Potrebbero piacerti anche

- Engineering Econ FinalsDocumento10 pagineEngineering Econ FinalsIvan Morise AtienzaNessuna valutazione finora

- SSA BUS 5111 Financial Management Unit 1 Written Assignment 1Documento6 pagineSSA BUS 5111 Financial Management Unit 1 Written Assignment 1Charles Irikefe100% (2)

- Usin Activity-Based Costing (ABC) To Measure Profitability On A Commercial Loan Portfolio - Mehmet C. KocakulahDocumento19 pagineUsin Activity-Based Costing (ABC) To Measure Profitability On A Commercial Loan Portfolio - Mehmet C. KocakulahUmar Farooq Attari100% (2)

- Financial Accounting, 7e by Pfeiffer, Hanlon, Magee 2023, Solution Manual Chapter 1Documento25 pagineFinancial Accounting, 7e by Pfeiffer, Hanlon, Magee 2023, Solution Manual Chapter 1Test bank WorldNessuna valutazione finora

- Introduction To Financial Statements 1Documento22 pagineIntroduction To Financial Statements 1Sarbani Mishra100% (1)

- 703 - Finance For Managers - Azizul Hakem - Sub On 18 JulyDocumento10 pagine703 - Finance For Managers - Azizul Hakem - Sub On 18 JulyAzeezulNessuna valutazione finora

- Designing Financial IncentivesDocumento6 pagineDesigning Financial IncentivesPriyanka HarilelaNessuna valutazione finora

- Corporate Debt Restructuring: Concept, Assessment and Emerging IssuesDocumento7 pagineCorporate Debt Restructuring: Concept, Assessment and Emerging IssuesGaurav KukrejaNessuna valutazione finora

- Incentive Plan WWBDocumento6 pagineIncentive Plan WWBAdnanZiadatNessuna valutazione finora

- Financial Analysis of BOK (FIM)Documento33 pagineFinancial Analysis of BOK (FIM)ram binod yadavNessuna valutazione finora

- CAMELSDRAFTVIJAIDocumento49 pagineCAMELSDRAFTVIJAIMurali Balaji M CNessuna valutazione finora

- Accenture Tying The Knot Between Risk and Performance ManagementDocumento16 pagineAccenture Tying The Knot Between Risk and Performance Managementkinky72100% (1)

- Ebook Case Studies in Finance 7Th Edition Bruner Solutions Manual Full Chapter PDFDocumento37 pagineEbook Case Studies in Finance 7Th Edition Bruner Solutions Manual Full Chapter PDFfintanthamh4jtd100% (13)

- Ratio Analysis of HDFC FINALDocumento10 pagineRatio Analysis of HDFC FINALJAYKISHAN JOSHI100% (2)

- Risk Assessment Model For Assessing NBFCsAsset FiDocumento11 pagineRisk Assessment Model For Assessing NBFCsAsset FiNishit RelanNessuna valutazione finora

- June 2016: BY: ZEWGE DANIAL R/2221/06 Advisor: Abdul Walli (Ba)Documento30 pagineJune 2016: BY: ZEWGE DANIAL R/2221/06 Advisor: Abdul Walli (Ba)Reta TolesaNessuna valutazione finora

- Posted: Sat Feb 03, 2007 1:58 PM Post Subject: Causes For Non-Performing Assets in Public Sector BanksDocumento13 paginePosted: Sat Feb 03, 2007 1:58 PM Post Subject: Causes For Non-Performing Assets in Public Sector BanksSimer KaurNessuna valutazione finora

- 3.1 Financial Statements Firms Financial OperationDocumento13 pagine3.1 Financial Statements Firms Financial Operationnahu a dinNessuna valutazione finora

- Management of Financial Services - FM06Documento16 pagineManagement of Financial Services - FM06Amit ChoudharyNessuna valutazione finora

- Gopal B S Kle Work EDITS WORKSDocumento52 pagineGopal B S Kle Work EDITS WORKSSarva ShivaNessuna valutazione finora

- Financial Ratio Analysis ThesisDocumento8 pagineFinancial Ratio Analysis Thesismichellebojorqueznorwalk100% (1)

- 1 Background To The StudyDocumento4 pagine1 Background To The StudyNagabhushanaNessuna valutazione finora

- UntitledDocumento9 pagineUntitledSHER LYN LOWNessuna valutazione finora

- 6 ChapterDocumento11 pagine6 ChapterAbdullah Al MahmudNessuna valutazione finora

- India's Private or Public Sector Banks - Who Is BetterDocumento9 pagineIndia's Private or Public Sector Banks - Who Is BetterSammyPeachNessuna valutazione finora

- Thesis On Financial Analysis of BanksDocumento6 pagineThesis On Financial Analysis of Bankstonyacartererie100% (2)

- NPA EvalautiaonDocumento7 pagineNPA EvalautiaonmgajenNessuna valutazione finora

- E10Block2FINAL 09 11 2009Documento44 pagineE10Block2FINAL 09 11 2009ashfaqchauhanNessuna valutazione finora

- Ac 2020 14Documento8 pagineAc 2020 14vcpc2008Nessuna valutazione finora

- Commonwealth Bank (AutoRecovered)Documento13 pagineCommonwealth Bank (AutoRecovered)Shivam Anand ShuklaNessuna valutazione finora

- Bank MergersDocumento6 pagineBank MergersBhavin shahNessuna valutazione finora

- Mba-608 (CF)Documento14 pagineMba-608 (CF)Saumya jaiswalNessuna valutazione finora

- Analysis of Financial StatementDocumento28 pagineAnalysis of Financial Statementbijay bhandariNessuna valutazione finora

- COL Finance Sample ExamDocumento7 pagineCOL Finance Sample ExammedicinenfookiNessuna valutazione finora

- Profitability Performance of SBI and HDF PDFDocumento5 pagineProfitability Performance of SBI and HDF PDFNitin ParasharNessuna valutazione finora

- Business FinanceDocumento2 pagineBusiness FinanceKate Lawrence MendozaNessuna valutazione finora

- Budget Control in Retail Div. TNBDocumento12 pagineBudget Control in Retail Div. TNBWan KhaidirNessuna valutazione finora

- Project Synopsis FinanceDocumento8 pagineProject Synopsis FinanceMuhammed SanadNessuna valutazione finora

- Executive Summary - 1Documento6 pagineExecutive Summary - 1Hassnain HaiderNessuna valutazione finora

- Axis Bank: IIA Stage II ReportDocumento7 pagineAxis Bank: IIA Stage II ReportPrince PriyadarshiNessuna valutazione finora

- Pearls MonographDocumento32 paginePearls MonographDanielleNessuna valutazione finora

- Executive - AnswersDocumento53 pagineExecutive - AnswersRakesh KushwahaNessuna valutazione finora

- Imp Interview TopicsDocumento67 pagineImp Interview TopicsHarendra KumarNessuna valutazione finora

- 2M AmDocumento27 pagine2M AmMohamed AbzarNessuna valutazione finora

- DuPont Analysis Operating MethodDocumento31 pagineDuPont Analysis Operating MethodAi Lin ChenNessuna valutazione finora

- Internship 1-2Documento19 pagineInternship 1-2Unni sajeevNessuna valutazione finora

- MAQT AssignmentDocumento11 pagineMAQT AssignmentSahan RodrigoNessuna valutazione finora

- Lesson 1. Financial Statements (Cabrera & Cabrera, 2017)Documento10 pagineLesson 1. Financial Statements (Cabrera & Cabrera, 2017)Axel MendozaNessuna valutazione finora

- Fin Sight - Apr 2013Documento4 pagineFin Sight - Apr 2013rohitgupta234Nessuna valutazione finora

- Chapter One (1) 1.1 Background of The Organization: Performance MeasurementDocumento14 pagineChapter One (1) 1.1 Background of The Organization: Performance MeasurementDANIEL CHEKOLNessuna valutazione finora

- Financial Evaluation of Co Operative Credit SocietyDocumento48 pagineFinancial Evaluation of Co Operative Credit SocietyGLOBAL INFO-TECH KUMBAKONAMNessuna valutazione finora

- Chapter 2Documento8 pagineChapter 2Pradeep RajNessuna valutazione finora

- Loan Recovery StrategyDocumento7 pagineLoan Recovery Strategyrecovery cellNessuna valutazione finora

- BBI Managing Two Bottom Lines-30!09!15Documento8 pagineBBI Managing Two Bottom Lines-30!09!15Sumant DungdungNessuna valutazione finora

- Business 9709-w21-qp11Documento6 pagineBusiness 9709-w21-qp11sivanesshniNessuna valutazione finora

- Micro ¿ Nance Con¿ Dence IndexDocumento11 pagineMicro ¿ Nance Con¿ Dence IndexmfcstatNessuna valutazione finora

- Sme ReportDocumento25 pagineSme Reportyatheesh07Nessuna valutazione finora

- IRE-1702750 Study On Model and Camel Analysis of BankingDocumento16 pagineIRE-1702750 Study On Model and Camel Analysis of BankingDr Bhadrappa HaralayyaNessuna valutazione finora

- Npa 119610079679343 5Documento46 pagineNpa 119610079679343 5Teju AshuNessuna valutazione finora

- Financial analysis – Tesco Plc: Model Answer SeriesDa EverandFinancial analysis – Tesco Plc: Model Answer SeriesNessuna valutazione finora

- Model answer: Launching a new business in Networking for entrepreneursDa EverandModel answer: Launching a new business in Networking for entrepreneursNessuna valutazione finora

- Master Circular - Single Borrower Exposure Limit 09.04.2005Documento3 pagineMaster Circular - Single Borrower Exposure Limit 09.04.2005tazim07Nessuna valutazione finora

- DocumentDocumento4 pagineDocumentLee AlbareceNessuna valutazione finora

- Appendix 37 - Instructions - RADAIDocumento2 pagineAppendix 37 - Instructions - RADAIhehehedontmind meNessuna valutazione finora

- International Financial Market InstrumentsDocumento21 pagineInternational Financial Market InstrumentsJASVEER S86% (21)

- "A Study On Cryptocurrency in India - Boon or Bane": Mr.J.P.Jaideep,, Mr. K.Rao Prashanth JyotyDocumento6 pagine"A Study On Cryptocurrency in India - Boon or Bane": Mr.J.P.Jaideep,, Mr. K.Rao Prashanth JyotyJagan MbaNessuna valutazione finora

- CH11Documento31 pagineCH11Marwa HassanNessuna valutazione finora

- CASA Statement Aug2023 01092023003052 PDFDocumento7 pagineCASA Statement Aug2023 01092023003052 PDFTony TrisnoNessuna valutazione finora

- International Financial Institutions: 1. World BankDocumento9 pagineInternational Financial Institutions: 1. World BankTabish AhmedNessuna valutazione finora

- General AnnuityDocumento18 pagineGeneral AnnuityErang ErangNessuna valutazione finora

- Mr. AnshulDocumento2 pagineMr. AnshulAnshul SharmaNessuna valutazione finora

- Indian Financial System Chapter 1Documento16 pagineIndian Financial System Chapter 1Rahul GhosaleNessuna valutazione finora

- Synopsis: T.Y. Banking & Insurance Core Banking SolutionDocumento49 pagineSynopsis: T.Y. Banking & Insurance Core Banking SolutionjignaparmarNessuna valutazione finora

- Matura 2015 Repetytorium PR Vocabulary 7Documento2 pagineMatura 2015 Repetytorium PR Vocabulary 7Natalia ZdanowskaNessuna valutazione finora

- NRB RemitDocumento56 pagineNRB Remitনীল রহমানNessuna valutazione finora

- Certification MinutesDocumento3 pagineCertification MinutesAraceli Gloria-FranciscoNessuna valutazione finora

- Cashless SocietyDocumento1 paginaCashless Societyapi-323064191Nessuna valutazione finora

- Development of The Banking System of The Republic of UzbekistanDocumento3 pagineDevelopment of The Banking System of The Republic of UzbekistanEditor IJTSRDNessuna valutazione finora

- Curriculum Vitae Jeroen Rijpkema PDFDocumento2 pagineCurriculum Vitae Jeroen Rijpkema PDFJoeri KerkhofNessuna valutazione finora

- Chapter 5 MC and TFDocumento12 pagineChapter 5 MC and TFAngela de Mesa100% (1)

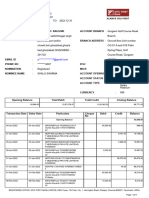

- Current & Saving Account Statement: Vishnu Gupta S/O Jagdish Gupta HNO 417 Mo Arya Nagar Shiv Ganj EtahDocumento6 pagineCurrent & Saving Account Statement: Vishnu Gupta S/O Jagdish Gupta HNO 417 Mo Arya Nagar Shiv Ganj Etahvishnu guptaNessuna valutazione finora

- Class 8: Chapter 15 - Simple Interest and Compound Interest - Exercise 15ADocumento13 pagineClass 8: Chapter 15 - Simple Interest and Compound Interest - Exercise 15AManu ThakurNessuna valutazione finora

- Ust 2014 NilDocumento40 pagineUst 2014 NilanajuanitoNessuna valutazione finora

- IDFCFIRSTBankstatement 10078073407 125932259Documento9 pagineIDFCFIRSTBankstatement 10078073407 125932259Ashwani KumarNessuna valutazione finora

- Plastic MoneyDocumento13 paginePlastic MoneyPrashant Jadhav70% (10)

- 846 में हैDocumento1 pagina846 में हैAbhishek BansalNessuna valutazione finora

- Cesar v. Areza and Lolita B. Areza Vs - Express Savings Bank, Inc. and Michael PotencianoDocumento4 pagineCesar v. Areza and Lolita B. Areza Vs - Express Savings Bank, Inc. and Michael PotencianoSam SaripNessuna valutazione finora

- Notes Payable and Bonds Payable - Quiz - With Answers - For PostingDocumento8 pagineNotes Payable and Bonds Payable - Quiz - With Answers - For PostingWinny PoeNessuna valutazione finora

- Reading Material Dec2020Documento14 pagineReading Material Dec2020jyottsnaNessuna valutazione finora

- Bank Statements PDFDocumento5 pagineBank Statements PDFhanhNessuna valutazione finora