaq MirNessuna valutazione finora

- Midterm 2 CodesDocumento15 pagineMidterm 2 CodessameertardaNessuna valutazione finora

- MATLAB Command Window 1/4 July 26, 2018 11:32:03 PM: % Nama: Moch. Syahrul Siddiq M % NIM: 2111161001 % Tugas 7Documento4 pagineMATLAB Command Window 1/4 July 26, 2018 11:32:03 PM: % Nama: Moch. Syahrul Siddiq M % NIM: 2111161001 % Tugas 7Fiqhry ZulfikarNessuna valutazione finora

- MaximaDocumento417 pagineMaximaEnrique ProfesorNessuna valutazione finora

- Assignments Walkthroughs and R Demo: W4290 Statistical Methods in Finance - Spring 2010 - Columbia UniversityDocumento38 pagineAssignments Walkthroughs and R Demo: W4290 Statistical Methods in Finance - Spring 2010 - Columbia UniversitytsitNessuna valutazione finora

- Introduction To MATLABDocumento30 pagineIntroduction To MATLABTrí Minh CaoNessuna valutazione finora

- Shadab - DS Lab FileDocumento17 pagineShadab - DS Lab FileEdu On PointsNessuna valutazione finora

- Regression: Pyspark - SQLDocumento5 pagineRegression: Pyspark - SQLAli AbdiNessuna valutazione finora

- Lecture 01 (Creating Variables & Arrays)Documento94 pagineLecture 01 (Creating Variables & Arrays)Efrem HabNessuna valutazione finora

- R AssignmentDocumento8 pagineR AssignmentTunaNessuna valutazione finora

- MATLAB Command Window: 'Ga68 - Scatter Corrected - 12i - 163.dcm'Documento8 pagineMATLAB Command Window: 'Ga68 - Scatter Corrected - 12i - 163.dcm'Abyan JadidanNessuna valutazione finora

- Business Analytics-1: STR (Crew - Data)Documento16 pagineBusiness Analytics-1: STR (Crew - Data)Nikhil MalhotraNessuna valutazione finora

- Lecture 22Documento64 pagineLecture 22Tev WallaceNessuna valutazione finora

- R Workshop PART 2Documento36 pagineR Workshop PART 2Izzue KashfiNessuna valutazione finora

- Notes 5 Working With NumPy 1sep2022Documento12 pagineNotes 5 Working With NumPy 1sep2022jeremyNessuna valutazione finora

- Procedure:: Macaraeg, Kim Andre S. Prelimenary Data Sheet (PDS) ECEA107 - E02Documento10 pagineProcedure:: Macaraeg, Kim Andre S. Prelimenary Data Sheet (PDS) ECEA107 - E02Kim Andre MacaraegNessuna valutazione finora

- Jaycolpdf 1Documento5 pagineJaycolpdf 1P Samyutha 22107849101Nessuna valutazione finora

- Bvarsv ReplicationDocumento13 pagineBvarsv ReplicationRene BarreraNessuna valutazione finora

- Stock IndicatorDocumento2 pagineStock IndicatordatsnoNessuna valutazione finora

- Corps@sos - Wa.gov: UBI Number: 601 257 413 Business NameDocumento1 paginaCorps@sos - Wa.gov: UBI Number: 601 257 413 Business NamedatsnoNessuna valutazione finora

- Corps@sos - Wa.gov: UBI Number: 601 257 413 Business NameDocumento1 paginaCorps@sos - Wa.gov: UBI Number: 601 257 413 Business NamedatsnoNessuna valutazione finora

- Commercial Statement of Change: Existing Registered AgentDocumento2 pagineCommercial Statement of Change: Existing Registered AgentdatsnoNessuna valutazione finora

- Corps@sos - Wa.gov: UBI Number: 602 946 134 Business NameDocumento1 paginaCorps@sos - Wa.gov: UBI Number: 602 946 134 Business NamedatsnoNessuna valutazione finora

- CongratulationLetterDocumento1 paginaCongratulationLetterdatsnoNessuna valutazione finora

- Commercial Statement of Change: Existing Registered AgentDocumento2 pagineCommercial Statement of Change: Existing Registered AgentdatsnoNessuna valutazione finora

- Corps@sos - Wa.gov: UBI Number: 601 257 413 Business NameDocumento1 paginaCorps@sos - Wa.gov: UBI Number: 601 257 413 Business NamedatsnoNessuna valutazione finora

- Page: 1 of 2: Work Order #: 2020012800054474 - 1 Received Date: 01/28/2020 Amount Received: $0.00Documento2 paginePage: 1 of 2: Work Order #: 2020012800054474 - 1 Received Date: 01/28/2020 Amount Received: $0.00datsnoNessuna valutazione finora

- Corps@sos - Wa.gov: UBI Number: 601 257 413 Business NameDocumento1 paginaCorps@sos - Wa.gov: UBI Number: 601 257 413 Business NamedatsnoNessuna valutazione finora

- Bias For The DayDocumento28 pagineBias For The DaydatsnoNessuna valutazione finora

- Basic Employee Training On Covid-19 Infection Prevention: June, 2020Documento16 pagineBasic Employee Training On Covid-19 Infection Prevention: June, 2020datsnoNessuna valutazione finora

- Foreign Registration Statement: Ubi NumberDocumento3 pagineForeign Registration Statement: Ubi NumberdatsnoNessuna valutazione finora

- Guidance For Daily COVID-19 Screening of Staff and VisitorsDocumento2 pagineGuidance For Daily COVID-19 Screening of Staff and VisitorsdatsnoNessuna valutazione finora

- RTD ToS Fields ExamplesDocumento2 pagineRTD ToS Fields ExamplesdatsnoNessuna valutazione finora

- FilingCorrespondence CongratulationLetterDocumento1 paginaFilingCorrespondence CongratulationLetterdatsnoNessuna valutazione finora

- Guidance On Developing A COVID-19 Safety Plan For Critical InfrastructureDocumento3 pagineGuidance On Developing A COVID-19 Safety Plan For Critical InfrastructuredatsnoNessuna valutazione finora

- Aussie Dollar PDFDocumento1 paginaAussie Dollar PDFdatsnoNessuna valutazione finora

- Aussie Dollar PDFDocumento1 paginaAussie Dollar PDFdatsnoNessuna valutazione finora

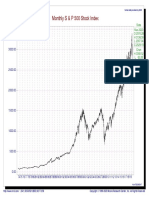

- Monthly S & P 500 Stock IndexDocumento1 paginaMonthly S & P 500 Stock IndexdatsnoNessuna valutazione finora

- Unified Bonds 20141008Documento57 pagineUnified Bonds 20141008datsnoNessuna valutazione finora

- Chicago Boothf Garch ScriptDocumento6 pagineChicago Boothf Garch ScriptdatsnoNessuna valutazione finora

- As of 12/31/14 10 Yrs. 25 Yrs. 50 Yrs. 75 Yrs. Since 1927 The Balanced Portfolio 60/40 Cash 1.6% 3.3% 5.4% 4.1% 3.7%Documento3 pagineAs of 12/31/14 10 Yrs. 25 Yrs. 50 Yrs. 75 Yrs. Since 1927 The Balanced Portfolio 60/40 Cash 1.6% 3.3% 5.4% 4.1% 3.7%datsnoNessuna valutazione finora

- Basics of Deep Learning: Pierre-Marc Jodoin and Christian DesrosiersDocumento183 pagineBasics of Deep Learning: Pierre-Marc Jodoin and Christian DesrosiersalyasocialwayNessuna valutazione finora

- Assignment 2 Management ScienceDocumento5 pagineAssignment 2 Management ScienceCheah Cheok NamNessuna valutazione finora

- FLT Course ManualDocumento28 pagineFLT Course Manualደመር ወድባርተ ቃንጪNessuna valutazione finora

- DSA - Question Bank - 2023Documento4 pagineDSA - Question Bank - 2023trupti.kodinariya9810Nessuna valutazione finora

- Circular QueueDocumento3 pagineCircular QueuekailasNessuna valutazione finora

- Maximum Flow: Algorithms and NetworksDocumento55 pagineMaximum Flow: Algorithms and NetworksduhancaracioloNessuna valutazione finora

- 2016 Graph SdaDocumento107 pagine2016 Graph SdaElisa OktavianiNessuna valutazione finora

- Lambda Calculus CLCDocumento38 pagineLambda Calculus CLCDan Mark Pidor BagsicanNessuna valutazione finora

- Problem A. Ladder: Input File FormatDocumento11 pagineProblem A. Ladder: Input File FormatSanskar BhargavaNessuna valutazione finora

- 3 - Design and Analysis of AlgorithmsDocumento188 pagine3 - Design and Analysis of AlgorithmsUdupiSri groupNessuna valutazione finora

- Computer Architecture and OrganizationDocumento46 pagineComputer Architecture and OrganizationALEMU DEMIRACHEWNessuna valutazione finora

- Q1 RA Vs RCDocumento6 pagineQ1 RA Vs RCdemisewNessuna valutazione finora

- Data Structures A Algorithms Multiple Choset 3Documento6 pagineData Structures A Algorithms Multiple Choset 3syrissco123Nessuna valutazione finora

- Optimization & Relaibility - Machine DesignDocumento2 pagineOptimization & Relaibility - Machine DesignYaswanthNessuna valutazione finora

- Neutrosophic Path-ColoringDocumento162 pagineNeutrosophic Path-ColoringHenry GarrettNessuna valutazione finora

- ML Session 15 BackpropagationDocumento30 pagineML Session 15 Backpropagationkr8665894Nessuna valutazione finora

- CS 473: Algorithms: Chandra Chekuri Chekuri@cs - Illinois.edu 3228 Siebel CenterDocumento98 pagineCS 473: Algorithms: Chandra Chekuri Chekuri@cs - Illinois.edu 3228 Siebel CenterNguyễn Quang HuyNessuna valutazione finora

- Operations Research Elective 3 1 0 4: 3/2/1: High/Medium/LowDocumento10 pagineOperations Research Elective 3 1 0 4: 3/2/1: High/Medium/LowNAJIYA NAZRIN P NNessuna valutazione finora

- Activity2 2623Documento14 pagineActivity2 2623ryle34Nessuna valutazione finora

- 19 Pragmatic Two Level OptimizationDocumento5 pagine19 Pragmatic Two Level OptimizationTADeNessuna valutazione finora

- Minimum Refueling Stops: Problem 8Documento24 pagineMinimum Refueling Stops: Problem 8ZainNessuna valutazione finora

- NNdemo MatlabDocumento7 pagineNNdemo MatlabMohammed MahdiNessuna valutazione finora

- Distributed Systems: Global StatesDocumento18 pagineDistributed Systems: Global StatesArjuna KrishNessuna valutazione finora

- Slides Lecture03Documento39 pagineSlides Lecture03dummyNessuna valutazione finora

- CS 188: Artificial Intelligence: Constraint Satisfaction ProblemsDocumento43 pagineCS 188: Artificial Intelligence: Constraint Satisfaction ProblemsSufi NoraniNessuna valutazione finora

- Applied Soft Computing Journal: EditorialDocumento3 pagineApplied Soft Computing Journal: EditorialEwerton DuarteNessuna valutazione finora

- Turing MachinesDocumento12 pagineTuring MachinesShashank Koundinya CherukuNessuna valutazione finora

- Dayananda Sagar College of EngineeringDocumento3 pagineDayananda Sagar College of EngineeringPower System Analysis-1Nessuna valutazione finora

- Assignment ProblemsDocumento36 pagineAssignment Problemsmanisha sonawane100% (2)