Potrebbero piacerti anche

- New Asit Ekka, Mba-Project Report @ucbDocumento71 pagineNew Asit Ekka, Mba-Project Report @ucbASIT EKKANessuna valutazione finora

- Impact of Deposit Mobilization On The Profitability of Laxmi Bank Limited by Nisha Thapa MagarDocumento49 pagineImpact of Deposit Mobilization On The Profitability of Laxmi Bank Limited by Nisha Thapa Magarparajuli2001kuNessuna valutazione finora

- Non Performing Assets in SBI GroupDocumento59 pagineNon Performing Assets in SBI GroupNavjinder Kaur67% (6)

- Project Report On Impact of NPA in The Performance of Financial InstitutionDocumento96 pagineProject Report On Impact of NPA in The Performance of Financial InstitutionManu Yuvi100% (1)

- Project VarshithaDocumento74 pagineProject VarshithaChandrika ChamsNessuna valutazione finora

- Keshav Mandal (Risk and Return of Sanima Bank)Documento31 pagineKeshav Mandal (Risk and Return of Sanima Bank)archanamandal667Nessuna valutazione finora

- Mitesh ProjectDocumento67 pagineMitesh ProjectMitesh Prajapati 7765Nessuna valutazione finora

- "Study On Loan and Credit Facility at SDCC Bank, Rourkela ": Summer Internship Project Report OnDocumento81 pagine"Study On Loan and Credit Facility at SDCC Bank, Rourkela ": Summer Internship Project Report OnASIT EKKANessuna valutazione finora

- Softcopy DOCUNMENT NPADocumento63 pagineSoftcopy DOCUNMENT NPAAditi KedariNessuna valutazione finora

- Internship Report-FinalDocumento48 pagineInternship Report-FinalShamim BaadshahNessuna valutazione finora

- Project Report On NPA and Its Impact On JK BankDocumento44 pagineProject Report On NPA and Its Impact On JK BankHuza if50% (2)

- Impact of Liquidity Management On Financial Performance of Nabil Bank LimitedDocumento23 pagineImpact of Liquidity Management On Financial Performance of Nabil Bank LimitedToran UpadhyayNessuna valutazione finora

- Mitesh Prajapati MB20023 (Project Report)Documento66 pagineMitesh Prajapati MB20023 (Project Report)Mitesh prajapatiNessuna valutazione finora

- Deposit Analysis of Kumari Bank Limited A Project Work Report - PDF - ConvertDocumento13 pagineDeposit Analysis of Kumari Bank Limited A Project Work Report - PDF - ConvertReshma ParweenNessuna valutazione finora

- A Research Report On "Foreign Exchange Operations" atDocumento68 pagineA Research Report On "Foreign Exchange Operations" atParth GandhiNessuna valutazione finora

- Project Report On NPA and Its Impact On JK BankDocumento61 pagineProject Report On NPA and Its Impact On JK BankHuza ifNessuna valutazione finora

- Account Project by PradipDocumento22 pagineAccount Project by Pradipnirajanthapa335Nessuna valutazione finora

- Mahalaxmi Bikash Bank ReportDocumento45 pagineMahalaxmi Bikash Bank ReportDeep MeditationNessuna valutazione finora

- Financial Performance of Kumari Bank Limited: Summitted byDocumento10 pagineFinancial Performance of Kumari Bank Limited: Summitted byAngbuhang Sushil Leemboo100% (1)

- Research ReportDocumento29 pagineResearch ReportRipesh AdhikariNessuna valutazione finora

- Internship Report - PDF P03793Documento60 pagineInternship Report - PDF P03793sam williamNessuna valutazione finora

- Rashid Solanki Roll No. 294 Bandhan Bank Final Year ProjectDocumento60 pagineRashid Solanki Roll No. 294 Bandhan Bank Final Year Projectsarah IsharatNessuna valutazione finora

- A Case Study On Npa 2.o PDFDocumento43 pagineA Case Study On Npa 2.o PDFAditya RoyNessuna valutazione finora

- Analysis of Deposit Schemes and Investment Modes of A Commercial Bank: A Study On Pubali Bank Limited, Chakbazar Branch, Chattogram"Documento64 pagineAnalysis of Deposit Schemes and Investment Modes of A Commercial Bank: A Study On Pubali Bank Limited, Chakbazar Branch, Chattogram"akash creationNessuna valutazione finora

- A Presentation On CREDIT APPRISAL FinalDocumento37 pagineA Presentation On CREDIT APPRISAL FinalNaveena ShankaraNessuna valutazione finora

- Proposal Mandip Labh Bbs 4th YearDocumento54 pagineProposal Mandip Labh Bbs 4th YearbinuNessuna valutazione finora

- Naveen MBA ProjectDocumento57 pagineNaveen MBA ProjectNaveen DasNessuna valutazione finora

- An Overview of Credit Appresal Process With Special Reference To Differnent Loans Offer by Indian BankDocumento86 pagineAn Overview of Credit Appresal Process With Special Reference To Differnent Loans Offer by Indian BankAbhinandan SahooNessuna valutazione finora

- Himalayan Bank Limited Internship ReportDocumento101 pagineHimalayan Bank Limited Internship ReportHossen M M50% (2)

- Mb206250-Shaik SafiullaDocumento42 pagineMb206250-Shaik Safiullakathirvelu0033Nessuna valutazione finora

- Financial Analysis ReportDocumento63 pagineFinancial Analysis ReportNabilaNessuna valutazione finora

- A Case Study of Financial Performance Kumari Bank Limeted: Binita JoshiDocumento46 pagineA Case Study of Financial Performance Kumari Bank Limeted: Binita JoshiBinita JoshiNessuna valutazione finora

- Dipanshu Mba ProjectDocumento72 pagineDipanshu Mba Projectn17mahey09Nessuna valutazione finora

- A Project: "On Impact of Covid 19 Pandemic On Banking & Financial Sector and Present Performance"Documento80 pagineA Project: "On Impact of Covid 19 Pandemic On Banking & Financial Sector and Present Performance"sanjay carNessuna valutazione finora

- Financial Performance Analysis of Kotak Mahindra BankDocumento60 pagineFinancial Performance Analysis of Kotak Mahindra Bankvaibhav pachputeNessuna valutazione finora

- Anu Kafle Report Bbs 4th YearDocumento17 pagineAnu Kafle Report Bbs 4th Yeartek bhattNessuna valutazione finora

- Project - Credit Risk ManagementDocumento56 pagineProject - Credit Risk ManagementTareq AlamNessuna valutazione finora

- CERTIFICATEDocumento31 pagineCERTIFICATEShanawaz ArifNessuna valutazione finora

- Working Capital Management of Nic Asia Bank LTD.: A Project ReportDocumento38 pagineWorking Capital Management of Nic Asia Bank LTD.: A Project ReportYutsarga Thiago ShresthaNessuna valutazione finora

- SIP PROJECT Final RAVIDocumento49 pagineSIP PROJECT Final RAVIRavi KhalkarNessuna valutazione finora

- Vaishnavi Dandekar - Financial Performance Commercial BankDocumento67 pagineVaishnavi Dandekar - Financial Performance Commercial BankMitesh Prajapati 7765Nessuna valutazione finora

- Pro Gandhi Final 1Documento79 paginePro Gandhi Final 1Adapaka SahithiNessuna valutazione finora

- Credit Risk SiDocumento90 pagineCredit Risk SiSampath SanguNessuna valutazione finora

- Retika SahaniDocumento84 pagineRetika Sahaniravi singhNessuna valutazione finora

- Summer Report Idbi (Avinash)Documento84 pagineSummer Report Idbi (Avinash)Govind KushwahaNessuna valutazione finora

- Performance Analysis of Mutual Trust BanDocumento23 paginePerformance Analysis of Mutual Trust BanEmran HossainNessuna valutazione finora

- Syed Mufrad Ahmed BBA 1802019043 Internship ReportDocumento68 pagineSyed Mufrad Ahmed BBA 1802019043 Internship ReportShopon KhanNessuna valutazione finora

- Global IME BankDocumento29 pagineGlobal IME BankSujan Bajracharya100% (2)

- Asset and Liabilities Management of UCO BANKDocumento62 pagineAsset and Liabilities Management of UCO BANKSaroj Dash100% (1)

- A Project Report On Financing Working Capital at PNBDocumento52 pagineA Project Report On Financing Working Capital at PNBMudit GuptaNessuna valutazione finora

- SIP ReportDocumento39 pagineSIP ReportAditya ShankarNessuna valutazione finora

- Financial Inclusion for Micro, Small, and Medium Enterprises in Kazakhstan: ADB Support for Regional Cooperation and Integration across Asia and the Pacific during Unprecedented Challenge and ChangeDa EverandFinancial Inclusion for Micro, Small, and Medium Enterprises in Kazakhstan: ADB Support for Regional Cooperation and Integration across Asia and the Pacific during Unprecedented Challenge and ChangeNessuna valutazione finora

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Da EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Nessuna valutazione finora

- Asia Small and Medium-Sized Enterprise Monitor 2020: Volume IV: Technical Note—Designing a Small and Medium-Sized Enterprise Development IndexDa EverandAsia Small and Medium-Sized Enterprise Monitor 2020: Volume IV: Technical Note—Designing a Small and Medium-Sized Enterprise Development IndexNessuna valutazione finora

- Regional Rural Banks of India: Evolution, Performance and ManagementDa EverandRegional Rural Banks of India: Evolution, Performance and ManagementNessuna valutazione finora

- Realizing the Potential of Public–Private Partnerships to Advance Asia's Infrastructure DevelopmentDa EverandRealizing the Potential of Public–Private Partnerships to Advance Asia's Infrastructure DevelopmentNessuna valutazione finora

- Public Financing for Small and Medium-Sized Enterprises: The Cases of the Republic of Korea and the United StatesDa EverandPublic Financing for Small and Medium-Sized Enterprises: The Cases of the Republic of Korea and the United StatesNessuna valutazione finora

- Strengthening Partnerships: Accountability Mechanism Annual Report 2014Da EverandStrengthening Partnerships: Accountability Mechanism Annual Report 2014Nessuna valutazione finora

- Public Financial Management Systems—Sri Lanka: Key Elements from a Financial Management PerspectiveDa EverandPublic Financial Management Systems—Sri Lanka: Key Elements from a Financial Management PerspectiveNessuna valutazione finora

- Finding Balance 2019: Benchmarking the Performance of State-Owned Banks in the PacificDa EverandFinding Balance 2019: Benchmarking the Performance of State-Owned Banks in the PacificNessuna valutazione finora

- Fig No. 2.1: Trend Line of Current Ratio 2.1.2 Quick RatioDocumento1 paginaFig No. 2.1: Trend Line of Current Ratio 2.1.2 Quick RatioShivam KarnNessuna valutazione finora

- Table: 2.7 Earning Per Share of Mega Bank Ltd. Form FY 2070/71 To 2074/75Documento1 paginaTable: 2.7 Earning Per Share of Mega Bank Ltd. Form FY 2070/71 To 2074/75Shivam KarnNessuna valutazione finora

- B) For Corporate Banking: AaoluayDocumento2 pagineB) For Corporate Banking: AaoluayShivam KarnNessuna valutazione finora

- Results and Analysis: Chapter - TwoDocumento2 pagineResults and Analysis: Chapter - TwoShivam KarnNessuna valutazione finora

- Mon - Jeujjaiem AaoiuayDocumento1 paginaMon - Jeujjaiem AaoiuayShivam KarnNessuna valutazione finora

- Year Growth Non-Interest Bearing Deposit % Growth Current Year Previous YearDocumento2 pagineYear Growth Non-Interest Bearing Deposit % Growth Current Year Previous YearShivam KarnNessuna valutazione finora

- 5 - Jewjaiem: Mon OaolusmDocumento1 pagina5 - Jewjaiem: Mon OaolusmShivam KarnNessuna valutazione finora

- 6034Documento94 pagine6034Shivam KarnNessuna valutazione finora

- Project Report of Banking InsuranceDocumento30 pagineProject Report of Banking InsuranceShivam KarnNessuna valutazione finora

- Sahayogi Vikas Bank LimitedDocumento2 pagineSahayogi Vikas Bank LimitedShivam KarnNessuna valutazione finora

- Project Nabil Bank-EditedDocumento34 pagineProject Nabil Bank-EditedShivam KarnNessuna valutazione finora

- Year Growth Interest Bearing Deposit % Growth Current Year Previous YearDocumento2 pagineYear Growth Interest Bearing Deposit % Growth Current Year Previous YearShivam KarnNessuna valutazione finora

- Securities Markets and Regulation of Securities Markets in NepalDocumento50 pagineSecurities Markets and Regulation of Securities Markets in NepalShivam KarnNessuna valutazione finora

- A Study Report On Textile Clothing Sectors in NepalDocumento3 pagineA Study Report On Textile Clothing Sectors in NepalShivam KarnNessuna valutazione finora

- Securities Markets and Regulation of Securities Markets in NepalDocumento50 pagineSecurities Markets and Regulation of Securities Markets in NepalShivam KarnNessuna valutazione finora

- New Microsoft Office Word DocumentDocumento3 pagineNew Microsoft Office Word DocumentShivam KarnNessuna valutazione finora

- KR - Sharma - PHD - Thesis - January - 2012 - Single PDFDocumento304 pagineKR - Sharma - PHD - Thesis - January - 2012 - Single PDFShivam KarnNessuna valutazione finora

- Credit Management Report On SIBL Bank - DoDocumento47 pagineCredit Management Report On SIBL Bank - DoShivam KarnNessuna valutazione finora

- Determinants of Disclosure Level of Related Party Transactions in IndonesiaDocumento25 pagineDeterminants of Disclosure Level of Related Party Transactions in IndonesiafidelaluthfianaNessuna valutazione finora

- Axis BankDocumento14 pagineAxis BankNikhil Kapoor50% (2)

- Indian Stock Market PDFDocumento14 pagineIndian Stock Market PDFDeepthi Thatha58% (12)

- Research Paper On Financial Analysis of BanksDocumento5 pagineResearch Paper On Financial Analysis of Banksc9rvcwhf100% (1)

- Resume and Cover Letter TemplateDocumento5 pagineResume and Cover Letter TemplateManoj ThomasNessuna valutazione finora

- 500 - Visa Document Checklist - 20211105Documento6 pagine500 - Visa Document Checklist - 20211105Mildred MendozaNessuna valutazione finora

- Goldman Future of Finance - Payment EcosystemsDocumento87 pagineGoldman Future of Finance - Payment Ecosystemsnirav kakariyaNessuna valutazione finora

- 11.1valuation of Intellectual Property Assets PDFDocumento31 pagine11.1valuation of Intellectual Property Assets PDFShivam Anand100% (1)

- ACBS Commercial Loan System Fact SheetDocumento4 pagineACBS Commercial Loan System Fact SheetRajitNessuna valutazione finora

- The Foreign Exchange Management Act, 1999: Legislative HistoryDocumento26 pagineThe Foreign Exchange Management Act, 1999: Legislative HistoryPrince VenkatNessuna valutazione finora

- Livro BegeDocumento32 pagineLivro BegeDinheirama.comNessuna valutazione finora

- Adna Steel - Abb CamDocumento41 pagineAdna Steel - Abb CamShivaniNessuna valutazione finora

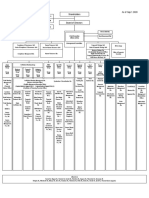

- PDF of Bank OrganogramDocumento1 paginaPDF of Bank OrganogramAntar ShaddadNessuna valutazione finora

- Draft Business Plan TemplateDocumento6 pagineDraft Business Plan TemplateSanket MoteNessuna valutazione finora

- Duplicate Gat Result Card S T NS T N: Personal InformationDocumento2 pagineDuplicate Gat Result Card S T NS T N: Personal InformationArif Ullah MarwatNessuna valutazione finora

- BFIN Week Wewe 1-9 11-18Documento52 pagineBFIN Week Wewe 1-9 11-18Mark Louie SuarezNessuna valutazione finora

- ENG Merchant 4275Documento7 pagineENG Merchant 4275thirdNessuna valutazione finora

- Surefire Sales Closing Techniqu LesDane PDFDocumento200 pagineSurefire Sales Closing Techniqu LesDane PDFSarah A. Lopez100% (1)

- Phrases AbroadDocumento20 paginePhrases Abroadᴍᴀʀɪᴀɴᴀ ᴍᴀʀɪᴀɴᴀNessuna valutazione finora

- IFIC Digital Banking Terms and ConditionsDocumento13 pagineIFIC Digital Banking Terms and Conditionstoyabcu10Nessuna valutazione finora

- Institutions International Financial: by Sachin N. ShettyDocumento33 pagineInstitutions International Financial: by Sachin N. ShettyPrasseedha Raghavan100% (1)

- FINACC1 - Cash and Cash Equivalents + ReceivablesDocumento3 pagineFINACC1 - Cash and Cash Equivalents + ReceivablesJerico DungcaNessuna valutazione finora

- Essay 1 - Economic Development in Medieval EuropeDocumento2 pagineEssay 1 - Economic Development in Medieval EuropeSergey GorbachovNessuna valutazione finora

- Experience and Satisfaction of Bancassurance Customers of SBI - Final AbhijeetDocumento97 pagineExperience and Satisfaction of Bancassurance Customers of SBI - Final AbhijeetGanesh TiwariNessuna valutazione finora

- What Is A Merchant Account?Documento2 pagineWhat Is A Merchant Account?michael amoryNessuna valutazione finora

- Ghaziabad Telecom District: Account SummaryDocumento1 paginaGhaziabad Telecom District: Account SummaryVinee SharmaNessuna valutazione finora

- Rythu Bandhu Form in TeluguDocumento5 pagineRythu Bandhu Form in TeluguRajashekar ChNessuna valutazione finora

- Medical Reimbursement Scheme For Bank Officers - Employees Under 10th BPS - Banking SchoolDocumento7 pagineMedical Reimbursement Scheme For Bank Officers - Employees Under 10th BPS - Banking SchoolNadeem MalekNessuna valutazione finora

- Which of The Following Is Not An Essential Characteristic of A LiabilityDocumento31 pagineWhich of The Following Is Not An Essential Characteristic of A LiabilityJam PotutanNessuna valutazione finora

- Artifact 5a - Guidelines For Filling PF Withdrawal Form TCSDocumento3 pagineArtifact 5a - Guidelines For Filling PF Withdrawal Form TCSAmy Brady100% (3)