Potrebbero piacerti anche

- The Economic Elite Vs The People of The United States of AmericaDocumento29 pagineThe Economic Elite Vs The People of The United States of Americajack007xrayNessuna valutazione finora

- CHRA Reviewer 3Documento15 pagineCHRA Reviewer 3Zaila Mitch100% (3)

- Summary of These Are the Plunderers by Gretchen Morgenson: How Private Equity Runs—and Wrecks—AmericaDa EverandSummary of These Are the Plunderers by Gretchen Morgenson: How Private Equity Runs—and Wrecks—AmericaNessuna valutazione finora

- American Rescue Plan Progress ReportDocumento8 pagineAmerican Rescue Plan Progress ReportJoecippNessuna valutazione finora

- 2.1solutions To Intermediate Public Economics Exercises PDFDocumento454 pagine2.1solutions To Intermediate Public Economics Exercises PDFMarc AC0% (1)

- Argument Paper FDDocumento7 pagineArgument Paper FDapi-312461507Nessuna valutazione finora

- Pipersundberg The Effects of Covid 2 6Documento5 paginePipersundberg The Effects of Covid 2 6api-666620541Nessuna valutazione finora

- The Great Ambiguity of The US EconomyDocumento4 pagineThe Great Ambiguity of The US EconomyJH_CarrNessuna valutazione finora

- WashPost, The battle over Biden’s child tax credit and its impact on poverty and workersDocumento6 pagineWashPost, The battle over Biden’s child tax credit and its impact on poverty and workersPaulo Vitor Antonacci MouraNessuna valutazione finora

- ChoroDocumento2 pagineChoroMariah ValdezNessuna valutazione finora

- Us Critical UnravelingDocumento11 pagineUs Critical UnravelingshelleyNessuna valutazione finora

- 1NC Foster R2Documento14 pagine1NC Foster R2Saje BushNessuna valutazione finora

- The Ledger 03/28/14Documento3 pagineThe Ledger 03/28/14American Enterprise InstituteNessuna valutazione finora

- It's A Wreck': 3.3 Million File Unemployment Claims As Economy Comes ApartDocumento10 pagineIt's A Wreck': 3.3 Million File Unemployment Claims As Economy Comes ApartJUNAID MIRZANessuna valutazione finora

- 5 MythsDocumento6 pagine5 MythsParvesh KhuranaNessuna valutazione finora

- The Good EconomyDocumento65 pagineThe Good EconomyRoosevelt Institute50% (2)

- Letter To President Biden Regarding Automatic StabilizersDocumento3 pagineLetter To President Biden Regarding Automatic StabilizersChris Berinato100% (6)

- Living Wages - MIT ArticlesDocumento9 pagineLiving Wages - MIT ArticlesUbaid ur Rehman SheikhNessuna valutazione finora

- End Poverty, Not the PoorDocumento2 pagineEnd Poverty, Not the PoorT BushmanNessuna valutazione finora

- Minimum Wage EssayDocumento5 pagineMinimum Wage EssayOwenNessuna valutazione finora

- Economic Growth: Key TakeawaysDocumento2 pagineEconomic Growth: Key TakeawaysAmerican Enterprise InstituteNessuna valutazione finora

- ArticolDocumento2 pagineArticolIoanaNessuna valutazione finora

- Article 3Documento17 pagineArticle 3Tianna Douglas LockNessuna valutazione finora

- COVID-19 recession shapes and economic recovery pathsDocumento3 pagineCOVID-19 recession shapes and economic recovery pathsnoviceNessuna valutazione finora

- American Welfare System Paper (5 On APsem Exam)Documento13 pagineAmerican Welfare System Paper (5 On APsem Exam)Livia HibshmanNessuna valutazione finora

- How The Pandemic Changed The U.S EconomyDocumento5 pagineHow The Pandemic Changed The U.S EconomyandresNessuna valutazione finora

- Midwest Edition: in Twin Cities, Improvement, GapsDocumento6 pagineMidwest Edition: in Twin Cities, Improvement, GapsPayersandProvidersNessuna valutazione finora

- A Bailout For The PeopleDocumento28 pagineA Bailout For The Peoplesirius57Nessuna valutazione finora

- SOTU Reactions: View It As A Web PageDocumento3 pagineSOTU Reactions: View It As A Web PageAmerican Enterprise InstituteNessuna valutazione finora

- Newton KuNe Neg 01 - Blue Valley Southwest OctasDocumento27 pagineNewton KuNe Neg 01 - Blue Valley Southwest OctasEmronNessuna valutazione finora

- Obama Stimulus Third AnniversaryDocumento6 pagineObama Stimulus Third AnniversarySenateRPCNessuna valutazione finora

- 19-07-11 Why The Wealthiest Americans Are The Real Job-KillersDocumento4 pagine19-07-11 Why The Wealthiest Americans Are The Real Job-KillersWilliam J GreenbergNessuna valutazione finora

- Covid 19 and The Great Depression SummativeDocumento3 pagineCovid 19 and The Great Depression Summative(Albert) Minkyu KimNessuna valutazione finora

- LocalDocumento11 pagineLocalJacob AronovitzNessuna valutazione finora

- Basic Income Poverty Aff Debate CaseDocumento67 pagineBasic Income Poverty Aff Debate CaseNicoNessuna valutazione finora

- How COVID-19 is Impacting Working LivesDocumento10 pagineHow COVID-19 is Impacting Working Livesroshik rughoonauthNessuna valutazione finora

- Before The Year Ends: Kevin HassettDocumento3 pagineBefore The Year Ends: Kevin HassettAmerican Enterprise InstituteNessuna valutazione finora

- Economics Commentary (Macro - Economics)Documento4 pagineEconomics Commentary (Macro - Economics)ariaNessuna valutazione finora

- The Organizer: February 2009Documento4 pagineThe Organizer: February 2009IATSENessuna valutazione finora

- Space Aff GrapevineDocumento25 pagineSpace Aff Grapevinegsd24337Nessuna valutazione finora

- Financial Resilience TaskForce Report - 29.10.19Documento36 pagineFinancial Resilience TaskForce Report - 29.10.19Mark Anthony KionisalaNessuna valutazione finora

- Spring 2014 Optimal Bundle: Issue XDocumento2 pagineSpring 2014 Optimal Bundle: Issue XColennonNessuna valutazione finora

- Long-Term Impacts of Job LossesDocumento5 pagineLong-Term Impacts of Job LossesirushadNessuna valutazione finora

- The Big Employer Still Adding Jobs and Boosting Pay - The Government - WSJDocumento4 pagineThe Big Employer Still Adding Jobs and Boosting Pay - The Government - WSJtimNessuna valutazione finora

- Income and Poverty in The COVID-19 Pandemic: Working PaperDocumento48 pagineIncome and Poverty in The COVID-19 Pandemic: Working PaperxgentusNessuna valutazione finora

- 2.5 AssignmentDocumento2 pagine2.5 AssignmentBhawna JoshiNessuna valutazione finora

- Policy Focus: Welfare Reform 2.0Documento6 paginePolicy Focus: Welfare Reform 2.0Independent Women's ForumNessuna valutazione finora

- The Economy Is Booming But Far From Normal, Posing A Challenge For BidenDocumento5 pagineThe Economy Is Booming But Far From Normal, Posing A Challenge For BidenDarrell SuNessuna valutazione finora

- Thesis On Economic Growth and Income InequalityDocumento8 pagineThesis On Economic Growth and Income Inequalitysheilaguyfargo100% (2)

- The Middle-Class SqueezeDocumento152 pagineThe Middle-Class SqueezeCenter for American Progress50% (2)

- America RecessionDocumento9 pagineAmerica RecessionashulibraNessuna valutazione finora

- Welfare reforms shaped modern systems and debatesDocumento15 pagineWelfare reforms shaped modern systems and debatesblaNessuna valutazione finora

- Opinion - Jobs Aren't Being Destroyed This Fast Elsewhere. Why Is That - The New York TimesDocumento2 pagineOpinion - Jobs Aren't Being Destroyed This Fast Elsewhere. Why Is That - The New York TimesJustBNessuna valutazione finora

- Principle 8: A Country'S Standard of Living Depends On Its Ability To Produce Goods and ServicesDocumento5 paginePrinciple 8: A Country'S Standard of Living Depends On Its Ability To Produce Goods and ServicesJanine AbucayNessuna valutazione finora

- Saliah DouglasDocumento8 pagineSaliah Douglasapi-425791806Nessuna valutazione finora

- FightingGlobPov PageDocumento16 pagineFightingGlobPov PageJ. Félix Angulo RascoNessuna valutazione finora

- Colle#7 - TheEconomy - 202304110004Documento1 paginaColle#7 - TheEconomy - 202304110004louna yunaNessuna valutazione finora

- RI - RecoveringandStructuringAfterCOVID19 IssueBrief 202010Documento16 pagineRI - RecoveringandStructuringAfterCOVID19 IssueBrief 202010ArgonzNessuna valutazione finora

- InsidersPower March 2015Documento15 pagineInsidersPower March 2015InterAnalyst, LLCNessuna valutazione finora

- Pathways To Opportunity ReportDocumento45 paginePathways To Opportunity ReportcaitlinthompsonNessuna valutazione finora

- The Ledger 03/21/14Documento3 pagineThe Ledger 03/21/14American Enterprise InstituteNessuna valutazione finora

- Editorial: Scandinavian Housing and Planning ResearchDocumento2 pagineEditorial: Scandinavian Housing and Planning ResearchgioanelaNessuna valutazione finora

- Capital Leakage From Owner-Occupied Housing: Jim Kemeny and Andrew ThomasDocumento18 pagineCapital Leakage From Owner-Occupied Housing: Jim Kemeny and Andrew ThomasgioanelaNessuna valutazione finora

- The Significance of Swedish Rental Policy: Cost Renting: Command Economy Versus The Social Market in Comparative PerspectiveDocumento14 pagineThe Significance of Swedish Rental Policy: Cost Renting: Command Economy Versus The Social Market in Comparative PerspectivegioanelaNessuna valutazione finora

- Post Industrial Housing Crisis-A Comment On Anneli Juntto: Scandinavian Housing and Planning ResearchDocumento2 paginePost Industrial Housing Crisis-A Comment On Anneli Juntto: Scandinavian Housing and Planning ResearchgioanelaNessuna valutazione finora

- Political Science Faculty Win 2 Major CSU AwardsDocumento6 paginePolitical Science Faculty Win 2 Major CSU AwardsgioanelaNessuna valutazione finora

- Figure I.2. The Capital/income Ratio in Europe, 1870-2010: Germany France United KingdomDocumento1 paginaFigure I.2. The Capital/income Ratio in Europe, 1870-2010: Germany France United KingdomgioanelaNessuna valutazione finora

- F10 5-2 PDFDocumento1 paginaF10 5-2 PDFgioanelaNessuna valutazione finora

- Contemporary Issue PaperDocumento1 paginaContemporary Issue PapergioanelaNessuna valutazione finora

- Religion Is Not What It Used To Be. Consumerism, Neoliberalism, and The Global Reshaping of ReligionDocumento10 pagineReligion Is Not What It Used To Be. Consumerism, Neoliberalism, and The Global Reshaping of ReligiongioanelaNessuna valutazione finora

- A Qualitative Examination of Jim Kemeny's Arguments On High Home Ownership, The Retirement Pension and The Dualist Rental System Focusing On AustraliaDocumento23 pagineA Qualitative Examination of Jim Kemeny's Arguments On High Home Ownership, The Retirement Pension and The Dualist Rental System Focusing On AustraliagioanelaNessuna valutazione finora

- F10 10 PDFDocumento1 paginaF10 10 PDFgioanelaNessuna valutazione finora

- Figure 1.1. The Distribution of World Output 1700-2012: Asia AfricaDocumento1 paginaFigure 1.1. The Distribution of World Output 1700-2012: Asia AfricagioanelaNessuna valutazione finora

- 2020.4 Coronavirus Crisis Underlines Weak Spots in U.S. Economic System - The New York TimesDocumento3 pagine2020.4 Coronavirus Crisis Underlines Weak Spots in U.S. Economic System - The New York TimesgioanelaNessuna valutazione finora

- Plagiarism in The Japanese Universities: Truly A Cultural Matter?Documento13 paginePlagiarism in The Japanese Universities: Truly A Cultural Matter?gioanelaNessuna valutazione finora

- Renewable and Sustainable Energy ReviewsDocumento15 pagineRenewable and Sustainable Energy ReviewsgioanelaNessuna valutazione finora

- Rati 12127Documento16 pagineRati 12127gioanelaNessuna valutazione finora

- Global Poverty Section 102 & 105 SyllabusDocumento2 pagineGlobal Poverty Section 102 & 105 SyllabusgioanelaNessuna valutazione finora

- 2020.4 Coronavirus Stimulus Package F.A.Q. - Checks, Unemployment, Layoffs and More - The New York TimesDocumento12 pagine2020.4 Coronavirus Stimulus Package F.A.Q. - Checks, Unemployment, Layoffs and More - The New York TimesgioanelaNessuna valutazione finora

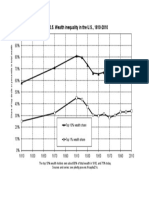

- Wealth inequality in the U.S. over 200 years: top 10% own 80% in 1910, 75% todayDocumento1 paginaWealth inequality in the U.S. over 200 years: top 10% own 80% in 1910, 75% todaygioanelaNessuna valutazione finora

- Geopolitics and Diffusion of Economics in Communist RomaniaDocumento22 pagineGeopolitics and Diffusion of Economics in Communist RomaniagioanelaNessuna valutazione finora

- Sumer Travel 2020 FlightsDocumento2 pagineSumer Travel 2020 FlightsgioanelaNessuna valutazione finora

- Dan BadulescuDocumento2 pagineDan BadulescugioanelaNessuna valutazione finora

- Smith1776 1Documento98 pagineSmith1776 1gioanelaNessuna valutazione finora

- Contemporary Issue PaperDocumento1 paginaContemporary Issue PapergioanelaNessuna valutazione finora

- F10 5-2 PDFDocumento1 paginaF10 5-2 PDFgioanelaNessuna valutazione finora

- Book Review - Has Globalization Gone Too Far - by Dani Rodrik. Wash PDFDocumento18 pagineBook Review - Has Globalization Gone Too Far - by Dani Rodrik. Wash PDFgioanelaNessuna valutazione finora

- 2020.4 Coronavirus Stimulus Package F.A.Q. - Checks, Unemployment, Layoffs and More - The New York TimesDocumento12 pagine2020.4 Coronavirus Stimulus Package F.A.Q. - Checks, Unemployment, Layoffs and More - The New York TimesgioanelaNessuna valutazione finora

- F1 1 PDFDocumento1 paginaF1 1 PDFgioanelaNessuna valutazione finora

- F10 10 PDFDocumento1 paginaF10 10 PDFgioanelaNessuna valutazione finora

- Essay On Child Labour For Children and StudentsDocumento7 pagineEssay On Child Labour For Children and StudentsIshank Singh100% (1)

- Investing in China Offers Low Costs and Huge MarketDocumento10 pagineInvesting in China Offers Low Costs and Huge MarketUroOj SaleEmNessuna valutazione finora

- Concern Over Business Automation and Artificial IntelligenceDocumento22 pagineConcern Over Business Automation and Artificial Intelligencelauradiez29Nessuna valutazione finora

- A Pandemic Was Inevitable. Why Was No One Ready?: Israel, U.A.E. To Establish Formal TiesDocumento55 pagineA Pandemic Was Inevitable. Why Was No One Ready?: Israel, U.A.E. To Establish Formal TiesradionshopNessuna valutazione finora

- Intersectionality of Marginalization andDocumento6 pagineIntersectionality of Marginalization andYashica HargunaniNessuna valutazione finora

- Decent Work According To ILO: Benefits IncludeDocumento4 pagineDecent Work According To ILO: Benefits IncludeSharlaine CabanayanNessuna valutazione finora

- Unit 3 Contd..Outplacement Services & Job RotationDocumento10 pagineUnit 3 Contd..Outplacement Services & Job RotationGabriel BelmonteNessuna valutazione finora

- Labor Process TheoryDocumento13 pagineLabor Process TheoryteslimsNessuna valutazione finora

- Mortality Morbidity and Health Selection Among Met PDFDocumento81 pagineMortality Morbidity and Health Selection Among Met PDFLuis EcheverriNessuna valutazione finora

- Demographic Effects On Labor Force Participation RateDocumento7 pagineDemographic Effects On Labor Force Participation RatemichaelNessuna valutazione finora

- FINAL PROJECT - PHÂN TÍCH THIẾT KẾ HỆ THỐNG THÔNG TINDocumento47 pagineFINAL PROJECT - PHÂN TÍCH THIẾT KẾ HỆ THỐNG THÔNG TINNguyễn Khánh HàNessuna valutazione finora

- Spoken Corpus Comes To Life: Reading Passage 1Documento12 pagineSpoken Corpus Comes To Life: Reading Passage 1Đức LêNessuna valutazione finora

- Tugas 1 Mata Kuliah Bahasa Inggris Niaga: NAMA: Faris Rahman Al - Bantani NIM: 042902212Documento2 pagineTugas 1 Mata Kuliah Bahasa Inggris Niaga: NAMA: Faris Rahman Al - Bantani NIM: 042902212Raina RahmayantiNessuna valutazione finora

- I Economic Development: Capita-Gdp-Has-Reached-An-All-Time-High-Under-Duterte/#1db297e169b1Documento40 pagineI Economic Development: Capita-Gdp-Has-Reached-An-All-Time-High-Under-Duterte/#1db297e169b1Che MerluNessuna valutazione finora

- Peter Drucker - The New Society (Ocr)Documento187 paginePeter Drucker - The New Society (Ocr)Anders FernstedtNessuna valutazione finora

- Managing Philanthropy - BCF Covid Special Report 2020Documento24 pagineManaging Philanthropy - BCF Covid Special Report 2020BernewsAdminNessuna valutazione finora

- The Impact of Covid-19 On Unemployment of BangladeshDocumento5 pagineThe Impact of Covid-19 On Unemployment of BangladeshMahinur MimiNessuna valutazione finora

- 0304 - Ec 2Documento29 pagine0304 - Ec 2haryhunterNessuna valutazione finora

- Unemployment Among GraduatesDocumento52 pagineUnemployment Among GraduatesIshrat PopyNessuna valutazione finora

- The Last Chronicles of Planet Earth July 11 2010 Edition by Frank Dimora 3Documento291 pagineThe Last Chronicles of Planet Earth July 11 2010 Edition by Frank Dimora 3ticklemeNessuna valutazione finora

- Report - How Robots Change The WorldDocumento64 pagineReport - How Robots Change The Worldhector gonzalezNessuna valutazione finora

- Moudud Jamee Strategic Competition Dynamics&Role of StateDocumento183 pagineMoudud Jamee Strategic Competition Dynamics&Role of StateHuei ChangNessuna valutazione finora

- Macroeconomics NotesDocumento5 pagineMacroeconomics Noteschuchaylopez7Nessuna valutazione finora

- Procedure Manual For Epwp Phase 3 PDFDocumento59 pagineProcedure Manual For Epwp Phase 3 PDFBizimenyera Zenza TheonesteNessuna valutazione finora

- TheamericandreamDocumento7 pagineTheamericandreamapi-307666609Nessuna valutazione finora

- Shocks and Policy Responses in The Open Economy: (This Is A Draft Chapter of A New Book - Carlin & Soskice (200x) )Documento25 pagineShocks and Policy Responses in The Open Economy: (This Is A Draft Chapter of A New Book - Carlin & Soskice (200x) )Martiniano MajoralNessuna valutazione finora

- Tutorial 8 MCQ QuestionDocumento2 pagineTutorial 8 MCQ QuestionMC SquiddyNessuna valutazione finora

- Notes On Public Policy MakingDocumento91 pagineNotes On Public Policy MakingaindreasNessuna valutazione finora