Potrebbero piacerti anche

- Real Estate Sector IndiaDocumento15 pagineReal Estate Sector IndiaMohan DhimanNessuna valutazione finora

- Real Estate Sector IndiaDocumento14 pagineReal Estate Sector Indiabhaktipmaldikar12Nessuna valutazione finora

- Real EstateDocumento8 pagineReal EstateViswanathan BalaNessuna valutazione finora

- Sales and Promotion of Real Estate ProjectDocumento73 pagineSales and Promotion of Real Estate ProjectShubham Bhardwaj100% (1)

- DLF Fundamental AnalysisDocumento20 pagineDLF Fundamental Analysismuzamilbasu0% (1)

- DLF Business Research Report DelhiDocumento65 pagineDLF Business Research Report DelhiPurnansh GuptaNessuna valutazione finora

- "A Study of The Prospects and Challenges of Real Estate Market" (With Special Reference To Thane District.)Documento8 pagine"A Study of The Prospects and Challenges of Real Estate Market" (With Special Reference To Thane District.)shweta meshramNessuna valutazione finora

- DLF Real Estate Project ReportDocumento75 pagineDLF Real Estate Project Reportअंकित Jindal61% (28)

- Double Impact NMIMSDocumento9 pagineDouble Impact NMIMSabeer_chakravartiNessuna valutazione finora

- Certificate: Submitted ToDocumento75 pagineCertificate: Submitted ToAmit AggarwalNessuna valutazione finora

- Chapter L: Industry Profile: Global ScenarioDocumento42 pagineChapter L: Industry Profile: Global ScenarioYounus ahmedNessuna valutazione finora

- FSM Sonamon 354Documento30 pagineFSM Sonamon 354Yashu Sharma100% (1)

- Real EstateDocumento59 pagineReal EstateManish RajakNessuna valutazione finora

- Dump - Indian Real State SectorDocumento10 pagineDump - Indian Real State SectorDeepak AgrawalNessuna valutazione finora

- DLFDocumento93 pagineDLFNamita SharmaNessuna valutazione finora

- Complete ProjectDocumento54 pagineComplete ProjectAbhijit SahaNessuna valutazione finora

- DLF - Real Estate MarketingDocumento60 pagineDLF - Real Estate MarketingChirag Thakwani85% (13)

- Real Estate: (Industry Guide) By:-Aamir SaleemDocumento18 pagineReal Estate: (Industry Guide) By:-Aamir SaleemAamir SaleemNessuna valutazione finora

- Real EstateDocumento78 pagineReal EstateKushal Mansukhani0% (1)

- RG GroupDocumento55 pagineRG GroupUpender GoelNessuna valutazione finora

- Summer Project On Real Est. Page .1Documento55 pagineSummer Project On Real Est. Page .1manisha_s200774% (19)

- Summer Training Report - RitikaDocumento69 pagineSummer Training Report - Ritikaritika_honey2377% (30)

- Management For Investment in Real EstateDocumento27 pagineManagement For Investment in Real Estatevasu989898Nessuna valutazione finora

- Real Estate Current ScenarioDocumento40 pagineReal Estate Current ScenariovedangibarotNessuna valutazione finora

- Project Report GRP (A08)Documento16 pagineProject Report GRP (A08)sagerofgyanNessuna valutazione finora

- Marketing StrategiesDocumento63 pagineMarketing StrategiesChetan PahwaNessuna valutazione finora

- Case Study Final VersionDocumento21 pagineCase Study Final VersionAnkit GangwarNessuna valutazione finora

- DLF: Real Estate Leadership in India: Vikas KujurDocumento29 pagineDLF: Real Estate Leadership in India: Vikas KujurVikas KujurNessuna valutazione finora

- FDI Experience in Indian Real Estate: Key HighlightsDocumento6 pagineFDI Experience in Indian Real Estate: Key HighlightsPallavi JhaNessuna valutazione finora

- DLF LTD.: Dr. Trilochan Tripathy, Faculty, IBS, HyderabadDocumento26 pagineDLF LTD.: Dr. Trilochan Tripathy, Faculty, IBS, Hyderabadsumitsabharwal17Nessuna valutazione finora

- Final ArticleDocumento12 pagineFinal ArticlesahulreddyNessuna valutazione finora

- A Study of Consumer Behavior in Real Estate Sector: Inderpreet SinghDocumento17 pagineA Study of Consumer Behavior in Real Estate Sector: Inderpreet SinghMahesh KhadeNessuna valutazione finora

- Asim Final DissertationDocumento83 pagineAsim Final Dissertationshad.jawdNessuna valutazione finora

- Real Estate PPT - V GoodDocumento144 pagineReal Estate PPT - V GoodShreenivas KVNessuna valutazione finora

- SdxgbdsDocumento9 pagineSdxgbdsTushar ShanNessuna valutazione finora

- BUSINESS LAWS PROJECT REPORT ON Issues Relating To Housing SectorDocumento20 pagineBUSINESS LAWS PROJECT REPORT ON Issues Relating To Housing SectorDishant GuptaNessuna valutazione finora

- Ê VV VVVV - .11V/Vvvv V$$VVV.VDocumento6 pagineÊ VV VVVV - .11V/Vvvv V$$VVV.VZubala Marium HelalNessuna valutazione finora

- Objective: Fundamental Analysis of Real Estate Sector in IndiaDocumento44 pagineObjective: Fundamental Analysis of Real Estate Sector in IndiaDnyaneshwar DaundNessuna valutazione finora

- Literature Review of Real Estate Sector in IndiaDocumento6 pagineLiterature Review of Real Estate Sector in Indiagvyztm2f100% (1)

- Real Estate Sector in IndiaDocumento11 pagineReal Estate Sector in IndiaVISHNU VIJAYAN100% (1)

- Shivam Real EstateDocumento46 pagineShivam Real EstateTasmay EnterprisesNessuna valutazione finora

- Final ProjectDocumento76 pagineFinal ProjectBHARATNessuna valutazione finora

- A ON Real Estate Sector OF India: Submitted By: Pooja Bhavsar Enrollment No: 10Bsphh010193Documento19 pagineA ON Real Estate Sector OF India: Submitted By: Pooja Bhavsar Enrollment No: 10Bsphh010193Pooja BhavsarNessuna valutazione finora

- Section F-Group 10 (Real Estate)Documento21 pagineSection F-Group 10 (Real Estate)Meghwant ThakurNessuna valutazione finora

- Indian Real Estate Opening Doors PDFDocumento18 pagineIndian Real Estate Opening Doors PDFkoolyogesh1Nessuna valutazione finora

- Consumer Behaviour Regarding Real EstateDocumento68 pagineConsumer Behaviour Regarding Real Estateparteekbhatia1989Nessuna valutazione finora

- Main Chapters of WIP 1 To 15 (PGDM - PIBM)Documento37 pagineMain Chapters of WIP 1 To 15 (PGDM - PIBM)Khushi SharmaNessuna valutazione finora

- Real Estate Sector in IndiaDocumento29 pagineReal Estate Sector in IndiaAmreen ParkarNessuna valutazione finora

- Overview of Indian Infrastructure, Real Estate & Construction IndustryDocumento25 pagineOverview of Indian Infrastructure, Real Estate & Construction IndustryShekhar SahNessuna valutazione finora

- Provincial Facilitation for Investment and Trade Index: Measuring Economic Governance for Business Development in the Lao People’s Democratic Republic-Second EditionDa EverandProvincial Facilitation for Investment and Trade Index: Measuring Economic Governance for Business Development in the Lao People’s Democratic Republic-Second EditionNessuna valutazione finora

- Dot.compradors: Power and Policy in the Development of the Indian Software IndustryDa EverandDot.compradors: Power and Policy in the Development of the Indian Software IndustryNessuna valutazione finora

- Emerging FinTech: Understanding and Maximizing Their BenefitsDa EverandEmerging FinTech: Understanding and Maximizing Their BenefitsNessuna valutazione finora

- Harnessing Technology for More Inclusive and Sustainable Finance in Asia and the PacificDa EverandHarnessing Technology for More Inclusive and Sustainable Finance in Asia and the PacificNessuna valutazione finora

- Toward Inclusive Access to Trade Finance: Lessons from the Trade Finance Gaps, Growth, and Jobs SurveyDa EverandToward Inclusive Access to Trade Finance: Lessons from the Trade Finance Gaps, Growth, and Jobs SurveyNessuna valutazione finora

- Rethinking Infrastructure Financing for Southeast Asia in the Post-Pandemic EraDa EverandRethinking Infrastructure Financing for Southeast Asia in the Post-Pandemic EraNessuna valutazione finora

- Innovative Infrastructure Financing through Value Capture in IndonesiaDa EverandInnovative Infrastructure Financing through Value Capture in IndonesiaValutazione: 5 su 5 stelle5/5 (1)

- Real Estate Investing: Building Wealth with Property Investments: Expert Advice for Professionals: A Series on Industry-Specific Guidance, #2Da EverandReal Estate Investing: Building Wealth with Property Investments: Expert Advice for Professionals: A Series on Industry-Specific Guidance, #2Nessuna valutazione finora

- Globalization and Outsourcing: Framing The DebateDocumento7 pagineGlobalization and Outsourcing: Framing The DebateShreya AgrawalNessuna valutazione finora

- Written Assignments For 15.769Documento2 pagineWritten Assignments For 15.769Shreya AgrawalNessuna valutazione finora

- 15.912 Technology Strategy: Mit OpencoursewareDocumento14 pagine15.912 Technology Strategy: Mit OpencoursewareShreya AgrawalNessuna valutazione finora

- Inventory TemplateDocumento2 pagineInventory TemplateShreya AgrawalNessuna valutazione finora

- Abcd QzieDocumento4 pagineAbcd QzieShreya AgrawalNessuna valutazione finora

- Outsourcing and Moving Up The Value ChainDocumento2 pagineOutsourcing and Moving Up The Value ChainShreya AgrawalNessuna valutazione finora

- Inventory TemplateDocumento2 pagineInventory TemplateShreya AgrawalNessuna valutazione finora

- The Hindu Business Line: Marico Seeks To Experiment, Introduces Prototypes To Fuel Growth of SaffolaDocumento2 pagineThe Hindu Business Line: Marico Seeks To Experiment, Introduces Prototypes To Fuel Growth of SaffolaShreya AgrawalNessuna valutazione finora

- Branded Foods in India - Forecasts To 2015: 2008 Edition: Oils and FatsDocumento4 pagineBranded Foods in India - Forecasts To 2015: 2008 Edition: Oils and FatsShreya AgrawalNessuna valutazione finora

- The Hindu Business Line: Adani Wilmar To Strengthen Food Play With Offerings in Packaged StaplesDocumento2 pagineThe Hindu Business Line: Adani Wilmar To Strengthen Food Play With Offerings in Packaged StaplesShreya AgrawalNessuna valutazione finora

- Ruchi Soya Industries LimitedDocumento67 pagineRuchi Soya Industries LimitedShreya AgrawalNessuna valutazione finora

- Ruchi Soya Industries Ltd. - Consumer Packaged Goods - Company Profile, SWOT & Financial AnalysisDocumento45 pagineRuchi Soya Industries Ltd. - Consumer Packaged Goods - Company Profile, SWOT & Financial AnalysisShreya AgrawalNessuna valutazione finora

- ProQuestDocuments 2020 08 17 PDFDocumento2 pagineProQuestDocuments 2020 08 17 PDFShreya AgrawalNessuna valutazione finora

- TATA TimelineDocumento12 pagineTATA TimelineShreya AgrawalNessuna valutazione finora

- Macroeconomics Extra Practice ProblemsDocumento2 pagineMacroeconomics Extra Practice ProblemsShreya AgrawalNessuna valutazione finora

- In-Class Practice Questions For Perfect Competitive MarketDocumento6 pagineIn-Class Practice Questions For Perfect Competitive MarketShreya AgrawalNessuna valutazione finora

- Managing Customer Responsiveness at Littlefield TechnologiesDocumento2 pagineManaging Customer Responsiveness at Littlefield TechnologiesShreya AgrawalNessuna valutazione finora

- Carnegie Mellon Pittsburgh Self-Driving Vehicles Bill PedutoDocumento3 pagineCarnegie Mellon Pittsburgh Self-Driving Vehicles Bill PedutoShreya AgrawalNessuna valutazione finora

- According To Customer's Frequency of Visits: Preferred BeverageDocumento1 paginaAccording To Customer's Frequency of Visits: Preferred BeverageShreya AgrawalNessuna valutazione finora

- Analyst Presentation JULY 2019: The Crest, GurugramDocumento44 pagineAnalyst Presentation JULY 2019: The Crest, GurugramShreya AgrawalNessuna valutazione finora

- Elec 1 Module 15Documento11 pagineElec 1 Module 15John Mikeel FloresNessuna valutazione finora

- FULL Download Ebook PDF International Business 16th Edition by John Daniels PDF EbookDocumento41 pagineFULL Download Ebook PDF International Business 16th Edition by John Daniels PDF Ebookquiana.dobiesz290100% (33)

- Tracking, Track Parcels, Packages, Shipments - DHL Express TrackingDocumento2 pagineTracking, Track Parcels, Packages, Shipments - DHL Express TrackingmmemonNessuna valutazione finora

- WeTransfer On Companies and CommunitiesDocumento51 pagineWeTransfer On Companies and CommunitiescgoulartNessuna valutazione finora

- D&D 5.0 - Aventura (Nível 7) O Refúgio Perdido Do ArquimagoDocumento30 pagineD&D 5.0 - Aventura (Nível 7) O Refúgio Perdido Do ArquimagoMurilo TeixeiraNessuna valutazione finora

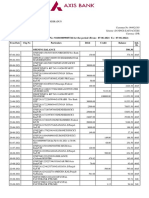

- Statement of Axis Account No:921010009005726 For The Period (From: 07-06-2021 To: 07-06-2022)Documento22 pagineStatement of Axis Account No:921010009005726 For The Period (From: 07-06-2021 To: 07-06-2022)TusharNessuna valutazione finora

- 916 3460 1 PBDocumento12 pagine916 3460 1 PBWiwin NovaNessuna valutazione finora

- UnlockedDocumento27 pagineUnlockedSameer DeshmukhNessuna valutazione finora

- Management Advisory ServicesDocumento14 pagineManagement Advisory ServicesChrizzele Quiohilag Sonsing100% (1)

- Environmental AnalysisDocumento11 pagineEnvironmental AnalysisRupanshi GuptaNessuna valutazione finora

- PR File OmpanyDocumento15 paginePR File OmpanybassemNessuna valutazione finora

- Certificate of Approval: Precision Equipments (Chennai) Pvt. LTDDocumento2 pagineCertificate of Approval: Precision Equipments (Chennai) Pvt. LTDAnonymous AyDvqgNessuna valutazione finora

- Problem 5-4Documento3 pagineProblem 5-4Diata Ian100% (4)

- Class Participation 4 - ADMS 1500 A&B - F17 Q1. (5 Marks) Financial Accounting Information and Managerial Accounting Information Have ADocumento4 pagineClass Participation 4 - ADMS 1500 A&B - F17 Q1. (5 Marks) Financial Accounting Information and Managerial Accounting Information Have Aaj singhNessuna valutazione finora

- Report On Apex Food Limited and Fu Wang Food LimitedDocumento17 pagineReport On Apex Food Limited and Fu Wang Food LimitedNaqvi KhanNessuna valutazione finora

- Principles of Accounting-Mid Term PaperDocumento7 paginePrinciples of Accounting-Mid Term PaperAbdullahNessuna valutazione finora

- M3 Lesson 3 Books of AccountsDocumento6 pagineM3 Lesson 3 Books of AccountsJohn Benedict Capiral TehNessuna valutazione finora

- Accura Diagnostics AMC Proposal All DocumentDocumento6 pagineAccura Diagnostics AMC Proposal All DocumentMahadeva SwamyNessuna valutazione finora

- Sec. 35 (1) (Ii) CBDT Approves Christian Medical College Vellore Association - Taxguru - inDocumento3 pagineSec. 35 (1) (Ii) CBDT Approves Christian Medical College Vellore Association - Taxguru - inSalilPeedikakkandiNessuna valutazione finora

- Brand Purpose BEDocumento8 pagineBrand Purpose BEAniruddha_basakNessuna valutazione finora

- Hidden City Ticketing DraftDocumento43 pagineHidden City Ticketing DraftPavan KethavathNessuna valutazione finora

- Verma EnterprisesDocumento2 pagineVerma EnterpriseskapilazarchitectsNessuna valutazione finora

- Bank StatementDocumento4 pagineBank StatementKristin BrooksNessuna valutazione finora

- KPMG Annual Report 2020 WebDocumento46 pagineKPMG Annual Report 2020 WebHo DasNessuna valutazione finora

- P08. Cash & Accrual BasisDocumento3 pagineP08. Cash & Accrual Basisayushiridara kwonNessuna valutazione finora

- Chapter 10 Audit 1Documento2 pagineChapter 10 Audit 1Ismah ParkNessuna valutazione finora

- Trends 1 Trends vs. FadsDocumento16 pagineTrends 1 Trends vs. FadsjacilcadacNessuna valutazione finora

- Offer AcceptanceDocumento13 pagineOffer AcceptanceKai LumNessuna valutazione finora

- Ultimate Guide To Crypto Airdrops in 2024 - 20240113 - 085833 - 0000Documento24 pagineUltimate Guide To Crypto Airdrops in 2024 - 20240113 - 085833 - 0000jonathanjasper842Nessuna valutazione finora

- PATHFINDERINTERMEDIATEMAY2013Documento108 paginePATHFINDERINTERMEDIATEMAY2013ALIU HADINessuna valutazione finora