Potrebbero piacerti anche

- Cookery & Bakery: Ruwan Ranasinghe, BSC, MbaDocumento61 pagineCookery & Bakery: Ruwan Ranasinghe, BSC, MbaCHATURIKA priyadarshaniNessuna valutazione finora

- Intro To Cost Control in FNBDocumento47 pagineIntro To Cost Control in FNBBilly Joe VillenaNessuna valutazione finora

- Food Courts Food Malls Banquet Halls Set Up ConsultancyDocumento28 pagineFood Courts Food Malls Banquet Halls Set Up ConsultancymohamadNessuna valutazione finora

- Presupuesto FamiliarbDocumento10 paginePresupuesto FamiliarbmmauryfgNessuna valutazione finora

- Prof. V. B. Shah Institute of ManagementDocumento69 pagineProf. V. B. Shah Institute of ManagementFaidz FuadNessuna valutazione finora

- Basic and Common Competencies ExamDocumento2 pagineBasic and Common Competencies ExamNoreen Cañaveral NochefrancaNessuna valutazione finora

- Comply With Workplace Hygiene Procedures: Unit Code: D1.HRS - CL1.05 D1.HOT - CL1.04 D2.TTO - CL4.10Documento187 pagineComply With Workplace Hygiene Procedures: Unit Code: D1.HRS - CL1.05 D1.HOT - CL1.04 D2.TTO - CL4.10irneil H. PepitoNessuna valutazione finora

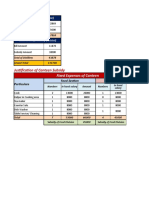

- Justification of Canteen SubsidyDocumento2 pagineJustification of Canteen SubsidyGaurav Vij Asstt. Manager - H.RNessuna valutazione finora

- Apply Basic Techniques of Commercial Cookery: D1.HCC - CL2.01Documento83 pagineApply Basic Techniques of Commercial Cookery: D1.HCC - CL2.01Desireersws u EspejonqtNessuna valutazione finora

- SP Session1Documento72 pagineSP Session1Abood Abood100% (1)

- Soezzy'S Catering Planner V 3.06Documento8 pagineSoezzy'S Catering Planner V 3.06José Manuel VazNessuna valutazione finora

- Rev MNGTDocumento63 pagineRev MNGTKiran MayiNessuna valutazione finora

- Kitchen Equipment SelectionDocumento21 pagineKitchen Equipment Selectioncucucucucu72Nessuna valutazione finora

- Assgnmnt Sheet Wa 01 DTRDocumento5 pagineAssgnmnt Sheet Wa 01 DTRNana TanNessuna valutazione finora

- Foodservice Internship Plan Manual Revised 2021 1Documento25 pagineFoodservice Internship Plan Manual Revised 2021 1Ralph Vincent GalzoteNessuna valutazione finora

- ADG Staffing Matrix As at 13-6-11 FINALDocumento44 pagineADG Staffing Matrix As at 13-6-11 FINALAnanda ZoelfaNessuna valutazione finora

- Excel 3 TestDocumento3 pagineExcel 3 Testapi-233183465Nessuna valutazione finora

- Sake Inventory and Cost - 16 Feb '15Documento2 pagineSake Inventory and Cost - 16 Feb '15Tom TommyNessuna valutazione finora

- Копия Restaurant Site ReviewDocumento14 pagineКопия Restaurant Site ReviewАнастасия КруминаNessuna valutazione finora

- Waste Managment NKA UPES Mar 2-2k11Documento64 pagineWaste Managment NKA UPES Mar 2-2k11Nk AgarwalNessuna valutazione finora

- Restaurant Cleaning Checklist: Week in Use: InitialsDocumento3 pagineRestaurant Cleaning Checklist: Week in Use: InitialsSampalau AnglerNessuna valutazione finora

- Lesson Plan Food and RestaurantDocumento3 pagineLesson Plan Food and RestaurantNath ZuletaNessuna valutazione finora

- Establishing Sales TargetDocumento10 pagineEstablishing Sales TargetErich VirayNessuna valutazione finora

- Covid 19 Secure ToolkitDocumento44 pagineCovid 19 Secure ToolkitDianNessuna valutazione finora

- Employee Schedule1Documento4 pagineEmployee Schedule1Faishal KalbuadiNessuna valutazione finora

- Food Storing and Issuing Control: Principles of Food, Beverage, and Labour Cost Controls, Canadian EditionDocumento26 pagineFood Storing and Issuing Control: Principles of Food, Beverage, and Labour Cost Controls, Canadian Editionnur sharmira mohamdNessuna valutazione finora

- Controlling Food SalesDocumento20 pagineControlling Food SalesMuhammad Salihin Jaafar100% (1)

- Job Description Cook IDocumento2 pagineJob Description Cook IYogie Si el'NinoNessuna valutazione finora

- Kitchen SOP For Operating Meat Slicer or Slicing MachineDocumento3 pagineKitchen SOP For Operating Meat Slicer or Slicing MachineAmgad saqrNessuna valutazione finora

- Chapter 05 The Flow of Food An IntroductionDocumento12 pagineChapter 05 The Flow of Food An Introductiondajonaef89Nessuna valutazione finora

- Prepared By: Janice N. Lupango Btled Iii-He Checked By: Jonnel Q. Bernardez Course InstructorDocumento47 paginePrepared By: Janice N. Lupango Btled Iii-He Checked By: Jonnel Q. Bernardez Course InstructorVirginia LupangoNessuna valutazione finora

- Kitchen Brigade Job RolesDocumento2 pagineKitchen Brigade Job RolesAndrew KillipNessuna valutazione finora

- QSM Finals 2 - Service Excellence - Leading The Way To WowDocumento14 pagineQSM Finals 2 - Service Excellence - Leading The Way To WowCasas MhelbbieNessuna valutazione finora

- U12601 Prepare and Clear Tables and Service AreasDocumento11 pagineU12601 Prepare and Clear Tables and Service AreasAshli GrantNessuna valutazione finora

- 15 Utensils and 5 Equipments: Anggota Kelompok: Yohana Riri Dian Hery BOYDocumento21 pagine15 Utensils and 5 Equipments: Anggota Kelompok: Yohana Riri Dian Hery BOYNadzwaaNessuna valutazione finora

- Prep Cook ChecklistDocumento14 paginePrep Cook ChecklistJay OhNessuna valutazione finora

- Guidelines For Plating FoodDocumento21 pagineGuidelines For Plating FoodCHARLENE GEMINANessuna valutazione finora

- Hotel MuseFood Safety Monitoring Record Version 1Documento13 pagineHotel MuseFood Safety Monitoring Record Version 1Aditya SharmaNessuna valutazione finora

- Food Storing and Issuing ControlDocumento26 pagineFood Storing and Issuing ControldamianuskrowinNessuna valutazione finora

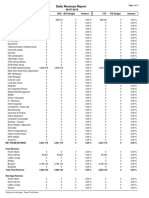

- Toast Profit Loss Statement Template 2022Documento24 pagineToast Profit Loss Statement Template 2022Krishna SharmaNessuna valutazione finora

- Cooksafe House RulesDocumento19 pagineCooksafe House RulesMUHAMMAD SUHAIB TAHIRNessuna valutazione finora

- SOP Template Food Production OBT 08LTB OSP T1FP 11-12-3Documento10 pagineSOP Template Food Production OBT 08LTB OSP T1FP 11-12-3munyekiNessuna valutazione finora

- Use Basic Methods of CookeryDocumento3 pagineUse Basic Methods of CookeryKemathi McnishNessuna valutazione finora

- HM 301 PDFDocumento159 pagineHM 301 PDFSona UthyasaniNessuna valutazione finora

- Daily Revenue ReportDocumento3 pagineDaily Revenue ReportRoftadiaWgNessuna valutazione finora

- Working in Tourism: ReadingDocumento65 pagineWorking in Tourism: ReadingMarcus VoNessuna valutazione finora

- Catering Management Element 1.1Documento10 pagineCatering Management Element 1.1JAML Create CornerNessuna valutazione finora

- BHM 232 Food and Beverage Operations 4Documento6 pagineBHM 232 Food and Beverage Operations 4Pankaj PathaniaNessuna valutazione finora

- Cafeteria Quality Inspection Audit Dec10Documento6 pagineCafeteria Quality Inspection Audit Dec10api-309301602Nessuna valutazione finora

- Cooking-Terms JeanDocumento22 pagineCooking-Terms Jeanjean fernandezNessuna valutazione finora

- Service Standard Training PlanDocumento9 pagineService Standard Training PlanQuy TranxuanNessuna valutazione finora

- FB Service Power Point Intro Ch5Documento26 pagineFB Service Power Point Intro Ch5Dian Maulid IINessuna valutazione finora

- Free Training For Full Tools of F&B ManagementDocumento48 pagineFree Training For Full Tools of F&B ManagementSPHM HospitalityNessuna valutazione finora

- Safe Work Practices Duties and Responsibilities Service StandardsDocumento35 pagineSafe Work Practices Duties and Responsibilities Service StandardsDr.Tony BettsNessuna valutazione finora

- BHM 402T PDFDocumento120 pagineBHM 402T PDFKamlesh HarbolaNessuna valutazione finora

- HT CoCU 1 F - B Hygiene and Work Safety PracticeDocumento9 pagineHT CoCU 1 F - B Hygiene and Work Safety PracticeAnien Margaret FranklingNessuna valutazione finora

- The Menu - GRT Hotels and ResortsDocumento85 pagineThe Menu - GRT Hotels and ResortsBalagurunathanNessuna valutazione finora

- Chapter 1 - Introduction To Food and Beverage Control SystemDocumento29 pagineChapter 1 - Introduction To Food and Beverage Control SystemNorsaedah100% (3)

- FOOD AND BEVERAGE COST CONTROL BKKDocumento28 pagineFOOD AND BEVERAGE COST CONTROL BKKstephanie de Lara100% (3)

- OB&L Term Report-16271Documento15 pagineOB&L Term Report-16271SZANessuna valutazione finora

- Training ManualDocumento13 pagineTraining ManualSZANessuna valutazione finora

- 10.1 Population of Pakistan: Pakistan Urban Rural CensusDocumento26 pagine10.1 Population of Pakistan: Pakistan Urban Rural CensusSZANessuna valutazione finora

- Accounting JacobHeiberg 2019Documento80 pagineAccounting JacobHeiberg 2019SZANessuna valutazione finora

- Clayton Watters MSW Notes - Dec-2009Documento25 pagineClayton Watters MSW Notes - Dec-2009SZANessuna valutazione finora

- Andrzej Mazur - MSW 2010 MSW Process V3Documento4 pagineAndrzej Mazur - MSW 2010 MSW Process V3SZANessuna valutazione finora

- John Rhoton's MSW Notes 2010Documento21 pagineJohn Rhoton's MSW Notes 2010SZANessuna valutazione finora

- Question # 01Documento15 pagineQuestion # 01SZANessuna valutazione finora

- Lecture 7 Income and SpendingDocumento30 pagineLecture 7 Income and SpendingSZANessuna valutazione finora

- Management AssignmentDocumento3 pagineManagement AssignmentSZANessuna valutazione finora

- Name ERP Quiz 1 Quiz 2 Quiz 3quiz 4quiz 5Documento8 pagineName ERP Quiz 1 Quiz 2 Quiz 3quiz 4quiz 5SZANessuna valutazione finora

- Business Finance Project: Lucky Cement: Group DDocumento12 pagineBusiness Finance Project: Lucky Cement: Group DSZANessuna valutazione finora

- CH 01Documento33 pagineCH 01SZANessuna valutazione finora

- Chapter 1 Introduction: Multiple-Choice QuestionsDocumento192 pagineChapter 1 Introduction: Multiple-Choice QuestionsSZANessuna valutazione finora

- Mid Term Exam Part BDocumento1 paginaMid Term Exam Part BSyed Irtiza HaiderNessuna valutazione finora

- MM Course Evaluation SheetDocumento1 paginaMM Course Evaluation SheetSZANessuna valutazione finora

- ECON 511 Revision Questions On CH 7Documento4 pagineECON 511 Revision Questions On CH 7SZANessuna valutazione finora

- Asian Continental Pvt. Limited - Squad: Ibtihaj Siddiqui Tahir Saleh (C) Syed Ahmer Shad Waheed Hussain Fazal MirajDocumento1 paginaAsian Continental Pvt. Limited - Squad: Ibtihaj Siddiqui Tahir Saleh (C) Syed Ahmer Shad Waheed Hussain Fazal MirajSZANessuna valutazione finora

- Page 173Documento2 paginePage 173SZANessuna valutazione finora

- Managerial Economics ECO 502 Sbs - Mba / MSC: Submission Date: 12 March, 2020Documento27 pagineManagerial Economics ECO 502 Sbs - Mba / MSC: Submission Date: 12 March, 2020SZANessuna valutazione finora

- Silo - Tips - Demand Supply and Market Equilibrium PDFDocumento30 pagineSilo - Tips - Demand Supply and Market Equilibrium PDFSZANessuna valutazione finora

- Financial Model: Prepared By: The Marquee GroupDocumento16 pagineFinancial Model: Prepared By: The Marquee GroupSZA100% (1)

- Q&P CH 7 PDFDocumento1 paginaQ&P CH 7 PDFSZANessuna valutazione finora

- 31 (2) Sbi and IciciDocumento6 pagine31 (2) Sbi and IciciShyla PascalNessuna valutazione finora

- ITC Covered Call Option Strategy - 24112020-1606213764Documento3 pagineITC Covered Call Option Strategy - 24112020-1606213764Bobby TNessuna valutazione finora

- 3Q 2018 KPAL Steadfast+Marine+TbkDocumento82 pagine3Q 2018 KPAL Steadfast+Marine+Tbkangga andi ardiansyahNessuna valutazione finora

- Product Services Feasibility Analysis Marketing EssayDocumento4 pagineProduct Services Feasibility Analysis Marketing Essayvikram100% (1)

- Third Attempt, Full Research ProposalDocumento15 pagineThird Attempt, Full Research ProposalsenayNessuna valutazione finora

- McqsDocumento2 pagineMcqsMuhammad AhmedNessuna valutazione finora

- 2.3 Guidelines On 2-Column JournalDocumento2 pagine2.3 Guidelines On 2-Column Journalchristan tizonNessuna valutazione finora

- Introduction To The Andy Elliott Trainingw22Documento5 pagineIntroduction To The Andy Elliott Trainingw22Carlos Parra RavenNessuna valutazione finora

- Consumer Protection Act 2019Documento4 pagineConsumer Protection Act 2019devangNessuna valutazione finora

- Cardholder Copy Cardholder Copy: No Refund No RefundDocumento1 paginaCardholder Copy Cardholder Copy: No Refund No RefundKenneth GonzalesNessuna valutazione finora

- Dispute Form1Documento3 pagineDispute Form1Raymond DomingoNessuna valutazione finora

- AKT - 2023-04-04 - Franchise Disclosure DocumentDocumento243 pagineAKT - 2023-04-04 - Franchise Disclosure DocumentFuzzy PandaNessuna valutazione finora

- Roll No 34 & 35 AssigmentDocumento3 pagineRoll No 34 & 35 AssigmentRitikaNessuna valutazione finora

- Handling Customer Complaints (Customer Service)Documento2 pagineHandling Customer Complaints (Customer Service)Alan CarranzaNessuna valutazione finora

- Audit of Intangibles - AudProb SolutionDocumento13 pagineAudit of Intangibles - AudProb SolutionPaula De RuedaNessuna valutazione finora

- A Economics Gr. 12 Monopoly PresentationDocumento22 pagineA Economics Gr. 12 Monopoly PresentationHari prakarsh NimiNessuna valutazione finora

- Types of Enterprenures - MICRODocumento1 paginaTypes of Enterprenures - MICRONeelmaniNessuna valutazione finora

- Chap 005Documento153 pagineChap 005Kim NgânNessuna valutazione finora

- Prepared By: Jilly Boy G. Bruno Jr. and Jerome Marquez (Set A) - 1Documento8 paginePrepared By: Jilly Boy G. Bruno Jr. and Jerome Marquez (Set A) - 1BSIT 1A Yancy CaliganNessuna valutazione finora

- Instant Download Ebook PDF Financial and Managerial Accounting 3rd Edition by Jerry J Weygandt PDF ScribdDocumento47 pagineInstant Download Ebook PDF Financial and Managerial Accounting 3rd Edition by Jerry J Weygandt PDF Scribdmaurice.nesbit229100% (40)

- Cross-Cultural Negotiations - Almond Chemical Case AnalysisDocumento15 pagineCross-Cultural Negotiations - Almond Chemical Case AnalysisSafa AamirNessuna valutazione finora

- (TOEIC650) Exam Practice 1 (16 Bản)Documento10 pagine(TOEIC650) Exam Practice 1 (16 Bản)Hải YếnNessuna valutazione finora

- Consort Utilizing Consolidation To Lower Transport CostsDocumento12 pagineConsort Utilizing Consolidation To Lower Transport CostsDenis Mendoza QuispeNessuna valutazione finora

- Electronic - Banking and Customer Satisfaction in Greece - The Case of Piraeus BankDocumento15 pagineElectronic - Banking and Customer Satisfaction in Greece - The Case of Piraeus BankImtiaz MasroorNessuna valutazione finora

- Overview of BSI and Standardisation (Smart Cities & Big Data)Documento15 pagineOverview of BSI and Standardisation (Smart Cities & Big Data)ThanhNessuna valutazione finora

- International Marketing MCQDocumento5 pagineInternational Marketing MCQTan SinghNessuna valutazione finora

- Revision Practice PaperDocumento10 pagineRevision Practice Paperbehlolahmad7Nessuna valutazione finora

- Designing An Information Management System For OLA A Information System Management Presentation Report by Aditya KhandelwalDocumento19 pagineDesigning An Information Management System For OLA A Information System Management Presentation Report by Aditya KhandelwalAditya Khandelwal100% (2)

- Director Marketing Communications Brand in Washington DC Resume Susan SpaldingDocumento2 pagineDirector Marketing Communications Brand in Washington DC Resume Susan SpaldingSusanSpaldingNessuna valutazione finora

- Vistara - Pepper - Content PlanDocumento50 pagineVistara - Pepper - Content PlanKishan PanpaliyaNessuna valutazione finora