Potrebbero piacerti anche

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsDa EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNessuna valutazione finora

- Manufacturing Company BudgetingDocumento10 pagineManufacturing Company BudgetingSajakul SornNessuna valutazione finora

- Master BudgetDocumento12 pagineMaster Budgetshi shiiisshhNessuna valutazione finora

- Chapter Two: Master Budget and Responsibility AccountingDocumento25 pagineChapter Two: Master Budget and Responsibility Accountingweyn deguNessuna valutazione finora

- Budgeting Basics and Responsibility AccountingDocumento12 pagineBudgeting Basics and Responsibility AccountingkirosNessuna valutazione finora

- Budget Format Sales Budget: Cash Collection Total Budgeted SalesDocumento6 pagineBudget Format Sales Budget: Cash Collection Total Budgeted Salessernhaow_658673991Nessuna valutazione finora

- Purposes of Budgeting Systems: BudgetDocumento42 paginePurposes of Budgeting Systems: BudgetJohn Joseph CambaNessuna valutazione finora

- Master BudgetingDocumento20 pagineMaster Budgetingjoinme2dayNessuna valutazione finora

- Profit Planning, Activity-Based Budgeting and E-Budgeting: Mcgraw-Hill/IrwinDocumento78 pagineProfit Planning, Activity-Based Budgeting and E-Budgeting: Mcgraw-Hill/IrwinSi HarisNessuna valutazione finora

- Material BudgetDocumento37 pagineMaterial BudgetRahul SardaNessuna valutazione finora

- Cost II (Chapter-Two)Documento48 pagineCost II (Chapter-Two)SemiraNessuna valutazione finora

- Treasury Management Vs Cash Management Answer To Warm Up ExercisesDocumento8 pagineTreasury Management Vs Cash Management Answer To Warm Up Exercisesephraim0% (1)

- Questions On Cash Budget-2Documento7 pagineQuestions On Cash Budget-2Mpolokeng HlabanaNessuna valutazione finora

- Budgeting Module - Sales, Production, Materials & Labor CostsDocumento9 pagineBudgeting Module - Sales, Production, Materials & Labor CostsAndrea Lyn Salonga CacayNessuna valutazione finora

- Financial Forecasting: Production Requirements (LO2) Sales For Western Boot Stores Are Expected To Be 40,000Documento13 pagineFinancial Forecasting: Production Requirements (LO2) Sales For Western Boot Stores Are Expected To Be 40,000Juliet Dorado100% (1)

- CH 10 BudgetingDocumento83 pagineCH 10 BudgetingShannon BánañasNessuna valutazione finora

- Proj 2Documento15 pagineProj 2Shahan AsifNessuna valutazione finora

- Quiz 3.1 BudgetingDocumento6 pagineQuiz 3.1 BudgetingMaxine ConstantinoNessuna valutazione finora

- MASTER-BUDGETDocumento36 pagineMASTER-BUDGETRafols AnnabelleNessuna valutazione finora

- April May June Quarter Product: 1 Budgeted Sales (Units) Selling Price Per Unit Total RevenueDocumento18 pagineApril May June Quarter Product: 1 Budgeted Sales (Units) Selling Price Per Unit Total Revenueyonna anggrelinaNessuna valutazione finora

- Boomstick Corp quarterly budgets and financial statementsDocumento14 pagineBoomstick Corp quarterly budgets and financial statementsDivya GoyalNessuna valutazione finora

- BudgetingDocumento74 pagineBudgetingRevathi AnandNessuna valutazione finora

- Chap07 Rev. FI5 Ex PRDocumento11 pagineChap07 Rev. FI5 Ex PRKhryzha Hanne Dela CruzNessuna valutazione finora

- Budgetary ControlDocumento5 pagineBudgetary ControlJasdeep Singh DeepuNessuna valutazione finora

- Cost Accounting Assignment #2Documento5 pagineCost Accounting Assignment #2BRIANNIE ASRI VIVASNessuna valutazione finora

- Exercises 7A1 and 7B1: Book: Administrative AccountingDocumento9 pagineExercises 7A1 and 7B1: Book: Administrative AccountingScribdTranslationsNessuna valutazione finora

- Seminar 11answer Group 11Documento115 pagineSeminar 11answer Group 11Shweta SridharNessuna valutazione finora

- Scenario Roletter Company Budgets For The Five Months 2007 Particulars Jan Feb Mar Apr MayDocumento11 pagineScenario Roletter Company Budgets For The Five Months 2007 Particulars Jan Feb Mar Apr MayajithsubramanianNessuna valutazione finora

- Case 8-31: April May June QuarterDocumento2 pagineCase 8-31: April May June QuarterileviejoieNessuna valutazione finora

- BudgetingDocumento130 pagineBudgetingRevathi AnandNessuna valutazione finora

- Ulod. Describe The Budgeting Framework and Develop A Master BudgetDocumento3 pagineUlod. Describe The Budgeting Framework and Develop A Master BudgetJeson MalinaoNessuna valutazione finora

- Mid Term Exam - MBA - Management Accounting - MBAT 202 - OnlineDocumento2 pagineMid Term Exam - MBA - Management Accounting - MBAT 202 - OnlineDullStar MOTONessuna valutazione finora

- 6486 Chap008 PDFDocumento17 pagine6486 Chap008 PDFDheaNessuna valutazione finora

- RF Ltd Cash BudgetDocumento26 pagineRF Ltd Cash BudgetRiaz Baloch Notezai100% (1)

- Acctg 202Documento9 pagineAcctg 202Lore Desa CenizaNessuna valutazione finora

- Quarterly Budget Report for Royal CompanyDocumento15 pagineQuarterly Budget Report for Royal CompanyMaeNessuna valutazione finora

- THE FOUNDATIONAL 15Documento8 pagineTHE FOUNDATIONAL 15Shafa AlyaNessuna valutazione finora

- Master budget planning and control for trading and manufacturing concernsDocumento14 pagineMaster budget planning and control for trading and manufacturing concernsJigoku ShojuNessuna valutazione finora

- Financial and Management and Accouting MBA0041 Assingment FALL 2014 LC-02009 Name: Nandeshwar Singh ROLL NO.1408001255Documento7 pagineFinancial and Management and Accouting MBA0041 Assingment FALL 2014 LC-02009 Name: Nandeshwar Singh ROLL NO.1408001255Nageshwar singhNessuna valutazione finora

- Excalibur Company sales budget and material requirements analysisDocumento6 pagineExcalibur Company sales budget and material requirements analysisMaxine ConstantinoNessuna valutazione finora

- Kế Toán Quản Trị Chương 3Documento41 pagineKế Toán Quản Trị Chương 3Nhựt AnhNessuna valutazione finora

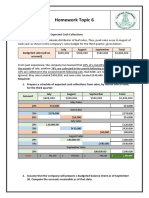

- Homework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionsDocumento3 pagineHomework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionskhetamNessuna valutazione finora

- Budgeting Problems PDFDocumento5 pagineBudgeting Problems PDFER Aditya DasNessuna valutazione finora

- Brewer8e GEs PPT Chapter 8 UpdDocumento22 pagineBrewer8e GEs PPT Chapter 8 UpdNguyễn Ngọc Quỳnh TiênNessuna valutazione finora

- Chap7vanderbeck ReviewerDocumento8 pagineChap7vanderbeck ReviewerSaeym SegoviaNessuna valutazione finora

- Financial Planning Tools and Concepts: Lesson 3Documento21 pagineFinancial Planning Tools and Concepts: Lesson 3chacha caberNessuna valutazione finora

- Master Budgeting (Sample Problems With Answers)Documento11 pagineMaster Budgeting (Sample Problems With Answers)Jonalyn TaboNessuna valutazione finora

- Profit planning and control budgetsDocumento13 pagineProfit planning and control budgetsMadhav RajbanshiNessuna valutazione finora

- Budgeting - 1Documento3 pagineBudgeting - 1Muhammad MansoorNessuna valutazione finora

- Case StudiesDocumento6 pagineCase StudiesFrancesnova B. Dela PeñaNessuna valutazione finora

- Case Analysis (1 30)Documento3 pagineCase Analysis (1 30)manishadaaNessuna valutazione finora

- ACFrOgAMXLJQ31ib6NhLGI0LJ g6GJ517KX03aMrtqxVEqeGBZVYeNyhJHHN9 NBC Vi fXXpyOSGJRyPbtkRLA5DID6 - WJh7xyy7T4 - lcWF9qvk7GWZbEblGKEapUTdWZQyBqXGaUpCDjeEy - FVDocumento6 pagineACFrOgAMXLJQ31ib6NhLGI0LJ g6GJ517KX03aMrtqxVEqeGBZVYeNyhJHHN9 NBC Vi fXXpyOSGJRyPbtkRLA5DID6 - WJh7xyy7T4 - lcWF9qvk7GWZbEblGKEapUTdWZQyBqXGaUpCDjeEy - FVmy VinayNessuna valutazione finora

- Cash Management QuestionsDocumento5 pagineCash Management QuestionsManasi Jamsandekar100% (1)

- Master Budget TemplateDocumento19 pagineMaster Budget TemplateSanie Hizkia Hendrik MendeNessuna valutazione finora

- Budget and Budgetary Control - Mba Ca. Asim K. Biswas: Question # 1Documento7 pagineBudget and Budgetary Control - Mba Ca. Asim K. Biswas: Question # 1Suraj KumarNessuna valutazione finora

- Chap07 Rev. FI5 Ex PR 1Documento10 pagineChap07 Rev. FI5 Ex PR 1Beyond ThatNessuna valutazione finora

- Operating Budget DiscussionDocumento3 pagineOperating Budget DiscussionDavin DavinNessuna valutazione finora

- Bud GettingDocumento8 pagineBud GettingLorena Mae LasquiteNessuna valutazione finora

- Ca Ipcc Costing and Financial Management Suggested Answers May 2015Documento20 pagineCa Ipcc Costing and Financial Management Suggested Answers May 2015Prasanna KumarNessuna valutazione finora

- FinalaccountingprojectDocumento14 pagineFinalaccountingprojectapi-242856546Nessuna valutazione finora

- Mrunal Economy Handouts PCB8 2023-24Documento901 pagineMrunal Economy Handouts PCB8 2023-24Adharsh Surendhiran100% (3)

- Westmont Bank VS Dela Rosa-RamosDocumento2 pagineWestmont Bank VS Dela Rosa-RamosCandelaria QuezonNessuna valutazione finora

- Understanding Credit Agreement Basics: Deals & FacilitiesDocumento36 pagineUnderstanding Credit Agreement Basics: Deals & FacilitiesJonathan RandallNessuna valutazione finora

- CV - Divya GoyalDocumento1 paginaCV - Divya GoyalGarima JainNessuna valutazione finora

- NC-III Bookkeeping Reviewer NC-III Bookkeeping ReviewerDocumento34 pagineNC-III Bookkeeping Reviewer NC-III Bookkeeping ReviewerSheila Mae Lira100% (2)

- T-Accounts E. Tria Systems ConsultantDocumento8 pagineT-Accounts E. Tria Systems ConsultantAnya DaniellaNessuna valutazione finora

- Chapter 11 Walter Nicholson Microcenomic TheoryDocumento15 pagineChapter 11 Walter Nicholson Microcenomic TheoryUmair QaziNessuna valutazione finora

- Investment Property Accounting StandardDocumento18 pagineInvestment Property Accounting StandardvijaykumartaxNessuna valutazione finora

- FBL Annual Report 2019Documento130 pagineFBL Annual Report 2019Fuaad DodooNessuna valutazione finora

- Global Transition of HR Practices During COVID-19Documento5 pagineGlobal Transition of HR Practices During COVID-19Md. Saifullah TariqueNessuna valutazione finora

- Elements of Financial StatementsDocumento31 pagineElements of Financial StatementsThelearningHightsNessuna valutazione finora

- Internship Report (11504725) PDFDocumento39 pagineInternship Report (11504725) PDFpreetiNessuna valutazione finora

- MGMT E-2000 Fall 2014 SyllabusDocumento13 pagineMGMT E-2000 Fall 2014 Syllabusm1k0eNessuna valutazione finora

- Acquisition Analysis and RecommendationsDocumento49 pagineAcquisition Analysis and RecommendationsAnkitSawhneyNessuna valutazione finora

- FAR NotesDocumento11 pagineFAR NotesJhem Montoya OlendanNessuna valutazione finora

- Itc Balance SheetDocumento2 pagineItc Balance SheetRGNNishant BhatiXIIENessuna valutazione finora

- Annexure-I-Bharat Griha RakshaDocumento64 pagineAnnexure-I-Bharat Griha RakshaAtul KumarNessuna valutazione finora

- Alagappa University DDE BBM First Year Financial Accounting Exam - Paper2Documento5 pagineAlagappa University DDE BBM First Year Financial Accounting Exam - Paper2mansoorbariNessuna valutazione finora

- Credit Rating AgenciesDocumento40 pagineCredit Rating AgenciesSmriti DurehaNessuna valutazione finora

- 3.1.2 IFM Module2Documento18 pagine3.1.2 IFM Module2Aishwarya M RNessuna valutazione finora

- Rahma ConsutingDocumento6 pagineRahma ConsutingEko Firdausta TariganNessuna valutazione finora

- A122 Exercises QDocumento30 pagineA122 Exercises QBryan Jackson100% (1)

- Acct TutorDocumento22 pagineAcct TutorKthln Mntlla100% (1)

- Islamic FINTECH + CoverDocumento26 pagineIslamic FINTECH + CoverM Abi AbdillahNessuna valutazione finora

- Ali Mousa and Sons ContractingDocumento1 paginaAli Mousa and Sons ContractingMohsin aliNessuna valutazione finora

- Enterprise Risk Management - Beyond TheoryDocumento34 pagineEnterprise Risk Management - Beyond Theoryjcl_da_costa6894100% (4)

- Shamik Bhose September Crude Oil ReportDocumento8 pagineShamik Bhose September Crude Oil ReportshamikbhoseNessuna valutazione finora

- Free Accounting Firm Business PlanDocumento1 paginaFree Accounting Firm Business PlansolomonNessuna valutazione finora

- Questionnaire ThesisDocumento3 pagineQuestionnaire ThesisAnonymous 0kDzzBgr15Nessuna valutazione finora

- Merchant of Venice Act 2 Part 2Documento25 pagineMerchant of Venice Act 2 Part 2Verna Santos-NafradaNessuna valutazione finora

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Da EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Valutazione: 4.5 su 5 stelle4.5/5 (12)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Da EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Valutazione: 4.5 su 5 stelle4.5/5 (14)

- The Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsDa EverandThe Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsNessuna valutazione finora

- The E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItDa EverandThe E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItValutazione: 5 su 5 stelle5/5 (13)

- Profit First for Therapists: A Simple Framework for Financial FreedomDa EverandProfit First for Therapists: A Simple Framework for Financial FreedomNessuna valutazione finora

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindDa EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindValutazione: 5 su 5 stelle5/5 (231)

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassDa EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassNessuna valutazione finora

- Love Your Life Not Theirs: 7 Money Habits for Living the Life You WantDa EverandLove Your Life Not Theirs: 7 Money Habits for Living the Life You WantValutazione: 4.5 su 5 stelle4.5/5 (146)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Da EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Valutazione: 4.5 su 5 stelle4.5/5 (5)

- Financial Accounting For Dummies: 2nd EditionDa EverandFinancial Accounting For Dummies: 2nd EditionValutazione: 5 su 5 stelle5/5 (10)

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanDa EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanValutazione: 4.5 su 5 stelle4.5/5 (79)

- Finance Basics (HBR 20-Minute Manager Series)Da EverandFinance Basics (HBR 20-Minute Manager Series)Valutazione: 4.5 su 5 stelle4.5/5 (32)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesDa EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesNessuna valutazione finora

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetDa EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetNessuna valutazione finora

- Sacred Success: A Course in Financial MiraclesDa EverandSacred Success: A Course in Financial MiraclesValutazione: 5 su 5 stelle5/5 (15)

- Bookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesDa EverandBookkeeping: An Essential Guide to Bookkeeping for Beginners along with Basic Accounting PrinciplesValutazione: 4.5 su 5 stelle4.5/5 (30)

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyDa EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyValutazione: 5 su 5 stelle5/5 (1)

- Financial Accounting - Want to Become Financial Accountant in 30 Days?Da EverandFinancial Accounting - Want to Become Financial Accountant in 30 Days?Valutazione: 5 su 5 stelle5/5 (1)

- You Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantDa EverandYou Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantValutazione: 4 su 5 stelle4/5 (104)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsDa EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsValutazione: 4 su 5 stelle4/5 (7)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelDa Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelNessuna valutazione finora