Potrebbero piacerti anche

- Gazette Notice - Shedule of Tarrifs For The Supply of Electrical Energy by KPLC PDFDocumento7 pagineGazette Notice - Shedule of Tarrifs For The Supply of Electrical Energy by KPLC PDFgeraldmrkNessuna valutazione finora

- CAK Sector-Statistics-Report-Q2-2019-2020 (Oct - Dec 2019) PDFDocumento24 pagineCAK Sector-Statistics-Report-Q2-2019-2020 (Oct - Dec 2019) PDFgeraldmrkNessuna valutazione finora

- Sector-Statistics-Report-Q2-2018-19 (Oct - Dec 2018) PDFDocumento26 pagineSector-Statistics-Report-Q2-2018-19 (Oct - Dec 2018) PDFgeraldmrkNessuna valutazione finora

- Forecasting Methods - Top 4 Types, Overview, Examples PDFDocumento13 pagineForecasting Methods - Top 4 Types, Overview, Examples PDFgeraldmrkNessuna valutazione finora

- Pearls of Wisdom PankajDocumento2 paginePearls of Wisdom PankajgeraldmrkNessuna valutazione finora

- Diploma in Information Communication Technology (DICT) : Advance Copy - July 2018Documento27 pagineDiploma in Information Communication Technology (DICT) : Advance Copy - July 2018geraldmrkNessuna valutazione finora

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (121)

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Bank Management System: ModulesDocumento2 pagineBank Management System: ModulesSumod SundarNessuna valutazione finora

- Soal Asis Pert 2 - Jordy - PA1Documento1 paginaSoal Asis Pert 2 - Jordy - PA1Jordy TangNessuna valutazione finora

- HDFC Life Guaranteed Income Insurance ( 8 - 16 )Documento2 pagineHDFC Life Guaranteed Income Insurance ( 8 - 16 )AbhishekNessuna valutazione finora

- Topic 5 Accounting For PartnershipsDocumento56 pagineTopic 5 Accounting For Partnershipstwahirwajeanpierre50Nessuna valutazione finora

- Himanshu Draft v1Documento3 pagineHimanshu Draft v1Praddy BrookNessuna valutazione finora

- TTTTTDocumento3 pagineTTTTTManoj KumarNessuna valutazione finora

- WFO V15 2 Genesys Integration With RecorderDocumento97 pagineWFO V15 2 Genesys Integration With RecorderMarcos Antonio100% (1)

- Bauwerk 155822010229 LCDocumento2 pagineBauwerk 155822010229 LCSadid ShahzadNessuna valutazione finora

- 6 Standard STR PresentationDocumento31 pagine6 Standard STR Presentationrajin_rammsteinNessuna valutazione finora

- Case Analysis: Netflix: Pricing Decision 2011: Group 3Documento7 pagineCase Analysis: Netflix: Pricing Decision 2011: Group 3vedant thakreNessuna valutazione finora

- 32 1 PDFDocumento402 pagine32 1 PDFThompsonNessuna valutazione finora

- Saraswat Bank Full & FinalDocumento15 pagineSaraswat Bank Full & FinalPratik RevankarNessuna valutazione finora

- Source: Capitaline Database: Company Long Name Industry Year End Net SalesDocumento9 pagineSource: Capitaline Database: Company Long Name Industry Year End Net SalesMadhuram SharmaNessuna valutazione finora

- Professional English For Students of Logistics PDFDocumento187 pagineProfessional English For Students of Logistics PDFbibaNessuna valutazione finora

- Hotel E-Voucher - Order ID 1010067682Documento1 paginaHotel E-Voucher - Order ID 1010067682putri sri nirmala putriNessuna valutazione finora

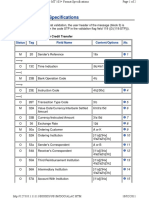

- MT 103+ Format Specifications: MT 103+ Single Customer Credit TransferDocumento2 pagineMT 103+ Format Specifications: MT 103+ Single Customer Credit Transferme Nader100% (1)

- Customer Pref. Towards Services Provided by HDFC BankDocumento67 pagineCustomer Pref. Towards Services Provided by HDFC BankAnonymous AXSx3vtPNessuna valutazione finora

- Corporate and Retail BankingDocumento13 pagineCorporate and Retail Bankingbipin kumarNessuna valutazione finora

- Personal Loan PDFDocumento3 paginePersonal Loan PDFbusiness loanNessuna valutazione finora

- Tera Romm 4Documento6 pagineTera Romm 4Temp TNessuna valutazione finora

- Intermediate Group I Test Papers FOR 2014 DECDocumento88 pagineIntermediate Group I Test Papers FOR 2014 DECwaterloveNessuna valutazione finora

- New Mail (30) 2 PDFDocumento6 pagineNew Mail (30) 2 PDFWilliam SimonNessuna valutazione finora

- 1.arrivals Summary ReportDocumento2 pagine1.arrivals Summary ReportmoisesNessuna valutazione finora

- GCP TutorialDocumento36 pagineGCP TutorialSandeep BharadwajNessuna valutazione finora

- Journal March 2012: The British Chapter of Aida, The International Association For Insurance LawDocumento96 pagineJournal March 2012: The British Chapter of Aida, The International Association For Insurance Lawmilica997Nessuna valutazione finora

- E Business Strategy Chaffey 2Documento24 pagineE Business Strategy Chaffey 2diyanaNessuna valutazione finora

- What Are Mutual FundsDocumento12 pagineWhat Are Mutual FundsSuraj00sNessuna valutazione finora

- Naukri ATULKUMARJAIN (26y 0m)Documento3 pagineNaukri ATULKUMARJAIN (26y 0m)emailbbishtNessuna valutazione finora

- Telemedicine According To WHO, Telemedicine Is Defined Advantages of Telemedicine Model of Telehealth SystemDocumento2 pagineTelemedicine According To WHO, Telemedicine Is Defined Advantages of Telemedicine Model of Telehealth SystemAmanda ScarletNessuna valutazione finora

- BHN Ajar Samone Equipment Repair Inc - PreparationDocumento29 pagineBHN Ajar Samone Equipment Repair Inc - PreparationfghhjjjnjjnNessuna valutazione finora