Potrebbero piacerti anche

- Intermediate Accounting ExamDocumento6 pagineIntermediate Accounting ExamPISONANTA KRISETIANessuna valutazione finora

- KsksDocumento8 pagineKsksMARICEL URBINANessuna valutazione finora

- BANGI, Joshua Celton - Assign2.Documento7 pagineBANGI, Joshua Celton - Assign2.Joshua BangiNessuna valutazione finora

- Problem 6-1: Interest Expense Present ValueDocumento3 pagineProblem 6-1: Interest Expense Present ValueAngieNessuna valutazione finora

- Chapter 24 Answer KeyDocumento3 pagineChapter 24 Answer KeyShane TabunggaoNessuna valutazione finora

- 6727 Statement of Financial PositionDocumento3 pagine6727 Statement of Financial PositionJane ValenciaNessuna valutazione finora

- FAR1Documento736 pagineFAR1Muhammad AwanNessuna valutazione finora

- 3.3.1 Notes and Loans Receivable Receivable FinancingDocumento14 pagine3.3.1 Notes and Loans Receivable Receivable FinancingJan Nelson BayanganNessuna valutazione finora

- Aud Prob LiabDocumento2 pagineAud Prob LiabKaren Yvonne R. BilonNessuna valutazione finora

- Acct 4010 Ch2-Handout-SolutionDocumento4 pagineAcct 4010 Ch2-Handout-Solutionlokyee801mikiNessuna valutazione finora

- To Record The Issuance of The Notes: Problem 6-1Documento4 pagineTo Record The Issuance of The Notes: Problem 6-1Danica RamosNessuna valutazione finora

- ACCT101 YUNLEE SOLUTIONS Ch05Documento19 pagineACCT101 YUNLEE SOLUTIONS Ch05KO YANG JINNessuna valutazione finora

- Instructor Questionaire AccountingDocumento4 pagineInstructor Questionaire AccountingjovelioNessuna valutazione finora

- Intermediate Accounting 2 Final ExamDocumento35 pagineIntermediate Accounting 2 Final ExamJEFFERSON CUTE97% (32)

- Defined Benefit Plan-Midnight CompanyDocumento2 pagineDefined Benefit Plan-Midnight CompanyDyenNessuna valutazione finora

- Investment in Associate ExercisesDocumento7 pagineInvestment in Associate ExercisesJo KeNessuna valutazione finora

- Week 1 PPT 2 Introduction To AccountingDocumento13 pagineWeek 1 PPT 2 Introduction To AccountingDinusha FernandoNessuna valutazione finora

- 07 Loan Receivable MCPDocumento4 pagine07 Loan Receivable MCPkyle mandaresioNessuna valutazione finora

- Midterm Practice QuestionsDocumento4 pagineMidterm Practice QuestionsGio RobakidzeNessuna valutazione finora

- AC4301 FinalExam 2020-21 SemA AnsDocumento9 pagineAC4301 FinalExam 2020-21 SemA AnslawlokyiNessuna valutazione finora

- Kelompok3 Tugas3 AKLDocumento4 pagineKelompok3 Tugas3 AKLsyifa fr100% (1)

- Tugas Penyelesaian 14 AIK - 0119101024 - Muhamad Adam Palmaleo - Kelas BDocumento23 pagineTugas Penyelesaian 14 AIK - 0119101024 - Muhamad Adam Palmaleo - Kelas BAdam PalmaleoNessuna valutazione finora

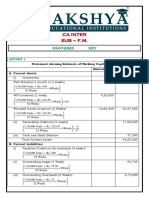

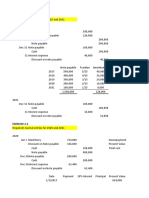

- Ca Inter-F.m.03-07-2023-KeyDocumento3 pagineCa Inter-F.m.03-07-2023-KeyChintuNessuna valutazione finora

- FAR - Final Preboard CPAR 92Documento14 pagineFAR - Final Preboard CPAR 92joyhhazelNessuna valutazione finora

- Asm 2 AcDocumento19 pagineAsm 2 AcNguyen Duc Quang (BTEC HN)Nessuna valutazione finora

- Ans: A) Journal Entry On Date of Issue Date Account DR CRDocumento4 pagineAns: A) Journal Entry On Date of Issue Date Account DR CRHumera AkbarNessuna valutazione finora

- Acc 102Documento3 pagineAcc 102Ike UzuNessuna valutazione finora

- Perpetual Bank: ReceivablesDocumento13 paginePerpetual Bank: ReceivablesYes ChannelNessuna valutazione finora

- Fra 3Documento7 pagineFra 3Subhajyoti MukhopadhyayNessuna valutazione finora

- Quiz 1.02 Cash and Cash Equivalents To Loan ImpairmentDocumento13 pagineQuiz 1.02 Cash and Cash Equivalents To Loan ImpairmentJohn Lexter MacalberNessuna valutazione finora

- Quiz 102 Cash and Cash Equivalents To Loan Impairment PDF FreeDocumento13 pagineQuiz 102 Cash and Cash Equivalents To Loan Impairment PDF FreeNashaNessuna valutazione finora

- Answer KeyDocumento9 pagineAnswer KeyDeepakshiNessuna valutazione finora

- ACC203 - AssignmentDocumento2 pagineACC203 - AssignmentHailsey WinterNessuna valutazione finora

- Mohsin Hassan Bba Iib BUS-19F-044 Principle of AccountingDocumento7 pagineMohsin Hassan Bba Iib BUS-19F-044 Principle of AccountingMohsin HassanNessuna valutazione finora

- PPE1&2Documento3 paginePPE1&2Kailah CalinogNessuna valutazione finora

- Cash Accrual Practice SetDocumento2 pagineCash Accrual Practice SetMa. Trixcy De VeraNessuna valutazione finora

- Cpa Review School of The Philippines ManilaDocumento2 pagineCpa Review School of The Philippines ManilaJoyce Anne DugayNessuna valutazione finora

- Intermediate Accounting 2: Financial LiabilitiesDocumento63 pagineIntermediate Accounting 2: Financial LiabilitiesLyca Mae CubangbangNessuna valutazione finora

- Cpa Review School of The Philippines ManilaDocumento2 pagineCpa Review School of The Philippines ManilaKyrie Gwynette OlarveNessuna valutazione finora

- Accounting GR 11 Acc T3 Wk7 Budgets ConsolidateDocumento5 pagineAccounting GR 11 Acc T3 Wk7 Budgets Consolidatesihlemooi3Nessuna valutazione finora

- Accounting ExamDocumento6 pagineAccounting Examgenn katherine gadunNessuna valutazione finora

- PART 4 - Opening BalancesDocumento2 paginePART 4 - Opening BalancesTabani RobertNessuna valutazione finora

- ACC101 Chapter1newDocumento16 pagineACC101 Chapter1newtazebachew birkuNessuna valutazione finora

- Module 5-NOTE PAYABLE AND DEBT RESTRUCTUREDocumento13 pagineModule 5-NOTE PAYABLE AND DEBT RESTRUCTUREJeanivyle Carmona100% (1)

- Comprehensive Quiz No. 007-Hyperinflation Current Cost Acctg - GROUP-3Documento4 pagineComprehensive Quiz No. 007-Hyperinflation Current Cost Acctg - GROUP-3Jericho VillalonNessuna valutazione finora

- Journal Entry ExampleDocumento52 pagineJournal Entry Examplesriram998983% (6)

- Bsib622 Fa 2 QPDocumento4 pagineBsib622 Fa 2 QPNoor AssignmentsNessuna valutazione finora

- Recording Adjustments For Revenues & Recording EquityDocumento7 pagineRecording Adjustments For Revenues & Recording Equitypratibha jaggan martinNessuna valutazione finora

- CH 10Documento32 pagineCH 10Gaurav KarkiNessuna valutazione finora

- Accounting Principles Assignment on Depreciation and Allowance for Doubtful AccountsDocumento7 pagineAccounting Principles Assignment on Depreciation and Allowance for Doubtful AccountsMohsin HassanNessuna valutazione finora

- 1ST Sem P.Y. Acct PaperDocumento30 pagine1ST Sem P.Y. Acct PaperSuraj KumarNessuna valutazione finora

- Far PreweekDocumento18 pagineFar PreweekHarvey OchoaNessuna valutazione finora

- LQ 1 - Set A Solution PDF Bonds (Finance) ADocumento2 pagineLQ 1 - Set A Solution PDF Bonds (Finance) AeaeNessuna valutazione finora

- Ida Ayu Koamang Sumi Antari (21021013) Tugas Bahasa Inggris 14Documento9 pagineIda Ayu Koamang Sumi Antari (21021013) Tugas Bahasa Inggris 14Ida ayu Komang Sumi AntariNessuna valutazione finora

- Problem 6-8 Answer A Savage CompanyDocumento6 pagineProblem 6-8 Answer A Savage CompanyJurie BalandacaNessuna valutazione finora

- Acct 4010 Ch2-Handout-QDocumento4 pagineAcct 4010 Ch2-Handout-Qlokyee801mikiNessuna valutazione finora

- Using Economic Indicators to Improve Investment AnalysisDa EverandUsing Economic Indicators to Improve Investment AnalysisValutazione: 3.5 su 5 stelle3.5/5 (1)

- One Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020Da EverandOne Year of Living with COVID-19: An Assessment of How ADB Members Fought the Pandemic in 2020Nessuna valutazione finora

- Asian Development Bank Trust Funds Report 2020: Includes Global and Special FundsDa EverandAsian Development Bank Trust Funds Report 2020: Includes Global and Special FundsNessuna valutazione finora

- Silven Industries, Which Manufactures and Sells A Highly Successful Line of Summer Lotions and Insect RepellentsDocumento5 pagineSilven Industries, Which Manufactures and Sells A Highly Successful Line of Summer Lotions and Insect RepellentsKailash KumarNessuna valutazione finora

- Napa Tours Co. Is A Travel Agency. The Nine Transactions Recorded by NapaDocumento2 pagineNapa Tours Co. Is A Travel Agency. The Nine Transactions Recorded by NapaKailash KumarNessuna valutazione finora

- The Alphabetical Listing Below Includes All of The Adjusted Account Balances of Battle CreekDocumento4 pagineThe Alphabetical Listing Below Includes All of The Adjusted Account Balances of Battle CreekKailash KumarNessuna valutazione finora

- Is A Construction Company Specializing in Custom PatiosDocumento8 pagineIs A Construction Company Specializing in Custom PatiosKailash KumarNessuna valutazione finora

- Calculate inventory balances, cost of goods sold, and net income with corrected inventory amountsDocumento3 pagineCalculate inventory balances, cost of goods sold, and net income with corrected inventory amountsKailash KumarNessuna valutazione finora

- Schrand Corporation PurchaseDocumento1 paginaSchrand Corporation PurchaseKailash KumarNessuna valutazione finora

- Jennys FroyoDocumento16 pagineJennys FroyoKailash Kumar100% (2)

- Alpha Corporation Issued 2,500 Shares of $4 Par Value Common Stock.Documento1 paginaAlpha Corporation Issued 2,500 Shares of $4 Par Value Common Stock.Kailash KumarNessuna valutazione finora

- Whispering-Air Is Selling A New Model of High-Efficiency Air ConditionerDocumento2 pagineWhispering-Air Is Selling A New Model of High-Efficiency Air ConditionerKailash KumarNessuna valutazione finora

- On April 1, 2018, Intel Issued $1,600,000 of 12% Face Value Bonds For $1,703,411.40.Documento3 pagineOn April 1, 2018, Intel Issued $1,600,000 of 12% Face Value Bonds For $1,703,411.40.Kailash KumarNessuna valutazione finora

- Crane Inc. Entered Into A Contract To Deliver One of Its Specialty Mowers To Kickapoo Landscaping CoDocumento1 paginaCrane Inc. Entered Into A Contract To Deliver One of Its Specialty Mowers To Kickapoo Landscaping CoKailash KumarNessuna valutazione finora

- Thompson Industrial Products Inc Is A DiversifiedDocumento4 pagineThompson Industrial Products Inc Is A DiversifiedKailash KumarNessuna valutazione finora

- Crane Inc. Entered Into A Contract To Deliver One of Its Specialty Mowers To Kickapoo Landscaping CoDocumento2 pagineCrane Inc. Entered Into A Contract To Deliver One of Its Specialty Mowers To Kickapoo Landscaping CoKailash KumarNessuna valutazione finora

- Pastore Drycleaners Has Capacity To Clean UpDocumento4 paginePastore Drycleaners Has Capacity To Clean UpKailash KumarNessuna valutazione finora

- O-Level Accounting Paper 2 Topical and yDocumento343 pagineO-Level Accounting Paper 2 Topical and yKailash Kumar100% (3)

- Adjusting Entry Pracyice Perry Company PaidDocumento1 paginaAdjusting Entry Pracyice Perry Company PaidKailash KumarNessuna valutazione finora

- On January 1, 20X5, Pirate Company Acquired All of The Outstanding Stock of Ship Inc.,Norwegian Company, ADocumento17 pagineOn January 1, 20X5, Pirate Company Acquired All of The Outstanding Stock of Ship Inc.,Norwegian Company, AKailash KumarNessuna valutazione finora

- Periodic Inventory Three MethodsDocumento2 paginePeriodic Inventory Three MethodsKailash KumarNessuna valutazione finora

- Prince Corporation Acquired 100 Percent of Sword CompanyDocumento2 paginePrince Corporation Acquired 100 Percent of Sword CompanyKailash Kumar50% (2)

- Calculating differential values and percentages from financial statementsDocumento2 pagineCalculating differential values and percentages from financial statementsKailash KumarNessuna valutazione finora

- Accounting entries for asset valuationDocumento2 pagineAccounting entries for asset valuationKailash KumarNessuna valutazione finora

- Industry Volume and Market Share Missing DataDocumento1 paginaIndustry Volume and Market Share Missing DataKailash KumarNessuna valutazione finora

- Diamond Hardware Uses The Periodic Inventory SystemDocumento7 pagineDiamond Hardware Uses The Periodic Inventory SystemKailash KumarNessuna valutazione finora

- Bracey Company Manufactures and Sells One ProductDocumento2 pagineBracey Company Manufactures and Sells One ProductKailash KumarNessuna valutazione finora

- Turcotte Corp Reported The Following Revenues and Cost of Goods Sodl AmountsDocumento1 paginaTurcotte Corp Reported The Following Revenues and Cost of Goods Sodl AmountsKailash KumarNessuna valutazione finora

- James Kimberley President of National Motors Receives A BonusDocumento1 paginaJames Kimberley President of National Motors Receives A BonusKailash KumarNessuna valutazione finora

- Kristen Lu Purchased A Used Automobile ForDocumento1 paginaKristen Lu Purchased A Used Automobile ForKailash KumarNessuna valutazione finora

- La Femme Accessories Inc Produces Womens HandbagsDocumento1 paginaLa Femme Accessories Inc Produces Womens HandbagsKailash KumarNessuna valutazione finora

- Bethany's Bicycle CorporationDocumento15 pagineBethany's Bicycle CorporationKailash Kumar100% (2)

- Project Financing AssignmentsDocumento17 pagineProject Financing AssignmentsAlemu OlikaNessuna valutazione finora

- Earnings Management in India: Managers' Fixation On Operating ProfitsDocumento27 pagineEarnings Management in India: Managers' Fixation On Operating ProfitsVaibhav KaushikNessuna valutazione finora

- Breaking The Time Barrier PDFDocumento70 pagineBreaking The Time Barrier PDFCalypso LearnerNessuna valutazione finora

- How To Write A Good Letter of Intent When Buying A Company?Documento4 pagineHow To Write A Good Letter of Intent When Buying A Company?Jose Antonio BarrosoNessuna valutazione finora

- Truth in Lending Act Requires Disclosure of Finance ChargesDocumento3 pagineTruth in Lending Act Requires Disclosure of Finance Chargesjeffprox69Nessuna valutazione finora

- Zillow 2Q22 Shareholders' LetterDocumento17 pagineZillow 2Q22 Shareholders' LetterGeekWireNessuna valutazione finora

- Internship Report (11504725) PDFDocumento39 pagineInternship Report (11504725) PDFpreetiNessuna valutazione finora

- Taxmann - Budget Highlights 2022-2023Documento42 pagineTaxmann - Budget Highlights 2022-2023Jinang JainNessuna valutazione finora

- Deco404 Public Finance Hindi PDFDocumento404 pagineDeco404 Public Finance Hindi PDFRaju Chouhan RajNessuna valutazione finora

- Agha Hassan AbdiDocumento28 pagineAgha Hassan Abdibilawal_scorpion0% (1)

- Entrepreneurial Law NotesDocumento70 pagineEntrepreneurial Law NotesPhebieon Mukwenha100% (1)

- Risk and Rates of Return: Multiple Choice: ConceptualDocumento79 pagineRisk and Rates of Return: Multiple Choice: ConceptualKatherine Cabading InocandoNessuna valutazione finora

- Business TransactionsDocumento6 pagineBusiness TransactionsMarlyn Joy Yacon100% (1)

- IPP Report PakistanDocumento296 pagineIPP Report PakistanALI100% (1)

- Vip No.8 - MeslDocumento4 pagineVip No.8 - Meslkj gandaNessuna valutazione finora

- Document ManagementDocumento55 pagineDocument Managementrtarak100% (1)

- Notes # 2 - Fundamentals of Real Estate Management PDFDocumento3 pagineNotes # 2 - Fundamentals of Real Estate Management PDFGessel Xan Lopez100% (2)

- 6,1 Manajemen Modal Kerja PDFDocumento14 pagine6,1 Manajemen Modal Kerja PDFIronaYurieNessuna valutazione finora

- T3-Sample Answers-Consideration PDFDocumento10 pagineT3-Sample Answers-Consideration PDF--bolabolaNessuna valutazione finora

- Mechanics of Futures MarketsDocumento42 pagineMechanics of Futures MarketsSidharth ChoudharyNessuna valutazione finora

- Bonds Payable PDFDocumento6 pagineBonds Payable PDFAnthony Tunying MantuhacNessuna valutazione finora

- IRS Updates The 2021 Child Tax Credit and Advance Child Tax Credit Frequently Asked QuestionsDocumento25 pagineIRS Updates The 2021 Child Tax Credit and Advance Child Tax Credit Frequently Asked QuestionsCrystal KleistNessuna valutazione finora

- Cash Flow Statements PDFDocumento101 pagineCash Flow Statements PDFSubbu ..100% (1)

- Rahma ConsutingDocumento6 pagineRahma ConsutingEko Firdausta TariganNessuna valutazione finora

- 03 BIWS Equity Value Enterprise ValueDocumento6 pagine03 BIWS Equity Value Enterprise ValuecarminatNessuna valutazione finora

- GEM/2022/B/2723659 Bid CorrigendumDocumento2 pagineGEM/2022/B/2723659 Bid CorrigendumAnmol JainNessuna valutazione finora

- How To Apply For A Rental Property - Rent - Ray White AscotDocumento2 pagineHow To Apply For A Rental Property - Rent - Ray White AscotRRWERERRNessuna valutazione finora

- Fundraising - Public Sector, Foundations and TrustsDocumento5 pagineFundraising - Public Sector, Foundations and TrustsLena HafizNessuna valutazione finora

- Contemporary Issues in Banking Sector in BangladeshDocumento8 pagineContemporary Issues in Banking Sector in Bangladeshangel100% (5)

- Sinhgad Institute of Management - Research TopicsDocumento17 pagineSinhgad Institute of Management - Research TopicsAnmol LimpaleNessuna valutazione finora