Potrebbero piacerti anche

- Impact Assessment AAK: Taxes and the Local Manufacture of PesticidesDa EverandImpact Assessment AAK: Taxes and the Local Manufacture of PesticidesNessuna valutazione finora

- Energy Recovery From WasteDocumento31 pagineEnergy Recovery From WasteSyed UmerNessuna valutazione finora

- Impact assessment AAK: The impact of Tax on the Local Manufacture of PesticidesDa EverandImpact assessment AAK: The impact of Tax on the Local Manufacture of PesticidesNessuna valutazione finora

- Income StatementDocumento3 pagineIncome StatementKhari haranNessuna valutazione finora

- United KingdomDocumento16 pagineUnited KingdomspephdNessuna valutazione finora

- Effutu Municipal Assembly POWER POINTDocumento28 pagineEffutu Municipal Assembly POWER POINTNana-Osei MainooNessuna valutazione finora

- BASF Report 2020Documento324 pagineBASF Report 2020Rafael FalconNessuna valutazione finora

- LB Kingston Upon ThamesDocumento3 pagineLB Kingston Upon ThamesparkingeconomicsNessuna valutazione finora

- MTAG-OB PPT (Form 4)Documento24 pagineMTAG-OB PPT (Form 4)Allan BeceraNessuna valutazione finora

- Engr. Charity Hope GayatinDocumento5 pagineEngr. Charity Hope Gayatinmedwin moralesNessuna valutazione finora

- Mushroom Farming Project ReportDocumento2 pagineMushroom Farming Project ReportSuman Kumar AdhikaryNessuna valutazione finora

- Ogjournal20201005 DL PDFDocumento68 pagineOgjournal20201005 DL PDFMarcelo SchaderNessuna valutazione finora

- 3 Analisis de Opciones y Propuesta Financiera (Ingles)Documento6 pagine3 Analisis de Opciones y Propuesta Financiera (Ingles)Jair Fajrdo LopezNessuna valutazione finora

- Lao Soil & Nutrition Company WhitepaperDocumento11 pagineLao Soil & Nutrition Company WhitepaperJulianNessuna valutazione finora

- Initial Investment: MaterialsDocumento10 pagineInitial Investment: MaterialsBeomiNessuna valutazione finora

- Laying The Groundwork For Jatropha-Based Biofuel Industry in The PhilippinesDocumento20 pagineLaying The Groundwork For Jatropha-Based Biofuel Industry in The PhilippinesUPLB Office of the Vice Chancellor for Research and ExtensionNessuna valutazione finora

- Calpine SolutionDocumento5 pagineCalpine SolutionDarshan GosaliaNessuna valutazione finora

- Biofuels Directive - Implications For IrelandDocumento40 pagineBiofuels Directive - Implications For IrelandBharath KumarNessuna valutazione finora

- Waste To Energy: Project Advisory & Structured FinanceDocumento30 pagineWaste To Energy: Project Advisory & Structured FinanceSantoshi SahooNessuna valutazione finora

- Untitled SpreadsheetDocumento11 pagineUntitled SpreadsheetBeomiNessuna valutazione finora

- Organic Farming Hub Raises Soil Health in LaosDocumento13 pagineOrganic Farming Hub Raises Soil Health in LaosJulianNessuna valutazione finora

- "Good Practices" in Policies and Measures: The Case of Costa RicaDocumento7 pagine"Good Practices" in Policies and Measures: The Case of Costa RicagregoryhageNessuna valutazione finora

- Carbicrete ReportDocumento33 pagineCarbicrete Reportelaine liNessuna valutazione finora

- North Macedonia Country Fact SheetDocumento18 pagineNorth Macedonia Country Fact SheetBiljanaNessuna valutazione finora

- DOF Presentation On TRAIN LawDocumento39 pagineDOF Presentation On TRAIN LawRogel RomeroNessuna valutazione finora

- Public - Private Partnerships and Solid Waste Management InfrastructureDocumento28 paginePublic - Private Partnerships and Solid Waste Management InfrastructureAntonis Mavropoulos100% (2)

- QGISBudget 2020Documento1 paginaQGISBudget 2020Yves-donald MakoumbouNessuna valutazione finora

- Solution Bebelac Uas Abm 2Documento9 pagineSolution Bebelac Uas Abm 2Hasna SeptianiNessuna valutazione finora

- Sample ComputationDocumento13 pagineSample ComputationKathleen AngidNessuna valutazione finora

- Sarvajal - Estados Financieros 211028-PDF-ENG-19Documento1 paginaSarvajal - Estados Financieros 211028-PDF-ENG-19Santiago et AlejandraNessuna valutazione finora

- Item 2U Staff ReportDocumento22 pagineItem 2U Staff ReportAnonymous PkeI8e84RsNessuna valutazione finora

- 3R Implementation in Indonesia Asia 3R ConferenceDocumento20 pagine3R Implementation in Indonesia Asia 3R ConferenceAndre SuitoNessuna valutazione finora

- PDF FileDocumento42 paginePDF FileNagavenkat.ChNessuna valutazione finora

- Current Approach Unsustainable. Energy Challenges Are GlobalDocumento25 pagineCurrent Approach Unsustainable. Energy Challenges Are Globalsustainovate_meNessuna valutazione finora

- Textile Costing Lecture 08 CVP in TextilesDocumento2 pagineTextile Costing Lecture 08 CVP in TextilesNeha Jain100% (1)

- Optimizing Domestic Gas Allocation For The Development of National IndustryDocumento36 pagineOptimizing Domestic Gas Allocation For The Development of National IndustryaxlpceNessuna valutazione finora

- Documento 2 TraducidoDocumento7 pagineDocumento 2 TraducidosergioNessuna valutazione finora

- Eco Profile 2018 Chapter-5Documento24 pagineEco Profile 2018 Chapter-5Nicole LayganNessuna valutazione finora

- Septage Treatment Options CEPT PM 20-1-17Documento25 pagineSeptage Treatment Options CEPT PM 20-1-17Suchitwa MissionNessuna valutazione finora

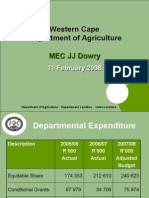

- Western Cape Department of AgricultureDocumento37 pagineWestern Cape Department of AgricultureezlynxNessuna valutazione finora

- Raw Material Costing AnalysisDocumento9 pagineRaw Material Costing AnalysisKevin PersadNessuna valutazione finora

- 241804052027.Sample-DPR Upgradation Distillery Effluent Treatment SystemDocumento31 pagine241804052027.Sample-DPR Upgradation Distillery Effluent Treatment SystemNagaraja SNessuna valutazione finora

- Atbsp Map-Abcd 070218 PDFDocumento113 pagineAtbsp Map-Abcd 070218 PDFGsp ChrismonNessuna valutazione finora

- Ekonomi Hans DadiDocumento279 pagineEkonomi Hans DadiHans DadiNessuna valutazione finora

- Chemical tanker voyage budget and detailsDocumento145 pagineChemical tanker voyage budget and detailsBoldashNessuna valutazione finora

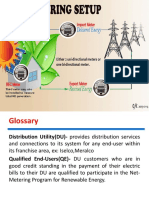

- Net-metering glossary and ROI sampleDocumento30 pagineNet-metering glossary and ROI sampleBilly Twaine Palma FuerteNessuna valutazione finora

- Answers To 11 - 16 Assignment in ABC PDFDocumento3 pagineAnswers To 11 - 16 Assignment in ABC PDFMubarrach MatabalaoNessuna valutazione finora

- AsratDocumento27 pagineAsratMechal Awerka SmammoNessuna valutazione finora

- BusinessPlan Mooncard 2019 2026 vIGF VadDocumento2.151 pagineBusinessPlan Mooncard 2019 2026 vIGF VadHed GnabryNessuna valutazione finora

- Tugas PPE 1Documento12 pagineTugas PPE 1Bertha Liona0% (1)

- 1-1 - Presentation of CBAM Taiwan April 23Documento29 pagine1-1 - Presentation of CBAM Taiwan April 23陳鼎元Nessuna valutazione finora

- Expert Group Meeting on Waste-to-Energy in Asian RegionDocumento33 pagineExpert Group Meeting on Waste-to-Energy in Asian RegionLuong Thu HaNessuna valutazione finora

- WACS Villaba, LeyteDocumento11 pagineWACS Villaba, Leyteroderick biazonNessuna valutazione finora

- Fecal Sludge Management - BORDA Permpong PhumwisetDocumento32 pagineFecal Sludge Management - BORDA Permpong PhumwisetamskalNessuna valutazione finora

- Appendix N Economic AnalysisDocumento10 pagineAppendix N Economic AnalysisRoui Jean VillarNessuna valutazione finora

- Michele Panella - GSE S.p.ADocumento28 pagineMichele Panella - GSE S.p.ArodrigoaraujogNessuna valutazione finora

- Budget For 2010/2011 Financial YearDocumento6 pagineBudget For 2010/2011 Financial YearJapie BoschNessuna valutazione finora

- Wnsum22 Part 43Documento1 paginaWnsum22 Part 43Holiday GreetingsNessuna valutazione finora

- Corporate Social Responsibility in GlobalizationDocumento49 pagineCorporate Social Responsibility in GlobalizationghdavaNessuna valutazione finora

- Case 10 CLAUS StatementDocumento6 pagineCase 10 CLAUS StatementClaudia AgüeraNessuna valutazione finora

- Metal Robot Background PPT TemplateDocumento25 pagineMetal Robot Background PPT TemplateJeeryNessuna valutazione finora

- Get Back Campaign Infographic Takeout of Reports FinalDocumento1 paginaGet Back Campaign Infographic Takeout of Reports FinalNebojsa RedzicNessuna valutazione finora

- UNDP Report On Environmental JusticeDocumento36 pagineUNDP Report On Environmental JusticeNebojsa RedzicNessuna valutazione finora

- WGEMA Questionnaire English 19042021Documento6 pagineWGEMA Questionnaire English 19042021Nebojsa RedzicNessuna valutazione finora

- Your Guide To Environmental Metrics: How To Develop and Track Environmental Metrics That Drive Enterprise PerformanceDocumento4 pagineYour Guide To Environmental Metrics: How To Develop and Track Environmental Metrics That Drive Enterprise PerformanceNebojsa RedzicNessuna valutazione finora

- Mapping ESPON 2013 DataDocumento25 pagineMapping ESPON 2013 DataOmark ArmNessuna valutazione finora

- Guidance Document n28Documento69 pagineGuidance Document n28Nebojsa RedzicNessuna valutazione finora

- Policy Framework Closed Loop Recycling Access Recycled ContentDocumento4 paginePolicy Framework Closed Loop Recycling Access Recycled ContentNebojsa RedzicNessuna valutazione finora

- 1 s2.0 S2352550922002251 MainDocumento10 pagine1 s2.0 S2352550922002251 MainNebojsa RedzicNessuna valutazione finora

- Zero Waste Training Handbook Guide</h1Documento199 pagineZero Waste Training Handbook Guide</h1Nebojsa RedzicNessuna valutazione finora

- 666 9-RelationWasteGenerationDocumento9 pagine666 9-RelationWasteGenerationNebojsa RedzicNessuna valutazione finora

- Ipcc Far WG III Chapter 03Documento28 pagineIpcc Far WG III Chapter 03Nebojsa RedzicNessuna valutazione finora

- Bc-1720-H Magnetic BikeDocumento13 pagineBc-1720-H Magnetic BikeNebojsa RedzicNessuna valutazione finora

- Quality Assurance and Quality ControlDocumento17 pagineQuality Assurance and Quality Controltraslie0% (1)

- Validation and Verification of GHG EmissionsDocumento67 pagineValidation and Verification of GHG EmissionsNebojsa RedzicNessuna valutazione finora

- Guide to Preparing a Working Plan for ScrapyardsDocumento6 pagineGuide to Preparing a Working Plan for ScrapyardsNebojsa RedzicNessuna valutazione finora

- 5th SEETO RSWG - Conclusions-Final2Documento6 pagine5th SEETO RSWG - Conclusions-Final2Nebojsa RedzicNessuna valutazione finora

- Preparation of A Spatialised Emission Inventory As Input For ModellingDocumento11 paginePreparation of A Spatialised Emission Inventory As Input For ModellingNebojsa RedzicNessuna valutazione finora

- DR AF T: End-of-Waste - Guidance DocumentDocumento26 pagineDR AF T: End-of-Waste - Guidance DocumentNebojsa RedzicNessuna valutazione finora

- AcomprehensiveQA-QCmethodology Dec2010Documento13 pagineAcomprehensiveQA-QCmethodology Dec2010mapykNessuna valutazione finora

- Sus 2017 29092 Aml PDFDocumento10 pagineSus 2017 29092 Aml PDFNebojsa RedzicNessuna valutazione finora

- Principal National Waste Management Plans and Strategies: Please State Your Desired Location On The Application FormDocumento3 paginePrincipal National Waste Management Plans and Strategies: Please State Your Desired Location On The Application FormNebojsa RedzicNessuna valutazione finora

- Pocket Guide To Capa City Buildin G: Fo R Cli M Ate C H An G EDocumento52 paginePocket Guide To Capa City Buildin G: Fo R Cli M Ate C H An G ENebojsa RedzicNessuna valutazione finora

- DR AF T: End-of-Waste - Guidance DocumentDocumento26 pagineDR AF T: End-of-Waste - Guidance DocumentNebojsa RedzicNessuna valutazione finora

- Document PDFDocumento4 pagineDocument PDFNebojsa RedzicNessuna valutazione finora

- Estimates of European Food Waste Levels PDFDocumento80 pagineEstimates of European Food Waste Levels PDFNacho ILzarbeNessuna valutazione finora

- Theenvironmentalproblemsfromaneconomicperspectiveluciavreja 15Documento10 pagineTheenvironmentalproblemsfromaneconomicperspectiveluciavreja 15Nebojsa RedzicNessuna valutazione finora

- Brief Overview on the Benefits of a Circular EconomyDocumento17 pagineBrief Overview on the Benefits of a Circular EconomyNebojsa RedzicNessuna valutazione finora

- FMM Transportation RecsDocumento11 pagineFMM Transportation RecsNebojsa RedzicNessuna valutazione finora

- Climate change M&E helps address impactsDocumento4 pagineClimate change M&E helps address impactsNebojsa RedzicNessuna valutazione finora

- Earth Song WorksheetDocumento3 pagineEarth Song Worksheetapi-252155626Nessuna valutazione finora

- Slow and Rapid Sand Filter EssayDocumento10 pagineSlow and Rapid Sand Filter EssayAbhijith SPNessuna valutazione finora

- BP Stats Review 2021 All DataDocumento624 pagineBP Stats Review 2021 All Dataivan sudibyoNessuna valutazione finora

- Redevelopment of Macchabhaudi, Dharan: Project ProposalDocumento7 pagineRedevelopment of Macchabhaudi, Dharan: Project Proposaldiwas baralNessuna valutazione finora

- Z240Documento26 pagineZ240Dany BonaventuraNessuna valutazione finora

- Scania P, G, R, T Series Workshop Manual - BatteriesDocumento4 pagineScania P, G, R, T Series Workshop Manual - Batterieswahyu2308100501Nessuna valutazione finora

- Drilling Waste Management Strategy for Field 'XDocumento10 pagineDrilling Waste Management Strategy for Field 'XMochamad adjie PamungkasNessuna valutazione finora

- 106-Article Text-203-1-10-20190109Documento8 pagine106-Article Text-203-1-10-20190109Raffel Wahyu MahardikaNessuna valutazione finora

- Disposable cups and the environment - which is betterDocumento3 pagineDisposable cups and the environment - which is bettertappannNessuna valutazione finora

- Voltas VRF Variable Refrigerant Flow PDFDocumento36 pagineVoltas VRF Variable Refrigerant Flow PDFYogesh0% (1)

- Ramboll Smart Cities Solutions IndiaDocumento9 pagineRamboll Smart Cities Solutions IndiaAbrar AhmadNessuna valutazione finora

- Ali Hassan (Ent-514)Documento18 pagineAli Hassan (Ent-514)Ali hassanNessuna valutazione finora

- Sekisui Thermobreak LS - Brochure 090516 INTL LOW RESDocumento4 pagineSekisui Thermobreak LS - Brochure 090516 INTL LOW RESTuyen NguyenNessuna valutazione finora

- James Graham - Presentation SlidesDocumento29 pagineJames Graham - Presentation Slidesapi-516075595Nessuna valutazione finora

- Scout of The World AwardDocumento1 paginaScout of The World AwardBim SagunNessuna valutazione finora

- CDP Hoshangabad EnglishDocumento220 pagineCDP Hoshangabad EnglishRidhi SaxenaNessuna valutazione finora

- The Taiga Ecosystem: By: Yomi Florentino and Rihanna DougilDocumento6 pagineThe Taiga Ecosystem: By: Yomi Florentino and Rihanna DougilCaoimhe Siri FlorentinoNessuna valutazione finora

- Circular Cities Week 2021 - CEC MalaysiaDocumento19 pagineCircular Cities Week 2021 - CEC MalaysiaNorman SuliNessuna valutazione finora

- Renewable and Sustainable Energy ReviewsDocumento18 pagineRenewable and Sustainable Energy ReviewsExequiel Monrroy MarquardtNessuna valutazione finora

- Pricelist Tank Poly June 2022 1Documento2 paginePricelist Tank Poly June 2022 1KrishHookoomNessuna valutazione finora

- Abu Dhabi Guidelines CollectionDocumento4 pagineAbu Dhabi Guidelines CollectionlplkwvNessuna valutazione finora

- Climate Change Impacts Philippine AgricultureDocumento32 pagineClimate Change Impacts Philippine AgricultureAroon Pol OlletNessuna valutazione finora

- Depletion of Natural ResourcesDocumento34 pagineDepletion of Natural ResourcesKartika Bhuvaneswaran NairNessuna valutazione finora

- Da Form 5458Documento2 pagineDa Form 5458Time ofNessuna valutazione finora

- TEWI CalculationDocumento228 pagineTEWI Calculationmirali74Nessuna valutazione finora

- Chapter 7 Climate and BiodiversityDocumento68 pagineChapter 7 Climate and BiodiversityBernard DayotNessuna valutazione finora

- Environmental Management System (E.M.S.) AND ISO 14000 SeriesDocumento12 pagineEnvironmental Management System (E.M.S.) AND ISO 14000 Seriessinghaks_2601Nessuna valutazione finora

- Solution To Homework Assignment No.9Documento2 pagineSolution To Homework Assignment No.9Phambra FiverNessuna valutazione finora

- Earth and Life Science Q1 Week 9Documento22 pagineEarth and Life Science Q1 Week 9Tabada NickyNessuna valutazione finora

- Garbage Cleaning Ship Based On Image Processing TechnologyDocumento8 pagineGarbage Cleaning Ship Based On Image Processing TechnologyBayang SilamNessuna valutazione finora