Potrebbero piacerti anche

- Cost Terminology FeladatokDocumento6 pagineCost Terminology FeladatokЭниЭ.Nessuna valutazione finora

- Accounts For Manufacturing FirmsDocumento17 pagineAccounts For Manufacturing FirmsZegera Mgendi100% (2)

- A7 Topic 10 - Gross Profit Variance AnalysisDocumento1 paginaA7 Topic 10 - Gross Profit Variance AnalysisAnna CharlotteNessuna valutazione finora

- Quiz Financial Management 1keyDocumento14 pagineQuiz Financial Management 1keyAdiansyach Patonangi100% (1)

- Treasury Management Vs Cash Management Answer To Warm Up ExercisesDocumento8 pagineTreasury Management Vs Cash Management Answer To Warm Up Exercisesephraim0% (1)

- c5 Solutions BudgetingDocumento13 paginec5 Solutions BudgetingChinnam Lalitha100% (1)

- QS09 - Class Exercises SolutionDocumento4 pagineQS09 - Class Exercises Solutionlyk0tex100% (1)

- Cash Budget Problems and SolutionsDocumento6 pagineCash Budget Problems and Solutionstamberahul1256Nessuna valutazione finora

- Ex and P-BudgetingDocumento10 pagineEx and P-BudgetingJessa Swing Dela CruzNessuna valutazione finora

- BudgetingDocumento130 pagineBudgetingRevathi AnandNessuna valutazione finora

- BASTRCSX Learning Activity 5 - With AnswersDocumento10 pagineBASTRCSX Learning Activity 5 - With AnswersChel EscuetaNessuna valutazione finora

- Brewer8e GEs PPT Chapter 8 UpdDocumento22 pagineBrewer8e GEs PPT Chapter 8 UpdNguyễn Ngọc Quỳnh TiênNessuna valutazione finora

- DocxDocumento6 pagineDocxMico Duñas CruzNessuna valutazione finora

- Master Budgeting (Sample Problems With Answers)Documento11 pagineMaster Budgeting (Sample Problems With Answers)Jonalyn TaboNessuna valutazione finora

- ACt1104 Final Quiz No. 1wit AnsDocumento7 pagineACt1104 Final Quiz No. 1wit AnsDyenNessuna valutazione finora

- BudgetingDocumento74 pagineBudgetingRevathi AnandNessuna valutazione finora

- Review Problem: Budget Schedules: RequiredDocumento8 pagineReview Problem: Budget Schedules: RequiredShafa AlyaNessuna valutazione finora

- Questions On Cash Budget-2Documento7 pagineQuestions On Cash Budget-2Mpolokeng HlabanaNessuna valutazione finora

- Chap07 Rev. FI5 Ex PRDocumento11 pagineChap07 Rev. FI5 Ex PRKhryzha Hanne Dela CruzNessuna valutazione finora

- Budget Questions Hac1Documento5 pagineBudget Questions Hac1odedeyi aishat0% (1)

- Master BudgetDocumento36 pagineMaster BudgetRafols AnnabelleNessuna valutazione finora

- Yunita Pangala (A031191177) - Akuntansi Manajemen (Tugas Mandiri)Documento4 pagineYunita Pangala (A031191177) - Akuntansi Manajemen (Tugas Mandiri)elvienNessuna valutazione finora

- Problems On Budgets and Budgetary ControlDocumento10 pagineProblems On Budgets and Budgetary ControlParthasarathi MishraNessuna valutazione finora

- Taller de Ejercicios de PresupuestosDocumento11 pagineTaller de Ejercicios de PresupuestosalexNessuna valutazione finora

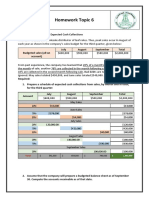

- Homework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionsDocumento3 pagineHomework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionskhetamNessuna valutazione finora

- BudgetingDocumento51 pagineBudgetingVignesh KivickyNessuna valutazione finora

- Obien, Francine Denise Eleanor G. Abm 12 Y1-7Documento2 pagineObien, Francine Denise Eleanor G. Abm 12 Y1-7Emar Kim0% (1)

- QuizDocumento15 pagineQuizMark Domingo Mendoza100% (1)

- Cost Accounting Assignment #2Documento5 pagineCost Accounting Assignment #2BRIANNIE ASRI VIVASNessuna valutazione finora

- FALL Class 7 - Cash Budgeting - Ch9 - GDBA - Note # 7 - TEACHERDocumento7 pagineFALL Class 7 - Cash Budgeting - Ch9 - GDBA - Note # 7 - TEACHERAkankshaNessuna valutazione finora

- Inventory Valuation and Gross Profit MethodDocumento3 pagineInventory Valuation and Gross Profit MethodLuiNessuna valutazione finora

- Lecture 11Documento26 pagineLecture 11Riaz Baloch Notezai100% (1)

- Chap07 Rev. FI5 Ex PR 1Documento10 pagineChap07 Rev. FI5 Ex PR 1Beyond ThatNessuna valutazione finora

- Budget Exercises - Part II (Model Answers)Documento7 pagineBudget Exercises - Part II (Model Answers)Menna AssemNessuna valutazione finora

- 4.2 Answers and Solutions - Assignment On Materials and LaborDocumento8 pagine4.2 Answers and Solutions - Assignment On Materials and LaborRoselyn LumbaoNessuna valutazione finora

- Buying and MerchDocumento4 pagineBuying and Merchapi-513411115Nessuna valutazione finora

- Management Accounting: BudgetingDocumento45 pagineManagement Accounting: BudgetingAdam Smith80% (5)

- Cash BudgetingDocumento5 pagineCash BudgetingAnissa GeddesNessuna valutazione finora

- Session 7 Practice Questions - Profit Planning: Multiple ChoiceDocumento4 pagineSession 7 Practice Questions - Profit Planning: Multiple ChoiceLee Freckles Haengbok0% (1)

- Exercise 1 Margarett Company: Sales BudgetDocumento4 pagineExercise 1 Margarett Company: Sales BudgetHannaniah PabicoNessuna valutazione finora

- Chapter Two: Master Budget and Responsibility AccountingDocumento25 pagineChapter Two: Master Budget and Responsibility Accountingweyn deguNessuna valutazione finora

- BudgetingDocumento28 pagineBudgetingJade Gomez50% (2)

- Financial Forecasting: Production Requirements (LO2) Sales For Western Boot Stores Are Expected To Be 40,000Documento13 pagineFinancial Forecasting: Production Requirements (LO2) Sales For Western Boot Stores Are Expected To Be 40,000Juliet Dorado100% (1)

- Exercises 4 Financial Planning BudgetingDocumento2 pagineExercises 4 Financial Planning BudgetingKyle PereiraNessuna valutazione finora

- Solution CH.8Documento10 pagineSolution CH.8Thanawat PHURISIRUNGROJNessuna valutazione finora

- Budgeting Pretest Teachers PDFDocumento4 pagineBudgeting Pretest Teachers PDFKatzkie Montemayor GodinezNessuna valutazione finora

- Merchandise Business Class PerformanceDocumento5 pagineMerchandise Business Class PerformanceGrace GamillaNessuna valutazione finora

- Notes PayableDocumento9 pagineNotes Payablerencelor21Nessuna valutazione finora

- CAS 11 Midterm QuizDocumento7 pagineCAS 11 Midterm QuizShariine BestreNessuna valutazione finora

- Homework On Inventories: Problem 1Documento3 pagineHomework On Inventories: Problem 1Amy SpencerNessuna valutazione finora

- Budget and Budgetary Control - Mba Ca. Asim K. Biswas: Question # 1Documento7 pagineBudget and Budgetary Control - Mba Ca. Asim K. Biswas: Question # 1Suraj KumarNessuna valutazione finora

- Question On Budget A LevelDocumento3 pagineQuestion On Budget A LevelMUSTHARI KHANNessuna valutazione finora

- Long Quiz Receivables AA MPDocumento2 pagineLong Quiz Receivables AA MPKay Hanalee Villanueva Norio25% (4)

- Exercise 3 BudgetingDocumento4 pagineExercise 3 BudgetingGabrielleNessuna valutazione finora

- (02D) Inventories Assignment 02 ANSWER KEYDocumento9 pagine(02D) Inventories Assignment 02 ANSWER KEYGabriel Adrian ObungenNessuna valutazione finora

- QS09 - Class ExercisesDocumento4 pagineQS09 - Class Exerciseslyk0texNessuna valutazione finora

- Quiz 4 Budgeting (For Students)Documento5 pagineQuiz 4 Budgeting (For Students)agaceram9090Nessuna valutazione finora

- Problem No. 1: Ap - 1Stpb - 05.07Documento10 pagineProblem No. 1: Ap - 1Stpb - 05.07AnnNessuna valutazione finora

- Budgeting - Planning: A325 Discussion - March 19, 2012Documento8 pagineBudgeting - Planning: A325 Discussion - March 19, 2012alfaNessuna valutazione finora

- Exercises 7A1 and 7B1: Book: Administrative AccountingDocumento9 pagineExercises 7A1 and 7B1: Book: Administrative AccountingScribdTranslationsNessuna valutazione finora

- 11 Land Capital (Complete Version)Documento3 pagine11 Land Capital (Complete Version)ЭниЭ.Nessuna valutazione finora

- Speak For 10 Minutes, I'd Ask You To Save Your Question at The End. Now I Want You To Look at Person No Paper,, Sitting Next To You, Try ToDocumento3 pagineSpeak For 10 Minutes, I'd Ask You To Save Your Question at The End. Now I Want You To Look at Person No Paper,, Sitting Next To You, Try ToЭниЭ.Nessuna valutazione finora

- Examination Questions: Introduction To ManagementDocumento1 paginaExamination Questions: Introduction To ManagementЭниЭ.Nessuna valutazione finora

- College of International Management and BusinessDocumento4 pagineCollege of International Management and BusinessЭниЭ.Nessuna valutazione finora

- Problem SetDocumento8 pagineProblem SetЭниЭ.Nessuna valutazione finora

- Its Main Objective Is Improving Economic Efficiency, Especially Labor ProductivityDocumento5 pagineIts Main Objective Is Improving Economic Efficiency, Especially Labor ProductivityЭниЭ.Nessuna valutazione finora

- CH 6 Exhibit 12 Q 19-22Documento4 pagineCH 6 Exhibit 12 Q 19-22ЭниЭ.Nessuna valutazione finora

- Sara Hajiyeva Enkhtsetseg Enkhbaatar Mai Ho Hoang VyDocumento10 pagineSara Hajiyeva Enkhtsetseg Enkhbaatar Mai Ho Hoang VyЭниЭ.Nessuna valutazione finora

- Question 8. T-Account Entries and Balance Sheet PreparationDocumento2 pagineQuestion 8. T-Account Entries and Balance Sheet PreparationЭниЭ.Nessuna valutazione finora

- CH 7 Exhibit 13, 14 Q 23-25Documento4 pagineCH 7 Exhibit 13, 14 Q 23-25ЭниЭ.Nessuna valutazione finora

- CH 3 Exhibit 3Documento1 paginaCH 3 Exhibit 3ЭниЭ.Nessuna valutazione finora

- Bus Econ QuestionsDocumento4 pagineBus Econ QuestionsЭниЭ.Nessuna valutazione finora

- CH 4 Exhibit 6Documento3 pagineCH 4 Exhibit 6ЭниЭ.Nessuna valutazione finora

- Acc Question 7 11Documento4 pagineAcc Question 7 11ЭниЭ.Nessuna valutazione finora

- CH 12 Exhibit 22Documento4 pagineCH 12 Exhibit 22ЭниЭ.Nessuna valutazione finora

- Exhibit 7. Revenue and Expense RecognitionDocumento6 pagineExhibit 7. Revenue and Expense RecognitionЭниЭ.Nessuna valutazione finora

- CH 1 Exhibit 1 Q 1-5Documento6 pagineCH 1 Exhibit 1 Q 1-5ЭниЭ.Nessuna valutazione finora

- CH 1 Exhibit 1 Q 1-5Documento6 pagineCH 1 Exhibit 1 Q 1-5ЭниЭ.Nessuna valutazione finora

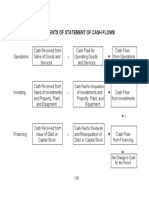

- CH 12 Components of CF StatementDocumento1 paginaCH 12 Components of CF StatementЭниЭ.Nessuna valutazione finora

- CH 8 Question 28 SolutionDocumento1 paginaCH 8 Question 28 SolutionЭниЭ.Nessuna valutazione finora

- Exhibit 17. Goodwill Calculation and The Consolidated Balance SheetDocumento4 pagineExhibit 17. Goodwill Calculation and The Consolidated Balance SheetЭниЭ.Nessuna valutazione finora

- CH 3 Exhibit 4, 5Documento5 pagineCH 3 Exhibit 4, 5ЭниЭ.Nessuna valutazione finora

- CH 1 Q 3b, 4a SolutionsDocumento2 pagineCH 1 Q 3b, 4a SolutionsЭниЭ.Nessuna valutazione finora

- CH 1 Definition of AccountingDocumento1 paginaCH 1 Definition of AccountingЭниЭ.Nessuna valutazione finora

- CH 3 Exhibit 4, 5Documento5 pagineCH 3 Exhibit 4, 5ЭниЭ.Nessuna valutazione finora

- CH 3 Exhibit 2Documento1 paginaCH 3 Exhibit 2ЭниЭ.Nessuna valutazione finora

- Questions Question 6. Journal Entries, T-Accounts, and Balance Sheet PreparationDocumento2 pagineQuestions Question 6. Journal Entries, T-Accounts, and Balance Sheet PreparationЭниЭ.Nessuna valutazione finora

- Unwomen What Is Local Government and How Is It OrganizedDocumento42 pagineUnwomen What Is Local Government and How Is It OrganizedHifsa AimenNessuna valutazione finora

- Fat Test (Jawaban)Documento19 pagineFat Test (Jawaban)Carat ForeverNessuna valutazione finora

- Contract Drafting BrochureDocumento10 pagineContract Drafting BrochureUtkarshini SinhaNessuna valutazione finora

- Waste Recycliny System IeeeDocumento3 pagineWaste Recycliny System IeeeAmit KumarNessuna valutazione finora

- "Barcode" Web Service: ManualDocumento64 pagine"Barcode" Web Service: ManualЕгон ЧарнојевићNessuna valutazione finora

- Achieving Superior QualityDocumento2 pagineAchieving Superior QualityPradeep ChintuNessuna valutazione finora

- PPTXDocumento26 paginePPTXmohsinziaNessuna valutazione finora

- Training Design On Expanded Monthly Agricultural and Fisheries Situation Reporting System (EMAFSRS)Documento6 pagineTraining Design On Expanded Monthly Agricultural and Fisheries Situation Reporting System (EMAFSRS)Gamel DeanNessuna valutazione finora

- Data-Visualization-Plan .Documento54 pagineData-Visualization-Plan .NabillahNessuna valutazione finora

- EXEMPTIONDocumento15 pagineEXEMPTIONAndrey PavlovskiyNessuna valutazione finora

- 7 PHILIPPINE NATIONAL BANK, Petitioner, vs. GREGORIO B. MARAYA, JR. and WENEFRIDA MARAYA, Respondents.Documento2 pagine7 PHILIPPINE NATIONAL BANK, Petitioner, vs. GREGORIO B. MARAYA, JR. and WENEFRIDA MARAYA, Respondents.Ken MarcaidaNessuna valutazione finora

- Chapter 3 Case Part 2Documento3 pagineChapter 3 Case Part 2graceNessuna valutazione finora

- Race and SportsDocumento29 pagineRace and SportsAngela BrownNessuna valutazione finora

- Oromia Regional Government - Phase II Expectations and WorkplanDocumento4 pagineOromia Regional Government - Phase II Expectations and WorkplanÁkosSzabóNessuna valutazione finora

- Contract of SaleDocumento4 pagineContract of Salecorvinmihai591Nessuna valutazione finora

- Hudson Transfer Press BrochureDocumento2 pagineHudson Transfer Press BrochureSean GribbenNessuna valutazione finora

- Business and IndustyDocumento3 pagineBusiness and IndustysantoshskpurNessuna valutazione finora

- FSSC 22000 GUIDELINE - FSSC CertificationDocumento14 pagineFSSC 22000 GUIDELINE - FSSC CertificationFelix MwandukaNessuna valutazione finora

- HW Chap 6Documento4 pagineHW Chap 6uong huonglyNessuna valutazione finora

- Ansell Healthcare Products LLC To Acquire Exam Specialty Glove Supplier DigitcareDocumento2 pagineAnsell Healthcare Products LLC To Acquire Exam Specialty Glove Supplier DigitcareRazvanRotaruNessuna valutazione finora

- Marketing DraftDocumento6 pagineMarketing DraftSwan HtetNessuna valutazione finora

- InteretrustDocumento21 pagineInteretrustConstantin WellsNessuna valutazione finora

- Sales Process Flow Chart (PDF, 118kb) - New Prodigy Marketing ...Documento5 pagineSales Process Flow Chart (PDF, 118kb) - New Prodigy Marketing ...Ian YongNessuna valutazione finora

- Welcome Pack ULIP PDFDocumento16 pagineWelcome Pack ULIP PDFRyan Putra GushendraNessuna valutazione finora

- Organizational Change and Development: Attempt All QuestionsDocumento2 pagineOrganizational Change and Development: Attempt All QuestionsJAYA JOSHI 2017408Nessuna valutazione finora

- ABM Module 3 Week 3 ORG. AND MANAGEMENT FINAL MODULEDocumento13 pagineABM Module 3 Week 3 ORG. AND MANAGEMENT FINAL MODULEJay Mark InobayaNessuna valutazione finora

- Employment Registration Form of Foreign Employees in China PDFDocumento1 paginaEmployment Registration Form of Foreign Employees in China PDFFabio SerranoNessuna valutazione finora

- LAI Insurance RequirementsDocumento3 pagineLAI Insurance RequirementsMatthew EveringhamNessuna valutazione finora

- The Rise of The Inclusive ConsumerDocumento6 pagineThe Rise of The Inclusive ConsumerpenstyloNessuna valutazione finora

- Titan Company - WikipediaDocumento74 pagineTitan Company - Wikipediakay617138Nessuna valutazione finora