Potrebbero piacerti anche

- Airbus Global Market Forecast 2013-2032Documento63 pagineAirbus Global Market Forecast 2013-2032ArturoNessuna valutazione finora

- The Evolution of Yield Management in the Airline Industry: Origins to the Last FrontierDa EverandThe Evolution of Yield Management in the Airline Industry: Origins to the Last FrontierNessuna valutazione finora

- Unparalleled Advantage: Opening Routes & Exploring Potential MarketsDocumento60 pagineUnparalleled Advantage: Opening Routes & Exploring Potential MarketsRobertas NegudinasNessuna valutazione finora

- Bcom Industry Report-2Documento7 pagineBcom Industry Report-2api-638731062Nessuna valutazione finora

- Aerospace GlobalReport 2011Documento24 pagineAerospace GlobalReport 2011subbotNessuna valutazione finora

- Airports of The World - May-June 2020 PDFDocumento86 pagineAirports of The World - May-June 2020 PDFV DNessuna valutazione finora

- Air Passenger Forecasts: Global ReportDocumento4 pagineAir Passenger Forecasts: Global ReportAadil KhanNessuna valutazione finora

- The-Star - co.ke-KQs Survival Strategy As Global Travel ResumesDocumento8 pagineThe-Star - co.ke-KQs Survival Strategy As Global Travel ResumesJunior Mebude SimbaNessuna valutazione finora

- LCC DensityDocumento13 pagineLCC Densityskyline_001Nessuna valutazione finora

- Flight International - Tails of The Unexpected (May 27, 2014)Documento54 pagineFlight International - Tails of The Unexpected (May 27, 2014)นาถวัฒน์ ฉลาดแย้มNessuna valutazione finora

- G11 Economics Student HandbookDocumento20 pagineG11 Economics Student HandbookAnand KumarNessuna valutazione finora

- Airbus GMF Booklet 2014-2033 01Documento49 pagineAirbus GMF Booklet 2014-2033 01oukast_23Nessuna valutazione finora

- Global FLeet and MRO Market Forecast 2021-2031Documento58 pagineGlobal FLeet and MRO Market Forecast 2021-2031rachid mouchaouche100% (1)

- Global Business Travel Magazine May June 2013Documento44 pagineGlobal Business Travel Magazine May June 2013haloheruNessuna valutazione finora

- Industry ReportDocumento10 pagineIndustry Reportapi-545824706Nessuna valutazione finora

- AirFreight Cargo ForwardingDocumento46 pagineAirFreight Cargo Forwardingmrprasad2k1100% (1)

- Speech by Willie WalshDocumento28 pagineSpeech by Willie Walshrgovindan123Nessuna valutazione finora

- Gourdin CHPT 1Documento32 pagineGourdin CHPT 1CharleneKronstedtNessuna valutazione finora

- You're Grounded - The COVID-19 Effect On Flight CapacityDocumento8 pagineYou're Grounded - The COVID-19 Effect On Flight Capacitypushp ranajnNessuna valutazione finora

- Questions 1 To 120 1Documento123 pagineQuestions 1 To 120 1Alc 2016Nessuna valutazione finora

- Analysis of The Effect of COVID-19 On The Stock Market and Potential Investing StrategiesDocumento17 pagineAnalysis of The Effect of COVID-19 On The Stock Market and Potential Investing StrategiesszaszaszNessuna valutazione finora

- Airline Leader - Issue 15Documento91 pagineAirline Leader - Issue 15capanaoNessuna valutazione finora

- How Has Covid-19 Impacted The Aviation IndustryDocumento8 pagineHow Has Covid-19 Impacted The Aviation Industryapi-653065309Nessuna valutazione finora

- Source: Adapted From The World's Richest Billionaires, Forbes, 2008Documento5 pagineSource: Adapted From The World's Richest Billionaires, Forbes, 2008angel_113Nessuna valutazione finora

- DVB Overview of Commercial Aircraft 2018 2019Documento49 pagineDVB Overview of Commercial Aircraft 2018 2019chand198Nessuna valutazione finora

- 2013-Q4 Ascend V1ewpoint (Issue 41)Documento16 pagine2013-Q4 Ascend V1ewpoint (Issue 41)awang90Nessuna valutazione finora

- Components:: Supply & RepairDocumento31 pagineComponents:: Supply & RepairrusdiNessuna valutazione finora

- American Airlines Conf TranscriptDocumento15 pagineAmerican Airlines Conf TranscriptzaptheimpalerNessuna valutazione finora

- Business EnvironmentDocumento10 pagineBusiness EnvironmentSanjana TasmiaNessuna valutazione finora

- Favorite Airline Were Far From Over. The Interview Took Place Three Days Before The FirstDocumento2 pagineFavorite Airline Were Far From Over. The Interview Took Place Three Days Before The Firstdrlov_20037767Nessuna valutazione finora

- HE Uroavia EWS: MARCH 2011Documento36 pagineHE Uroavia EWS: MARCH 2011Diana ScodreanuNessuna valutazione finora

- United Continental Holdings 2011Documento52 pagineUnited Continental Holdings 2011helmyirwanNessuna valutazione finora

- British Airways - EditedDocumento17 pagineBritish Airways - EditedMunabi AshleyNessuna valutazione finora

- Business Insider March 2020 PDFDocumento118 pagineBusiness Insider March 2020 PDFMoldovan OvidiuNessuna valutazione finora

- BEAV Q312 TranscriptDocumento16 pagineBEAV Q312 TranscriptcasefortrilsNessuna valutazione finora

- 2018-2028 Global Fleet MRO Market Forecast Commentary Public Final WebDocumento51 pagine2018-2028 Global Fleet MRO Market Forecast Commentary Public Final WebOmar A TavarezNessuna valutazione finora

- 2018-2028 Global Fleet MRO Market Forecast Commentary Public Final WebDocumento51 pagine2018-2028 Global Fleet MRO Market Forecast Commentary Public Final WebPraveen100% (1)

- WarnockSmith DDocumento3 pagineWarnockSmith DRicky RizaldiNessuna valutazione finora

- MKTG 6650 - Individual AssignmentDocumento14 pagineMKTG 6650 - Individual AssignmentShehriyar AhmedNessuna valutazione finora

- The Industry Handbook: The Airline Industry: Printer Friendly Version (PDF Format)Documento21 pagineThe Industry Handbook: The Airline Industry: Printer Friendly Version (PDF Format)Gaurav JainNessuna valutazione finora

- 2006 InterVISTASDocumento139 pagine2006 InterVISTASKatiaNessuna valutazione finora

- Bombardier Aerospace 20140717 Commercial Aircraft Market Forecast 2014 33Documento43 pagineBombardier Aerospace 20140717 Commercial Aircraft Market Forecast 2014 33Mostafi RashelNessuna valutazione finora

- Discrete Prob Practice QsDocumento8 pagineDiscrete Prob Practice QsAitzul SchkohNessuna valutazione finora

- Vintage Airplane - Mar 2007Documento44 pagineVintage Airplane - Mar 2007Aviation/Space History LibraryNessuna valutazione finora

- Critical Analysis OF Irbus External Macro Context UsingDocumento15 pagineCritical Analysis OF Irbus External Macro Context UsingAndres morenoNessuna valutazione finora

- Grouping Assignment Lte135Documento42 pagineGrouping Assignment Lte135NOOR HANAFI ABDUL AZIZNessuna valutazione finora

- The 10 Stocks To Avoid During The Coronavirus Pandemic Tkc442Documento8 pagineThe 10 Stocks To Avoid During The Coronavirus Pandemic Tkc442Dorene CashNessuna valutazione finora

- Air Transportation 2. Civil Aviation and Activity SpacesDocumento42 pagineAir Transportation 2. Civil Aviation and Activity SpacesXavier LeroyNessuna valutazione finora

- 2020 Airline Insights ReviewDocumento70 pagine2020 Airline Insights ReviewSatrio AditomoNessuna valutazione finora

- Aircraft Interiors International - Show - Case 2024Documento96 pagineAircraft Interiors International - Show - Case 2024Carlos PanaoNessuna valutazione finora

- Aviation Strategy: The Dawn of A Golden Age?Documento24 pagineAviation Strategy: The Dawn of A Golden Age?JamesNessuna valutazione finora

- Aircraft Records Technician Assignment 1Documento16 pagineAircraft Records Technician Assignment 1Mohamad Hazwan Mohamad JanaiNessuna valutazione finora

- Boeing Current Market Outlook 2010 To 2029Documento36 pagineBoeing Current Market Outlook 2010 To 2029pasqconteNessuna valutazione finora

- Very Low Accident Rates: Cswe IiiDocumento4 pagineVery Low Accident Rates: Cswe IiiSiobhan ConnollyNessuna valutazione finora

- The Future of Air Travel ReportDocumento78 pagineThe Future of Air Travel ReportNicole VelasquezNessuna valutazione finora

- Group Assignment Opm554 Nbo4b Group 5Documento24 pagineGroup Assignment Opm554 Nbo4b Group 5Afiq Najmi RosmanNessuna valutazione finora

- Logistics Management Air and Sea 1 4Documento86 pagineLogistics Management Air and Sea 1 4Jibin SamuelNessuna valutazione finora

- ACI Project May, 09Documento14 pagineACI Project May, 09aryan295Nessuna valutazione finora

- CRITICAL REVIEW of AirlineDocumento5 pagineCRITICAL REVIEW of AirlineSakshi PokhriyalNessuna valutazione finora

- 340 FCOM-3 Rev32 2009Documento1.246 pagine340 FCOM-3 Rev32 2009campomarzoNessuna valutazione finora

- A340 Flight Deck and Systems Briefing For PilotsDocumento211 pagineA340 Flight Deck and Systems Briefing For PilotsMa JoNessuna valutazione finora

- 340 FCOM-4 Rev22 2009Documento533 pagine340 FCOM-4 Rev22 2009campomarzoNessuna valutazione finora

- 340 FCOM-2 Rev31 2009Documento750 pagine340 FCOM-2 Rev31 2009campomarzoNessuna valutazione finora

- 340 FCOM-1 Rev27 2009Documento1.200 pagine340 FCOM-1 Rev27 2009campomarzoNessuna valutazione finora

- EASA CFM56 5Band5C Series EnginesDocumento14 pagineEASA CFM56 5Band5C Series EnginescampomarzoNessuna valutazione finora

- A340 Low Visibility OperationDocumento8 pagineA340 Low Visibility OperationPunthep Punnotok100% (1)

- 340 All PanelsDocumento1 pagina340 All PanelscampomarzoNessuna valutazione finora

- Airbus Abbreviations A320 AircraftDocumento193 pagineAirbus Abbreviations A320 AircraftRavindra Sampath Dayarathna85% (13)

- Airbus Abbreviations A320 AircraftDocumento193 pagineAirbus Abbreviations A320 AircraftRavindra Sampath Dayarathna85% (13)

- Speed Tape Airbus - Descent & ArrivalDocumento4 pagineSpeed Tape Airbus - Descent & Arrivalapi-3805097100% (29)

- A340 Flight Deck and Systems Briefing For PilotsDocumento211 pagineA340 Flight Deck and Systems Briefing For PilotsMa JoNessuna valutazione finora

- Kyk Over Al June - 1948 vl2 n7Documento60 pagineKyk Over Al June - 1948 vl2 n7Armando Vázquez CarrilloNessuna valutazione finora

- Para Oficina de Oir 04-Noviembre-2019: Marca Modelo Serie B.H.P. Combustible Tipo Fecha DE Fabricacion InstalacionDocumento49 paginePara Oficina de Oir 04-Noviembre-2019: Marca Modelo Serie B.H.P. Combustible Tipo Fecha DE Fabricacion InstalacionLuis FinquinNessuna valutazione finora

- Economic Growth and Human DevelopmentDocumento48 pagineEconomic Growth and Human DevelopmentTHORIQ ADHARIARDINessuna valutazione finora

- Belapur Housing CCDocumento7 pagineBelapur Housing CCManasviJindal89% (9)

- Indian Acetyls Market OverviewDocumento24 pagineIndian Acetyls Market OverviewPrakrutiShahNessuna valutazione finora

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocumento4 pagineStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancepavans25Nessuna valutazione finora

- Dr. Somdeep Chatterjee Extn: 2028 M-105, NAB: Somdeep@iimcal - Ac.inDocumento30 pagineDr. Somdeep Chatterjee Extn: 2028 M-105, NAB: Somdeep@iimcal - Ac.inV SURENDAR NAIKNessuna valutazione finora

- 122333Documento2 pagine122333Carla Mae F. DaduralNessuna valutazione finora

- Eurocontrol Lssip 2022 Bosnia HerzegovinaDocumento133 pagineEurocontrol Lssip 2022 Bosnia HerzegovinaDeniNessuna valutazione finora

- Ramos - Value and Price of Production. New Evidence On Marx's Transformation Procedure.1999Documento16 pagineRamos - Value and Price of Production. New Evidence On Marx's Transformation Procedure.1999Alejandro RamosNessuna valutazione finora

- Admission ChallanDocumento2 pagineAdmission ChallanBorn TalentedNessuna valutazione finora

- Investment Analysis and Portfolio Management: Question: Explain TheDocumento4 pagineInvestment Analysis and Portfolio Management: Question: Explain TheMo ToNessuna valutazione finora

- WKU, CET, HWRE: Engineering Economics Final Exam 2022Documento1 paginaWKU, CET, HWRE: Engineering Economics Final Exam 2022Bedassa DessalegnNessuna valutazione finora

- PDF Applied Economics Module 4Documento34 paginePDF Applied Economics Module 4Raiza CabreraNessuna valutazione finora

- 0962燃气管道布置qme 00 g 141b 000 Ei 172 en d Piping Arrangement Gas Turbine(121t7058)0962Documento10 pagine0962燃气管道布置qme 00 g 141b 000 Ei 172 en d Piping Arrangement Gas Turbine(121t7058)0962ALAMGIR HOSSAINNessuna valutazione finora

- IE WRITING - TASK 1 Poverty Rates Bar GraphDocumento13 pagineIE WRITING - TASK 1 Poverty Rates Bar Graphhiep huyNessuna valutazione finora

- Ffa08 - g08 - en (Connecting Fittings)Documento118 pagineFfa08 - g08 - en (Connecting Fittings)GetziNessuna valutazione finora

- Bachelor Degree in Wildlife ManagementDocumento10 pagineBachelor Degree in Wildlife ManagementSimon PargasNessuna valutazione finora

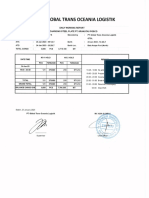

- DWR - Asia Glory 6 - Gtol PDFDocumento9 pagineDWR - Asia Glory 6 - Gtol PDFRahmat HidayatNessuna valutazione finora

- Srilankan Share MarketDocumento35 pagineSrilankan Share MarketSivaratnam Navatharan100% (1)

- Topic 2-Economics ModelsDocumento17 pagineTopic 2-Economics ModelsAbid RanaNessuna valutazione finora

- Consumer Behavior PDFDocumento16 pagineConsumer Behavior PDFowaisNessuna valutazione finora

- An Introduction To Marxism - Its Origins, Key Ideas, and Contemporary RelevanceDocumento2 pagineAn Introduction To Marxism - Its Origins, Key Ideas, and Contemporary RelevancemikeNessuna valutazione finora

- Edexcel GCE History A World Divided Superpower Relations Unit 3 PDFDocumento225 pagineEdexcel GCE History A World Divided Superpower Relations Unit 3 PDFJK67% (3)

- Maruti SuzukiDocumento4 pagineMaruti SuzukihukaNessuna valutazione finora

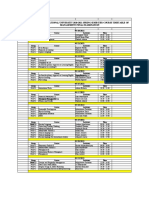

- Ala-Too International University 2020-2021 Spring Semester Course Timetable of Management Final ExaminationDocumento8 pagineAla-Too International University 2020-2021 Spring Semester Course Timetable of Management Final ExaminationKunduz IbraevaNessuna valutazione finora

- Chapter 14Documento34 pagineChapter 14Pháp NguyễnNessuna valutazione finora

- FULL Download Ebook PDF Issues in Economics Today 9th Edition by Robert Guell PDF EbookDocumento41 pagineFULL Download Ebook PDF Issues in Economics Today 9th Edition by Robert Guell PDF Ebookanthony.mckinley501100% (30)

- 014-Din en 1503 2001 001 Steels Specified in European StandardsDocumento9 pagine014-Din en 1503 2001 001 Steels Specified in European StandardsQuality MSIPLNessuna valutazione finora

- Wolf Principles BookDocumento165 pagineWolf Principles BookSarmad AsadNessuna valutazione finora

- CUNY Proficiency Examination (CPE): Passbooks Study GuideDa EverandCUNY Proficiency Examination (CPE): Passbooks Study GuideNessuna valutazione finora

- Drilling Supervisor: Passbooks Study GuideDa EverandDrilling Supervisor: Passbooks Study GuideNessuna valutazione finora

- Master the Boards USMLE Step 2 CK, Seventh EditionDa EverandMaster the Boards USMLE Step 2 CK, Seventh EditionNessuna valutazione finora

- Certified Professional Coder (CPC): Passbooks Study GuideDa EverandCertified Professional Coder (CPC): Passbooks Study GuideValutazione: 5 su 5 stelle5/5 (1)

- Clinical Internal Medicine Review 2023: For USMLE Step 2 CK and COMLEX-USA Level 2Da EverandClinical Internal Medicine Review 2023: For USMLE Step 2 CK and COMLEX-USA Level 2Valutazione: 3 su 5 stelle3/5 (1)

- Preclinical Pathology Review 2023: For USMLE Step 1 and COMLEX-USA Level 1Da EverandPreclinical Pathology Review 2023: For USMLE Step 1 and COMLEX-USA Level 1Valutazione: 5 su 5 stelle5/5 (1)

- ASVAB Flashcards, Fourth Edition: Up-to-date PracticeDa EverandASVAB Flashcards, Fourth Edition: Up-to-date PracticeNessuna valutazione finora

- LMSW Passing Score: Your Comprehensive Guide to the ASWB Social Work Licensing ExamDa EverandLMSW Passing Score: Your Comprehensive Guide to the ASWB Social Work Licensing ExamValutazione: 5 su 5 stelle5/5 (1)

- Outliers by Malcolm Gladwell - Book Summary: The Story of SuccessDa EverandOutliers by Malcolm Gladwell - Book Summary: The Story of SuccessValutazione: 4.5 su 5 stelle4.5/5 (17)

- Medical Terminology For Health Professions 4.0: Ultimate Complete Guide to Pass Various Tests Such as the NCLEX, MCAT, PCAT, PAX, CEN (Nursing), EMT (Paramedics), PANCE (Physician Assistants) And Many Others Test Taken by Students in the Medical FieldDa EverandMedical Terminology For Health Professions 4.0: Ultimate Complete Guide to Pass Various Tests Such as the NCLEX, MCAT, PCAT, PAX, CEN (Nursing), EMT (Paramedics), PANCE (Physician Assistants) And Many Others Test Taken by Students in the Medical FieldValutazione: 4.5 su 5 stelle4.5/5 (2)

- 1,001 Questions & Answers for the CWI Exam: Welding Metallurgy and Visual Inspection Study GuideDa Everand1,001 Questions & Answers for the CWI Exam: Welding Metallurgy and Visual Inspection Study GuideValutazione: 3.5 su 5 stelle3.5/5 (7)

- The NCLEX-RN Exam Study Guide: Premium Edition: Proven Methods to Pass the NCLEX-RN Examination with Confidence – Extensive Next Generation NCLEX (NGN) Practice Test Questions with AnswersDa EverandThe NCLEX-RN Exam Study Guide: Premium Edition: Proven Methods to Pass the NCLEX-RN Examination with Confidence – Extensive Next Generation NCLEX (NGN) Practice Test Questions with AnswersNessuna valutazione finora

- EMT (Emergency Medical Technician) Crash Course with Online Practice Test, 2nd Edition: Get a Passing Score in Less TimeDa EverandEMT (Emergency Medical Technician) Crash Course with Online Practice Test, 2nd Edition: Get a Passing Score in Less TimeValutazione: 3.5 su 5 stelle3.5/5 (3)

- College Level Anatomy and Physiology: Essential Knowledge for Healthcare Students, Professionals, and Caregivers Preparing for Nursing Exams, Board Certifications, and BeyondDa EverandCollege Level Anatomy and Physiology: Essential Knowledge for Healthcare Students, Professionals, and Caregivers Preparing for Nursing Exams, Board Certifications, and BeyondNessuna valutazione finora

- Check Your English Vocabulary for TOEFL: Essential words and phrases to help you maximise your TOEFL scoreDa EverandCheck Your English Vocabulary for TOEFL: Essential words and phrases to help you maximise your TOEFL scoreValutazione: 5 su 5 stelle5/5 (1)

- Nursing School Entrance Exams: HESI A2 / NLN PAX-RN / PSB-RN / RNEE / TEASDa EverandNursing School Entrance Exams: HESI A2 / NLN PAX-RN / PSB-RN / RNEE / TEASNessuna valutazione finora

- Improve Your Global Business English: The Essential Toolkit for Writing and Communicating Across BordersDa EverandImprove Your Global Business English: The Essential Toolkit for Writing and Communicating Across BordersValutazione: 4 su 5 stelle4/5 (14)

- ABSTRACT REASONING / SPATIAL RELATIONS: Passbooks Study GuideDa EverandABSTRACT REASONING / SPATIAL RELATIONS: Passbooks Study GuideValutazione: 5 su 5 stelle5/5 (1)

- The CompTIA Network+ & Security+ Certification: 2 in 1 Book- Simplified Study Guide Eighth Edition (Exam N10-008) | The Complete Exam Prep with Practice Tests and Insider Tips & Tricks | Achieve a 98% Pass Rate on Your First Attempt!Da EverandThe CompTIA Network+ & Security+ Certification: 2 in 1 Book- Simplified Study Guide Eighth Edition (Exam N10-008) | The Complete Exam Prep with Practice Tests and Insider Tips & Tricks | Achieve a 98% Pass Rate on Your First Attempt!Nessuna valutazione finora

- The Official U.S. Army Survival Guide: Updated Edition: FM 30-05.70 (FM 21-76)Da EverandThe Official U.S. Army Survival Guide: Updated Edition: FM 30-05.70 (FM 21-76)Valutazione: 4 su 5 stelle4/5 (1)

- Airplane Flying Handbook: FAA-H-8083-3C (2024)Da EverandAirplane Flying Handbook: FAA-H-8083-3C (2024)Valutazione: 4 su 5 stelle4/5 (12)

- NASM CPT Study Guide 2024-2025: Review Book with 360 Practice Questions and Answer Explanations for the Certified Personal Trainer ExamDa EverandNASM CPT Study Guide 2024-2025: Review Book with 360 Practice Questions and Answer Explanations for the Certified Personal Trainer ExamNessuna valutazione finora

- The Science of Self-Discipline: The Willpower, Mental Toughness, and Self-Control to Resist Temptation and Achieve Your GoalsDa EverandThe Science of Self-Discipline: The Willpower, Mental Toughness, and Self-Control to Resist Temptation and Achieve Your GoalsValutazione: 4.5 su 5 stelle4.5/5 (77)