Potrebbero piacerti anche

- Rs. 54.67 Lakh Property Valuation Report for 2BHK Apartment in Greater NoidaDocumento5 pagineRs. 54.67 Lakh Property Valuation Report for 2BHK Apartment in Greater NoidaHenry KotoNessuna valutazione finora

- Definition of Common Real Estate TermsDocumento20 pagineDefinition of Common Real Estate TermsloterryjrNessuna valutazione finora

- Property Valuation PrinciplesDocumento13 pagineProperty Valuation PrinciplesAmulie JarjuseyNessuna valutazione finora

- Valuation Principles and Procedures by Dr. Ashok NainDocumento2 pagineValuation Principles and Procedures by Dr. Ashok Nainmukul_goyalin33% (3)

- Appraisal 1426 N 3rd St. HarrisburgDocumento84 pagineAppraisal 1426 N 3rd St. HarrisburgPennLive100% (1)

- Final Valuation Report - DMI - FEB 2014Documento33 pagineFinal Valuation Report - DMI - FEB 2014Soumi DasNessuna valutazione finora

- Valuation of Real PDocumento5 pagineValuation of Real PKowsalyaNessuna valutazione finora

- LBP AppraisalDocumento24 pagineLBP Appraisaldonaldhax01Nessuna valutazione finora

- Introduction To Theory & Practice of Fixed Asset Valuation Based On Market ApproachDocumento19 pagineIntroduction To Theory & Practice of Fixed Asset Valuation Based On Market ApproachGagan100% (1)

- Valuation Report SampleDocumento8 pagineValuation Report SampleBoghiu ZNessuna valutazione finora

- Salford University School of Built Environment BSC Property Management and InvestmentDocumento26 pagineSalford University School of Built Environment BSC Property Management and InvestmentThomas MacdonaldNessuna valutazione finora

- Real Property Valuation Methods & TechniquesDocumento7 pagineReal Property Valuation Methods & TechniquesLavanya LakshmiNessuna valutazione finora

- Valuation Methods for Real EstateDocumento16 pagineValuation Methods for Real EstateKishor AhirNessuna valutazione finora

- Property Management Proposal Template FreeDocumento12 pagineProperty Management Proposal Template FreeLiz100% (1)

- Income Approach ExplainedDocumento156 pagineIncome Approach ExplainedMinani Marc100% (1)

- Real Estate Valuation FactorsDocumento52 pagineReal Estate Valuation FactorsRamesh KumarNessuna valutazione finora

- Contractor Method For ValuationDocumento2 pagineContractor Method For Valuationpschil100% (1)

- Triple Net Lease Cap Rate ReportDocumento3 pagineTriple Net Lease Cap Rate ReportnetleaseNessuna valutazione finora

- Guide Valuation Unregistered Land PDFDocumento84 pagineGuide Valuation Unregistered Land PDFVishal BalrajNessuna valutazione finora

- Commercial Land Valuation ReportDocumento4 pagineCommercial Land Valuation ReportveepuruNessuna valutazione finora

- 19RM919 (Ishmeet)Documento3 pagine19RM919 (Ishmeet)PRANAV JAIN - RMNessuna valutazione finora

- Appraisal Report For Gordon River Apartments Paid by The City of Naples - January 2021Documento114 pagineAppraisal Report For Gordon River Apartments Paid by The City of Naples - January 2021Omar Rodriguez OrtizNessuna valutazione finora

- Valuation Report of Immovable Property FinalDocumento10 pagineValuation Report of Immovable Property FinalSandesh Puppal100% (1)

- Valuation ReportsDocumento28 pagineValuation ReportsRahsia DirikuNessuna valutazione finora

- Bank Appraisal PDFDocumento61 pagineBank Appraisal PDFScott BowermanNessuna valutazione finora

- 2020REIT - Briefer On Philippine REIT PDFDocumento7 pagine2020REIT - Briefer On Philippine REIT PDFN.a. M. TandayagNessuna valutazione finora

- A Comparative Analysis of Rental Variation in Residential and Commercial Properties in NigeriaDocumento64 pagineA Comparative Analysis of Rental Variation in Residential and Commercial Properties in NigeriaRamani Krishnamoorthy100% (1)

- Introduction to Statutory Valuation in MalaysiaDocumento11 pagineIntroduction to Statutory Valuation in MalaysiaQayyumNessuna valutazione finora

- 7 - Market ApproachDocumento22 pagine7 - Market ApproachThresia Navarro LadicaNessuna valutazione finora

- Chapter 6-Income ApproachDocumento37 pagineChapter 6-Income ApproachHosnii QamarNessuna valutazione finora

- Ivsc International Valuation StandardsDocumento23 pagineIvsc International Valuation StandardsCARamachandranMahadeNessuna valutazione finora

- Real Estate DevelopmentDocumento21 pagineReal Estate Developmentkrnitesh41Nessuna valutazione finora

- Proposal For Tenant Representative & Advisory ServicesDocumento12 pagineProposal For Tenant Representative & Advisory Servicesanhnh592Nessuna valutazione finora

- Real - Estate CpdprogramDocumento164 pagineReal - Estate CpdprogramPRC BoardNessuna valutazione finora

- 5 Methods of ValuationDocumento14 pagine5 Methods of Valuationmennakhla100% (1)

- Tpa ProjectDocumento23 pagineTpa ProjectTushar Chowdhary50% (2)

- Real Estate InvestmentsDocumento29 pagineReal Estate InvestmentsKaushal Nahata100% (1)

- Lecture 1 - Introduction To Real Estate EconomicsDocumento7 pagineLecture 1 - Introduction To Real Estate EconomicsCamca BesiNessuna valutazione finora

- Real Property Valuation MethodsDocumento6 pagineReal Property Valuation MethodsMuhammadIqbalMughalNessuna valutazione finora

- Broker Reviewer 2022Documento8 pagineBroker Reviewer 2022Janzel SantillanNessuna valutazione finora

- Arizona Property Management Agreement PDFDocumento4 pagineArizona Property Management Agreement PDFDrake MontgomeryNessuna valutazione finora

- Real Property Valuation FundamentalsDocumento40 pagineReal Property Valuation FundamentalsMelkamu AmusheNessuna valutazione finora

- 1.1 Introduction To Property EconomicsDocumento30 pagine1.1 Introduction To Property EconomicswphammanNessuna valutazione finora

- REITs and InvITsDocumento17 pagineREITs and InvITsSai YvstNessuna valutazione finora

- Market Feasibility Dane ApartmentDocumento4 pagineMarket Feasibility Dane ApartmentGrachel Gabrielle Enriquez0% (1)

- Overview of The Property Development ProcessDocumento5 pagineOverview of The Property Development ProcessAnonymous lV8E5mEO100% (1)

- Real Estate Laws in IndiaDocumento3 pagineReal Estate Laws in Indiarrahuldeshpande9Nessuna valutazione finora

- Valuation Maths (3&4) 15.7.09Documento31 pagineValuation Maths (3&4) 15.7.09Luis AdrianNessuna valutazione finora

- Appraisal Report Lovejoy FehnelDocumento121 pagineAppraisal Report Lovejoy FehnelHoangTruongNessuna valutazione finora

- Property Management NotesDocumento11 pagineProperty Management Notesseleb777Nessuna valutazione finora

- Understand Appraisal 1109 PDFDocumento18 pagineUnderstand Appraisal 1109 PDFrubydelacruzNessuna valutazione finora

- Importance of Highest and Best Use Analysis in Real Estate AppraisalDocumento5 pagineImportance of Highest and Best Use Analysis in Real Estate AppraisalEnp Gus AgostoNessuna valutazione finora

- Valuation ModelsDocumento47 pagineValuation ModelsHamis Rabiam MagundaNessuna valutazione finora

- Valuation of Lease InterestsDocumento30 pagineValuation of Lease InterestsRossvelt DucusinNessuna valutazione finora

- Proposal For Real Estate Asset Management and Brokerage ServicesDocumento2 pagineProposal For Real Estate Asset Management and Brokerage ServicesTed McKinnonNessuna valutazione finora

- Property ValuationDocumento6 pagineProperty Valuationsurendra_pangaNessuna valutazione finora

- Real Estate Consulting AgreementDocumento4 pagineReal Estate Consulting AgreementAnurag GoelNessuna valutazione finora

- Real Estate EconomicsDocumento8 pagineReal Estate EconomicsPushpa BaruaNessuna valutazione finora

- Acquisition Residential Version 4Documento32 pagineAcquisition Residential Version 4Chujja ChuNessuna valutazione finora

- Disposal Residential Version 4Documento19 pagineDisposal Residential Version 4Emmanuel Tolulope AdeniyiNessuna valutazione finora

- Emerging MarketDocumento4 pagineEmerging Marketsv03Nessuna valutazione finora

- IF3206 - Front Cover SheetDocumento9 pagineIF3206 - Front Cover Sheetsv03Nessuna valutazione finora

- Understanding The Business EnvironmenDocumento8 pagineUnderstanding The Business Environmensv03Nessuna valutazione finora

- 1098389Documento1 pagina1098389sv03Nessuna valutazione finora

- Imperial Bank of Canada (TSX: Ry) : Mcclelland May Work at RBC, Yet It'S Not WhyDocumento6 pagineImperial Bank of Canada (TSX: Ry) : Mcclelland May Work at RBC, Yet It'S Not Whysv03Nessuna valutazione finora

- Event and Entertainment ContextDocumento10 pagineEvent and Entertainment Contextsv03Nessuna valutazione finora

- Advanced Marketing StrategyDocumento4 pagineAdvanced Marketing Strategysv03Nessuna valutazione finora

- Capital Budgeting: RUNNING HEAD: Alliant Credit Union and Its Budgeting 1Documento7 pagineCapital Budgeting: RUNNING HEAD: Alliant Credit Union and Its Budgeting 1sv03Nessuna valutazione finora

- Final ExamDocumento5 pagineFinal Examsv03Nessuna valutazione finora

- Acct 3074Documento10 pagineAcct 3074sv03Nessuna valutazione finora

- Movie Assignment: Student NameDocumento8 pagineMovie Assignment: Student Namesv03Nessuna valutazione finora

- Human Resource PoliciesDocumento11 pagineHuman Resource Policiessv03Nessuna valutazione finora

- Question1SolutionsDocumento5 pagineQuestion1Solutionssv03Nessuna valutazione finora

- Ba A Uvoc300919Documento5 pagineBa A Uvoc300919sv03Nessuna valutazione finora

- Ba C Arch310819 DQ3Documento2 pagineBa C Arch310819 DQ3sv03Nessuna valutazione finora

- Cash Budgeting and Fraud Management: Topic 4Documento16 pagineCash Budgeting and Fraud Management: Topic 4sv03Nessuna valutazione finora

- CoC DISS011019Documento2 pagineCoC DISS011019sv03Nessuna valutazione finora

- Favorite Property Analysis Nguyen Hong Hanh - 300272328 November 27, 2017 HOSP 1235-001 Instructor: Anton KosztyoDocumento8 pagineFavorite Property Analysis Nguyen Hong Hanh - 300272328 November 27, 2017 HOSP 1235-001 Instructor: Anton Kosztyosv03Nessuna valutazione finora

- Topic 3: Operational Budgeting and Inventory ManagementDocumento29 pagineTopic 3: Operational Budgeting and Inventory Managementsv03Nessuna valutazione finora

- City Sky Co: Laws Related To The CaseDocumento12 pagineCity Sky Co: Laws Related To The Casesv03Nessuna valutazione finora

- Reworked 1083394 - Heritage AssetsDocumento13 pagineReworked 1083394 - Heritage Assetssv03100% (1)

- Running Head: Financial Analysis and Valuation 1Documento6 pagineRunning Head: Financial Analysis and Valuation 1sv03Nessuna valutazione finora

- Cash Flow Annual SampleDocumento37 pagineCash Flow Annual SampleKSXNessuna valutazione finora

- Hotel Investment DecisionsDocumento20 pagineHotel Investment Decisionssv03Nessuna valutazione finora

- Topic 2: Pricing Decisions in HotelsDocumento28 pagineTopic 2: Pricing Decisions in Hotelssv03Nessuna valutazione finora

- Operational Budgeting and Variance Analysis Topic 5Documento17 pagineOperational Budgeting and Variance Analysis Topic 5sv03Nessuna valutazione finora

- Topic 2: Pricing Decisions in HotelsDocumento28 pagineTopic 2: Pricing Decisions in Hotelssv03Nessuna valutazione finora

- Performance Control Systems and Internal Controls: Topic 1 and Introduction To UnitDocumento24 paginePerformance Control Systems and Internal Controls: Topic 1 and Introduction To Unitsv03Nessuna valutazione finora

- Information Uncertainty and Behavioral eDocumento23 pagineInformation Uncertainty and Behavioral esv03Nessuna valutazione finora

- Csec Poa January 2012 p2Documento9 pagineCsec Poa January 2012 p2Renelle RampersadNessuna valutazione finora

- Corporate Governance - An OverviewDocumento15 pagineCorporate Governance - An OverviewSyed NaseemNessuna valutazione finora

- Project ManagementDocumento43 pagineProject ManagementAwot Haileslassie100% (3)

- Sms 315 Test 2Documento22 pagineSms 315 Test 2Yutaka KomatsuzakiNessuna valutazione finora

- 43 CA CPT Dec 2010 Question Paper With Answer Key 2Documento6 pagine43 CA CPT Dec 2010 Question Paper With Answer Key 2Vishal Gattani100% (1)

- Senior QA Automation EngineerDocumento3 pagineSenior QA Automation EngineerMihaela AvramNessuna valutazione finora

- 221-Article Text-301-1-10-20190822Documento4 pagine221-Article Text-301-1-10-20190822Aviral GuptaNessuna valutazione finora

- Impact of Technology on Restaurant Food Delivery ServicesDocumento26 pagineImpact of Technology on Restaurant Food Delivery ServicesAngelica GementizaNessuna valutazione finora

- Marketing Management Strategies and PlansDocumento39 pagineMarketing Management Strategies and PlansErlita KusumaNessuna valutazione finora

- Chapter 7 PPT Version 2Documento61 pagineChapter 7 PPT Version 2islamasifNessuna valutazione finora

- Learning new skills and applying them to achieve goalsDocumento2 pagineLearning new skills and applying them to achieve goalsbrian njauNessuna valutazione finora

- 5 Desain CVDocumento5 pagine5 Desain CVInda Sela GifariNessuna valutazione finora

- Entrepreneurship CH 6Documento27 pagineEntrepreneurship CH 6AYELENessuna valutazione finora

- Ifrs Inr Press ReleaseDocumento7 pagineIfrs Inr Press ReleaseV KeshavdevNessuna valutazione finora

- Himachal Pradesh Public Service Commission: Advertisement No. 6/5-2023 Dated: 18 May, 2023Documento12 pagineHimachal Pradesh Public Service Commission: Advertisement No. 6/5-2023 Dated: 18 May, 2023AmanNessuna valutazione finora

- Not A Certified Copy: Filing# 141606080 E-Filed 01/07/2022 05:13:19 PMDocumento10 pagineNot A Certified Copy: Filing# 141606080 E-Filed 01/07/2022 05:13:19 PMlarry-612445Nessuna valutazione finora

- TFM SNEL Congo Energy Notification (D&P Comments) (1000782849v1) enDocumento3 pagineTFM SNEL Congo Energy Notification (D&P Comments) (1000782849v1) encefuneslpezNessuna valutazione finora

- Antonakakis Et Al, 2017 - Oil Dependence, Quality of Political Institutions and Economic Growth A Panel VAR ApproachDocumento17 pagineAntonakakis Et Al, 2017 - Oil Dependence, Quality of Political Institutions and Economic Growth A Panel VAR ApproachSlice LeNessuna valutazione finora

- Confidential Term Sheet for $750K Convertible Note OfferingDocumento1 paginaConfidential Term Sheet for $750K Convertible Note OfferingbrentbushnellNessuna valutazione finora

- Add. Add2Documento81 pagineAdd. Add2Shashi RajputNessuna valutazione finora

- Law, Land Tenure and Gender Review: Latin America (Mexico)Documento118 pagineLaw, Land Tenure and Gender Review: Latin America (Mexico)United Nations Human Settlements Programme (UN-HABITAT)Nessuna valutazione finora

- My Notebook Sections and StickersDocumento32 pagineMy Notebook Sections and StickersNikka CamannongNessuna valutazione finora

- DATA PRIVACY CONSENT FORM - NSA Final - v2-1Documento1 paginaDATA PRIVACY CONSENT FORM - NSA Final - v2-1I Love You 3000100% (1)

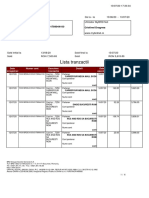

- Lista Tranzactii: Cristinel Dragnea RO81BRDE410SV31789944100 RON Cristinel DragneaDocumento6 pagineLista Tranzactii: Cristinel Dragnea RO81BRDE410SV31789944100 RON Cristinel DragneaSebastian PSNessuna valutazione finora

- Imposto D Renda em Inglês Tax Return - BrancoDocumento5 pagineImposto D Renda em Inglês Tax Return - BrancoAbimaelNessuna valutazione finora

- 3 từ còn lại:: I. NGỮ ÂM: (1 điểm) Chọn từ mà phần phần gạch chân có cách phát âm khác vớiDocumento5 pagine3 từ còn lại:: I. NGỮ ÂM: (1 điểm) Chọn từ mà phần phần gạch chân có cách phát âm khác vớiHương Quỳnh ĐặngNessuna valutazione finora

- SWR Reservation ReportDocumento94 pagineSWR Reservation ReportVasu HarshvardhanNessuna valutazione finora

- Final Report 123Documento64 pagineFinal Report 123habtamu geremewNessuna valutazione finora

- F 12. Sulit V CADocumento2 pagineF 12. Sulit V CAChilzia RojasNessuna valutazione finora

- Seminar 15Documento23 pagineSeminar 15Chann ChannNessuna valutazione finora