Potrebbero piacerti anche

- Shoe Dog: A Memoir by the Creator of NikeDa EverandShoe Dog: A Memoir by the Creator of NikeValutazione: 4.5 su 5 stelle4.5/5 (537)

- CIAP-PCAB Inquiry and Customer Complain Form (PCAB-PAD-ICC-F01) - 0 PDFDocumento1 paginaCIAP-PCAB Inquiry and Customer Complain Form (PCAB-PAD-ICC-F01) - 0 PDFEcosense TechnologiesNessuna valutazione finora

- Grit: The Power of Passion and PerseveranceDa EverandGrit: The Power of Passion and PerseveranceValutazione: 4 su 5 stelle4/5 (587)

- Recommended Specifications For CCTV 0408Documento11 pagineRecommended Specifications For CCTV 0408Ecosense TechnologiesNessuna valutazione finora

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDa EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceValutazione: 4 su 5 stelle4/5 (894)

- Recommended For CCTV PDFDocumento11 pagineRecommended For CCTV PDFEcosense TechnologiesNessuna valutazione finora

- The Yellow House: A Memoir (2019 National Book Award Winner)Da EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Valutazione: 4 su 5 stelle4/5 (98)

- Recommended Specifications For CCTV 0408Documento11 pagineRecommended Specifications For CCTV 0408Ecosense TechnologiesNessuna valutazione finora

- The Little Book of Hygge: Danish Secrets to Happy LivingDa EverandThe Little Book of Hygge: Danish Secrets to Happy LivingValutazione: 3.5 su 5 stelle3.5/5 (399)

- How To Register A Sole Proprietor Business in The PhilippinesDocumento5 pagineHow To Register A Sole Proprietor Business in The PhilippinesEcosense TechnologiesNessuna valutazione finora

- On Fire: The (Burning) Case for a Green New DealDa EverandOn Fire: The (Burning) Case for a Green New DealValutazione: 4 su 5 stelle4/5 (73)

- RS Means Estimating Cost Ch4Documento33 pagineRS Means Estimating Cost Ch4Krish DoodnauthNessuna valutazione finora

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDa EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeValutazione: 4 su 5 stelle4/5 (5794)

- Cost Estimation Concepts and Methodology GuideDocumento45 pagineCost Estimation Concepts and Methodology GuideRamphani Nunna100% (2)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDa EverandNever Split the Difference: Negotiating As If Your Life Depended On ItValutazione: 4.5 su 5 stelle4.5/5 (838)

- Recommended Specifications For CCTV 0408Documento11 pagineRecommended Specifications For CCTV 0408Ecosense TechnologiesNessuna valutazione finora

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDa EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureValutazione: 4.5 su 5 stelle4.5/5 (474)

- Philgeps - Ecosense Technologies PDFDocumento3 paginePhilgeps - Ecosense Technologies PDFEcosense TechnologiesNessuna valutazione finora

- Blade Module 72 PolyDocumento2 pagineBlade Module 72 PolyEcosense TechnologiesNessuna valutazione finora

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDa EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryValutazione: 3.5 su 5 stelle3.5/5 (231)

- Philgeps - Ecosense Technologies PDFDocumento3 paginePhilgeps - Ecosense Technologies PDFEcosense TechnologiesNessuna valutazione finora

- How the Five Forces Model Reveals Agriculture as a Better Investment than a Sari-Sari StoreDocumento6 pagineHow the Five Forces Model Reveals Agriculture as a Better Investment than a Sari-Sari StoreJoshua Eric Velasco DandalNessuna valutazione finora

- The Emperor of All Maladies: A Biography of CancerDa EverandThe Emperor of All Maladies: A Biography of CancerValutazione: 4.5 su 5 stelle4.5/5 (271)

- Advertising Plan Outline 0217 PDFDocumento3 pagineAdvertising Plan Outline 0217 PDFSushovan Bahadur AmatyaNessuna valutazione finora

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDa EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreValutazione: 4 su 5 stelle4/5 (1090)

- Konsult Assignment-2: VRIN Analysis of StarbucksDocumento4 pagineKonsult Assignment-2: VRIN Analysis of StarbucksSiddhant SinghNessuna valutazione finora

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDa EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyValutazione: 3.5 su 5 stelle3.5/5 (2219)

- Accounting For Installment SalesDocumento16 pagineAccounting For Installment SalesLeimonadeNessuna valutazione finora

- Team of Rivals: The Political Genius of Abraham LincolnDa EverandTeam of Rivals: The Political Genius of Abraham LincolnValutazione: 4.5 su 5 stelle4.5/5 (234)

- Cost Acc EPBM 4 Q PaperDocumento2 pagineCost Acc EPBM 4 Q PaperBhaskar BasakNessuna valutazione finora

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDa EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersValutazione: 4.5 su 5 stelle4.5/5 (344)

- Principles of Accounting IIDocumento72 paginePrinciples of Accounting IIAsaminow GirmaNessuna valutazione finora

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDa EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaValutazione: 4.5 su 5 stelle4.5/5 (265)

- Maharlika Ice Cream: Case StudyDocumento13 pagineMaharlika Ice Cream: Case StudyBhabi Barruga100% (1)

- Saint Paul School of Business and Law Managerial Accounting Final ExaminationDocumento2 pagineSaint Paul School of Business and Law Managerial Accounting Final ExaminationErin CruzNessuna valutazione finora

- Adobe Scan 7 Mar 2023Documento1 paginaAdobe Scan 7 Mar 2023Apurva KumarNessuna valutazione finora

- BSBMKG413 Task 2 AssessmentDocumento5 pagineBSBMKG413 Task 2 AssessmentnattyNessuna valutazione finora

- Elan EPIC - NEWDocumento35 pagineElan EPIC - NEWKaran MehtaNessuna valutazione finora

- IBUS 305 Lecture 2 - Managing Industry CompetitionDocumento3 pagineIBUS 305 Lecture 2 - Managing Industry Competitionmohit verrmaNessuna valutazione finora

- The Unwinding: An Inner History of the New AmericaDa EverandThe Unwinding: An Inner History of the New AmericaValutazione: 4 su 5 stelle4/5 (45)

- Managerial Accounting and Cost Concept Continuation Lesson Proper: The Analysis of Mixed CostsDocumento5 pagineManagerial Accounting and Cost Concept Continuation Lesson Proper: The Analysis of Mixed CostsGladymae MaggayNessuna valutazione finora

- Merchandise Budget Plan - Class ExcerciseDocumento1 paginaMerchandise Budget Plan - Class ExcerciseRAHUL KUMARNessuna valutazione finora

- Lean and JIT McdonaldsDocumento10 pagineLean and JIT McdonaldsHarshal Naik100% (2)

- Introduction To Marketing Management: Learning OutcomesDocumento9 pagineIntroduction To Marketing Management: Learning OutcomesNorhailaNessuna valutazione finora

- Johnson Turnaround Case Study AnalysisDocumento20 pagineJohnson Turnaround Case Study AnalysisMohamad Afif ShafiqNessuna valutazione finora

- Atlantic Computer: Competitive Pricing for Bundled Hardware and SoftwareDocumento5 pagineAtlantic Computer: Competitive Pricing for Bundled Hardware and Softwareilltutmish100% (2)

- Marketing ManagementDocumento328 pagineMarketing Managementlatsek50% (4)

- PCA Presentation - Abuse of Dominance 2Documento12 paginePCA Presentation - Abuse of Dominance 2Giuliana FloresNessuna valutazione finora

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)Da EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Valutazione: 4.5 su 5 stelle4.5/5 (119)

- Surabhi 1Documento20 pagineSurabhi 1Chingith RamakrishnanNessuna valutazione finora

- InvoiceDocumento1 paginaInvoiceEdulent FoundationNessuna valutazione finora

- Business Model Canvas Ent300Documento10 pagineBusiness Model Canvas Ent300Nur Afiqah100% (5)

- Associate Degree of Accounting: Examination Question BookletDocumento11 pagineAssociate Degree of Accounting: Examination Question BookletfernandarvNessuna valutazione finora

- Merchandising: Apparel Manufacturing: Sewn Product Analysis, 4/EDocumento17 pagineMerchandising: Apparel Manufacturing: Sewn Product Analysis, 4/Evishnuvardhinikj100% (1)

- Student's Roll No: A16 Student's Reg. No: 11906130Documento7 pagineStudent's Roll No: A16 Student's Reg. No: 11906130Prateek SehgalNessuna valutazione finora

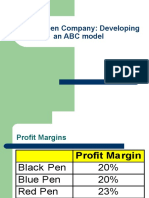

- Classic Pen Company: Developing An ABC ModelDocumento22 pagineClassic Pen Company: Developing An ABC Modeljk kumarNessuna valutazione finora

- Balance Between Fixed and Variable Compensation For Sales PeopleDocumento2 pagineBalance Between Fixed and Variable Compensation For Sales PeopleNazibul IslamNessuna valutazione finora

- Audit Risk NotesDocumento14 pagineAudit Risk NotesRana NadeemNessuna valutazione finora

- Her Body and Other Parties: StoriesDa EverandHer Body and Other Parties: StoriesValutazione: 4 su 5 stelle4/5 (821)

- Retail Service Management in the PhilippinesDocumento9 pagineRetail Service Management in the PhilippinesJovy DelaCruzNessuna valutazione finora